| Contents | |

|---|---|

| Introduction: | General notes on the return |

| Section A: | Balance Sheet |

| Section B: | Profit & Loss Account |

| Section C: | Capital |

| Section D: | Lending: Business Flows & Rates |

| Section E: | Residential Lending to Individuals: New Business Profile |

| Section F: | Lending: Arrears Analysis |

| Section G: | Mortgage Administration: Business profile |

| Section H: | Mortgage Administration: Arrears analysis |

| Section J: | Fee tariff measures |

| Section K: | Sale and rent back (SRB agreement) business |

| Section L: | Credit risk |

| Section M: | Liquidity |

INTRODUCTION: GENERAL NOTES ON THE RETURN

1. Introduction

This section covers a number of points that have relevance across the return generally:

• Overview

• Purpose of reporting requirements

• Regulated mortgage contracts and the wider mortgage market

• Home reversion plans and Home purchase plans

• Sale and rent back business

• Accounting conventions

• Accuracy

• Time period

• Loans made before 31 October 2004

• Second charge regulated mortgage contracts

• Specific items:

- (i) positions to be reported gross

- (ii) foreign currencies

2. Overview of reporting requirements

The data requirements for firms carrying on the regulated activities of home finance providing activity and administering a home finance transaction consist of quarterly, half yearly and annual information. The same data requirements apply to a P2P platform operator facilitating home finance transactions where a lender or provider does not require permission to enter into the transaction, and references to home finance providers or home finance administrators should be read as including such P2P platform operators, where relevant.

This guidance deals only with the quarterly requirements, however, which are referred to as the Mortgage Lenders and Administrators Return (MLAR). The remaining data requirements are applied to firms through existing rules within the following sections of the Handbook:

• the Dispute Resolution: Complaints sourcebook for complaints reporting; and

• Chapter 16 of the Supervision manual for controllers reports (section 16.4), close links report (section 16.5) and annual accounts (section 16.12).

Because the MLAR is activity based, not all sections are applicable to all types of home finance activity firm. The applicability of each section is explained in the table below:

| Section | Applicability: |

|---|---|

| A1 and A2: Balance sheet | Applies to all home finance activity firms except: • A firm that is required to submit a balance sheet by a lower numbered regulated activity group, as described in SUP 16.12.3R(1)(a)(iii) • An incoming EEA firm (note a) |

| A3: Analysis of loans to customers | Applies to all home finance activityfirms |

| A4: Analysis of second charge loans to customers | Applies to all home finance activity firms in respect of second charge regulated mortgage contracts. |

| B1: Income statement | Applies to all home finance activity firms except: • A firm that is required to submit an income statement by a lower numbered regulated activity group, as described in SUP 16.12.3R(1)(a)(iii) • An incoming EEA firm (note a) |

| B2: Provisions analysis | Applies to all home finance activityfirms |

| C: Capital | Applies to all home finance activityfirms except: • A firm that is required to submit a capital adequacy data item by a lower numbered regulated activity group, as described in SUP 16.12.3R(1)(a)(iii) • An incoming EEA firm (note a) • A firm which is a solo-consolidated subsidiary of an authorised credit institution • A firm which exclusively carries on home finance activities in relation to second charge regulated mortgage contracts, as set out in SUP 16.12.18BR (note 4). |

| D: Lending: business flows and rates | Applies to all firms with permission to undertake a home finance providing activity except: |

| D(a): Second charge business flows and rates | Applies to all home finance providing activity firms in respect of second charge regulated mortgage contracts. |

| E: Residential lending to individuals: new business profile | Applies to all firms with permission to undertake a home finance providing activity except: |

| E1(a) and E2(a): Second charge lending to individuals | Applies to all home finance providing activity firms in respect of second charge regulated mortgage contracts. |

| F: Lending: Arrears Analysis | Applies to all firms with permission to undertake a home finance providing activity except: |

| F(a): Second charge lending: Arrearsanalysis | Applies to all home finance providing activity firms in respect of second charge regulated mortgage contracts. |

| G: Mortgage Administration: Business Profile | Applies to all firms with permission to undertake administering a home finance transaction, except: |

| H: Mortgage Administration: Arrears analysis | Applies to all firms with permission to undertake administering a home finance transaction, except: |

| H(a): Second charge mortgage administration: Arrears analysis | Applies to all firms with permission to undertake administering a home finance transaction, in respect of second charge regulated mortgage contracts. |

| J: Fee tariff measures | Applies to all home finance activity firms |

| K: Sale and rent back business | Applies to SRB agreement providers and SRB administrators |

| L: Credit risk | Applies to a firm that meets the conditions of SUP 16.12.18BR (notes 2 and 4). |

| M: Liquidity | Applies to a firm that meets the conditions of SUP 16.12.18BR (notes 3 and 4). |

| Note (a): Credit Institutions passporting under BCD for mortgage lending (which also includes mortgage administration), or other firms passporting under another EU Directive for a non-mortgage activity and holding a top-up permission from the appropriate regulator for mortgage lending and/or mortgage administration. Also includes firms classed as "Treaty firms" under Schedule 4 of the Act. But any other EEA firm type should complete in full all sections of the MLAR described above this table, as it would not be eligible for any reduction in reporting requirements. | |

3. Purpose of reporting requirements

The reasons why the FCA requires this data from home finance providers and administrators are as follows:

• to assess the probability of the failure of firms and the impact of failure on the ability of the FCA to meet its statutory objectives, including an assessment of compliance with the threshold conditions;

• to assist with prudential supervision of firms; and

• to help assess the risks in the home finance market as a whole to inform, for example, the FCA’s thematic work. By this we mean that we will use some of our supervisory resources to examine issues (known as ‘themes’) that affect a number of firms rather than firms individually. The data collected will be considered alongside other information we receive, to identify trends and issues that inform our supervision of firms.

The MLAR requires home finance providers and administrators to submit four types of data:

• financial data to assist in the prudential supervision of home finance providers and administrators. A quarterly financial return is required, including a balance sheet and profit and loss account;

• quarterly reporting of quantitative and qualitative data by all home finance providers and administrators to enable monitoring of compliance with the requirements of MCOB;

• quarterly provision of qualitative home finance information by all home finance providers and administrators to enable the FCA to understand developments in the home finance markets as a whole, and to inform future policy developments and prudential supervision; and

• annual reporting of information on fee tariff measures.

The reporting requirements set out in the MLAR enable the FCA to realise these information needs. In particular:

| Tables A to C, L, M: | provide the framework for the FCA’s financial monitoring and prudential supervision of home finance providers and administrators; |

| Tables D to F: | provide the framework for the provision of qualitative home finance information by home finance providers; |

| Tables G, H: | provide the framework for the FCA’s monitoring of administering a home finance transaction activity; |

| Table J: | provides information on fee tariff measures for home finance providers and administrators; |

| Table K: | provides the framework for the FCA’s monitoring of SRB agreement providers and SRB administrators. |

4. Regulated mortgage contracts and the wider mortgage market

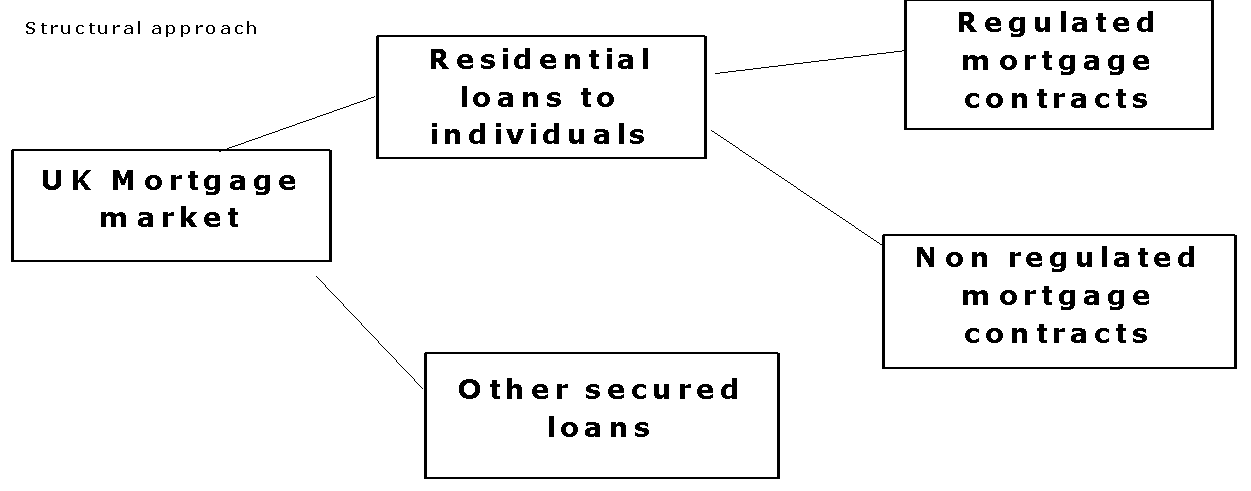

Given this background to reporting requirements, the FCA’s approach to obtaining information on mortgage lending has been structured so that regulated mortgage contracts are seen within the wider context of the UK mortgage market as a whole. This approach can be illustrated as follows:

Each of these key terms is explained below:

(i) UK mortgage market

This refers to all lending secured on land and buildings in the United Kingdom, whether to individuals, housing associations or corporates. However, given the importance of mortgages to individuals we have chosen to look at the market in terms of two components, namely 'residential lending to individuals' and 'other secured lending'. Loans and mortgages secured on land in the EEA other than the UK should be reported in ‘other loans’ in section A3 of the MLAR.

(ii) Residential loans to individuals

This is a discrete category of the mortgage market, and has characteristics (e.g. in terms of products, lending criteria and methods of credit assessments) that are often markedly different from those applying to other types of secured lending (e.g. to corporates).

It is lending to individuals secured by mortgage on land and buildings where the lender has either a first or second (or subsequent) charge, where at least 40% of the land and buildings is used for residential purposes, and where the premises are for occupation by either the borrower (or dependant), or any other third party (e.g. it includes ‘buy to let’ lending to individuals).

Only loans where there is a one-to-one correspondence between the loan and a specific security should be included within ‘residential loans to individuals’. Do not include here any residential loans to individuals that are part of a ‘business loans’ type package (involving multiple loans and multiple securities, where there is no one-to-one correspondence between a loan and a specific security), but report them under ‘other secured lending’.

Regulated mortgage contracts that are secured on UK land are therefore a subset of this market category.

Examples of non-regulated mortgage contracts which fall under the wider category of residential loans to individuals include: buy-to-let loans and other types of loan where the property is not for use by the borrower (or qualifying dependants). Prior to 21 March 2016, non-regulated mortgage contracts also included second charge mortgage lending.

(iii) Other secured lending

This covers all other forms of lending secured on land and buildings in the United Kingdom. Primarily it covers secured lending to corporate bodies (including to housing associations), but it also includes lending to individuals which, although being secured on land and buildings, is not deemed to be residential (e.g. the residential element is less than 40%). A corporate body for this purpose is any entity other than an individual. Loans and mortgages secured on land in the EEA other than the UK should be reported in ‘other loans’ in section A3 of the MLAR.

It also includes any residential lending to an individual that forms part of a ‘business loan’ type package. These arrangements between a lender and a borrower are usually offered by a lender’s specialist business or corporate lending departments. They typically involve a number of loans secured against a range of securities including the borrower’s residential property, business premises and the business itself. Such packages involve no specific one-to-one correspondence between a single loan and a single security, and instead the lender assesses loan cover against the basket of securities in the package. Given the business nature of this type of lending, it would therefore be misleading to try and classify some or all of the loan elements in such cases to any part of ‘residential lending to individuals’, and hence all such lending should be reported under ‘other secured lending’. This is for MLAR reporting purposes only; the actual categorisation or treatment for MCOB purposes remains unchanged.

(iv) Regulated mortgage contract

This is defined in the Handbook as follows:

- (a) (in relation to a contract) a contract which:

- (i) (in accordance with article 61(3) of the Regulated Activities Order) at the time it is entered into, meets the following conditions:

- (A) a lender provides credit to an individual or to trustees (the ‘borrower’); and

- (B) the obligation of the borrower to repay is secured by a mortgage on land in the EEA, at least 40% of which is used, or is intended to be used, in the case of credit provided to an individual, as or in connection with a dwelling; or (in the case of credit provided to a trustee who is not an individual), as or in connection with a dwelling by an individual who is a beneficiary of the trust, or by a related person;

- (ii) is not a home purchase plan, a limited payment second charge bridging loan, a second charge business loan, an investment property loan, an exempt consumer buy-to-let mortgage contract, an exempt equitable mortgage bridging loan, an exempt housing authority loan or a limited interest second charge credit union loan within the meaning or article 61A(1) or (2) of the Regulated Activities Order; and

- (iii) if the contract was entered into before 21 March 2016:

- (A) at the time the contract was entered into, entering into the contract constituted the regulated activity of entering into a regulated mortgage contract; or

- (B) the contract is a consumer credit back book mortgage contract within the meaning of article 2 of the MCD Order.

- (i) (in accordance with article 61(3) of the Regulated Activities Order) at the time it is entered into, meets the following conditions:

- (b) (in relation to a specified investment) the investment, specified in article 88 of the Regulated Activities Order, which is rights under a regulated mortgage contract within (a).

[Note: articles 3(1)(a) and 4(2) of the MCD]

Loans and mortgages secured on land in the EEA other than the UK, although regulated mortgages, should be reported in ‘other loans’ in section A3 of the MLAR.

- (a) (in relation to a contract) a contract which:

(v) Second charge regulated mortgage contract

A second charge regulated mortgage contract is defined in the Handbook as a regulated mortgage contract which is not a first charge legal mortgage. Therefore, it includes second and subsequent charge mortgages.

Data which is provided in relation to a second charge regulated mortgage contract in A3(a), D (a), E(1)(a), E(2)(a), F(a), or H(a) in SUP 16 Annex 19AAR will also need to be provided as part of the data items in A3, D, E, F or H, as the case may be, in SUP 16 Annex 19AR.

The guidance on how to submit the data items in A3, D, E, F or H of SUP 16 Annex 19AR applies to A3(a), D(a), E(1)(a), E(2)(a), F(a) or H(a) of SUP 16 Annex 19AAR where the same terms are used in the corresponding parts of SUP 16 Annex 19AAR.

4a. Home reversion and home purchase plans

Definitions

This is defined in the Handbook as follows:

(in accordance with article 63B(3) of the Regulated Activities Order) an arrangement comprised in one or more instruments or agreements which meets the following conditions at the time it is entered into:

- (a) the arrangement is one under which a person (the reversion provider) buys all or part of a qualifying interest in land from an individual or trustees (the reversion occupier);

- (b) the reversion occupier (if he is or she an individual) or an individual who is a beneficiary of the trust (if the reversion occupier is a trustee), or a related person, is entitled under the arrangement to occupy at least 40% of the land in question as or in connection with a dwelling and intends to do so; and

(c) the arrangement specifies that the entitlement to occupy will end on the occurrence of one or more of:

- (i) a person in (b) becoming a resident of a care home;

- (ii) a person in (b) dying; or

- (iii) the end of a specified period of at least twenty years from the date the reversion occupier entered into the arrangement;

in this definition "related person" means:

- (A) that person’s spouse or civil partner;

- (B) a person (whether or not of the opposite sex) whose relationship with that person has the characteristics of the relationship between husband and wife; or

- (C) the person’s parent, brother, sister, child, grandparent or grandchild.

Guidance to home reversion (HR) and home purchase plan (HPP) firms on the completion of the MLAR

It is recognised that HR and HPP products are not loans as such, being effectively sale and lease products. However, in order to use the MLAR as a vehicle for capturing some data on these products, they are to be treated for MLAR purposes as if they were loan products. This means that:

- (i) For a firm which is a provider of HR and/or HPP products:

- • HR and HPP products are to be included in the balance sheet within A1.6 "Loans to Customers". This may differ from the reporting of such products in a firm's published accounts.

- • Within section A3, which contains a further breakdown of "Loans to Customers", HR and HPP products are to be reported within the single category A3.5 "Other Loans".

- • As a consequence, the FCA will be able to capture the key balances outstanding on these products (including any which may have been securitised).

- (ii) For a firm which is undertaking administration of HR and/or HPP products (and where that firm did not also act as provider of these products):

- • HR and HPP products being administered for third parties are to be reported in section G.

- • Within G1 and G2 they are to be reported within the "Other firms" category. They should however be shown under "regulated loans" solely for the purposes of recording their administration in the MLAR.

- • In section G2.2, when entering the "name of firm" in column 2, add "HR" and/or "HPP" in brackets after the name, as appropriate.

4b. Sale and rent back (SRB) agreement business

Definitions

A regulated sale and rent back agreement

This is defined in the Handbook as follows:

(in accordance with article 63J(3)(a) of the Regulated Activities Order) an arrangement comprised in one or more instruments or agreements, in relation to which the following conditions are met at the time it is entered into:

- (a) the arrangement is one under which a person (an agreement provider) buys all or part of the qualifying interest in land in the United Kingdom from an individual or trustees (the "agreement seller"); and

- (b) the agreement seller (if they are an individual) or an individual who is the beneficiary of the trust (if the agreement seller is a trustee), or a related person, is entitled under the arrangement to occupy at least 40% of the land in question as or in connection with a dwelling, and intends to do so;

but excluding any arrangement that is a regulated home reversion plan.

Guidance to regulated SRB firms on the completion of the MLAR

This section explains how SRB firms should complete the MLAR.

SRB providers and administrators should complete the following sections of the MLAR:

• Section A (balance sheet);

• Section B (profit and loss account);

• Section C (capital);

• Section J (fees tariff measures): and

• Section K (sale and rent back business).

SRB firms should not complete sections D to H, L or M in respect of their SRB business.

SRB providers should note the following in relation to their reporting of SRB agreements and SRB assets:

In section A

• Do not enter any information on SRB agreements in A1.6 ‘Loans to customers’ or A3.5 ‘Other loans’.

• Report SRB assets in A1.11.

• Report any liabilities incurred in acquiring SRB assets in A2.7.

In section B

• Where applicable, information on SRB agreements should be entered in B2.5 ‘Other loans’.

As a consequence the FCA will be able to capture key information on these products.

5. Accounting conventions

Unless the contrary is stated in these guidance notes, the return should be compiled using generally accepted accounting practice.

However, information in respect of lending (e.g. balances, advances, interest rates, arrears etc) to be reported in sections D, E, F, G, H and J of the return should not be fair-valued but should be reported as the contractual position (i.e. as between lender and borrower).

All amounts should be shown in one of the reporting currencies accepted by the relevant platform provided by the FCA, unless otherwise specified in the Handbook.

6. Accuracy

It is expected that entries on the return will be actual values, or in some cases close approximations established or drawn from the firm’s systems and prepared on the basis of being the best information in the time available for their compilation.

If such 'close approximations' are considered by the firm as likely to be materially different from the underlying actual values, the firm should advise its supervisory team of data items affected.

7. Time periods

Where stock figures are required (e.g. balance sheet, capital position) the information is required as at the firm’s accounting reference date and the three quarter ends following this date (see SUP 16.3.13R).

Where flow figures are required, these are either for 3 months only (i.e. the latest quarter) as in for example lending figures in tables D and E, or cumulative in the 'year to date', (e.g. profit and loss in table B), covering the period from the firm’s accounting reference date to the end of the reporting quarter.

8. Loans made before 31 October 2004

This section does not apply to second charge regulated mortgage contracts.

(i) Classifying the ‘back book’

Many loans made before 31 October 2004 became regulated as regulated mortgage contracts on 21 March 2016 or, depending on the nature of the loan and the applicable transitional provisions, on a date no later than 21 March 2017; these loans should be treated as regulated mortgage contracts in the MLAR accordingly. Loans made before 31 October 2004 which continue not to be regulated as regulated mortgage contracts fall into the following categories:

• residential loans to individuals which, for the purposes of the MLAR, should be classified as non-regulated (see Introduction, section 4(ii)); for example at A3.3 and D1.2.

• other secured loans (see Introduction, section 4(iii)); for example at A3.4 and D1.3.

• other loans (see Guidance for A3.5).

The approach to classification for pre-31 Oct 2004 loans will, of necessity, need to be a pragmatic one. We do not, for example, envisage the need to look at individual paper loan files. Rather, we expect the firm to apply its knowledge of its various loan books, products and their characteristics, to come up with some realistic allocation rules. This enables the firm to apply some automatic process to its computerised loan records, and thereby classify individual loans into each of the relevant categories used in the MLAR. Such a process may not be perfect, and it may result in a few loans being wrongly allocated, but it will be sufficient for the purpose.

(ii) Specific treatment of residential loans to individuals

Any loans made before 31 October 2004 that have not become regulated as regulated mortgage contracts, should be reported as non-regulated loans in the various parts of the MLAR.

This reporting basis for loans should continue until such time, if ever, that a subsequent transaction on the loan causes it to be formally treated as a regulated contract.

(iii) Further advances on loans made before 31 October 2004 which have not already become regulated as regulated mortgage contracts

We cannot be prescriptive about whether a further advance (or any other variation) to a pre-31 October 2004 mortgage which has not already become regulated as a regulated mortgage contract (see (i) above) will have the effect of creating a new regulated mortgage contract. Whether a variation amounts to creating a new contract will depend on each lender's individual mortgage documentation. This documentation will differ, possibly significantly, between firms. Each lender will need to review its existing documentation and take a view on the scope that this provides for making changes.

In practice this means that:

• If the lender can make a further advance without creating a new contract (i.e. makes a variation to the existing mortgage contract), then the further advance should be added to the original loan and the combined loan treated as a single loan for MLAR reporting. This combined loan should be reported as ‘non-regulated’;

• If making a further advance creates a new contract, (and this further advance is a regulated mortgage contract) then the correct reporting approach will be determined as follows:

- (a) where the original loan was made before 31 October 2004, has not in the meantime become a regulated mortgage contract (for example, because it is not a regulated credit agreement) but would otherwise satisfy the specific requirements of a regulated mortgage contract, and the further advance is documented in a new loan agreement separate from the original loan (and is not a variation to the existing mortgage contract), the original loan and further advance may be treated as one for MLAR reporting, being shown as ‘regulated’ under “Residential loans to individuals”;

- (b) where the original loan did not satisfy the defined conditions of a regulated mortgage contract at the time it was entered into and has not in the meantime become a regulated mortgage contract, and the further advance is documented in a new loan agreement separate from the original loan (and is not a variation to the existing mortgage contract), the old loan and further advance will be treated as two separate loans for most aspects of MLAR reporting, the former being ‘unregulated’ while the latter will be reported as ‘regulated’. However, for the LTV and Income Multiple analysis, while the firm should only show the amount of the further advance in the relevant “cell”, the “cell” should be determined by using the total amount of the loan (old loan + further advance) when deciding which LTV band and which Income Multiple band are applicable; and

- (c) where the lender decides to combine the original loan and the further advance to create a single new contract that replaces the existing mortgage contract and is a regulated mortgage contract, this should be reported as ‘regulated’.

9. Specific items

(i) Positions to be reported gross

In general, liabilities and assets should be shown gross, and not netted off (unless there is a legal right of set-off). Thus an account which moves from credit to debit will move from one side of the balance sheet to the other.

A notable exception to this however concerns the reporting of loan assets, which should follow MIPRU 4.2.14R to MIPRU 4.2.16G. Such assets should be shown in the balance sheet net of linked funding; similarly in other tables where balances are reported on the same basis. Only sections A3, D2, G and H require the reporting of such loan assets on a ‘gross’ basis.

The treatment of loan assets that are being operated as part of a current account offset mortgage product (or similar products where deposit funding is offset against loan balances in arriving at a net interest cost on the account) will depend on the conditions pertaining to the mortgage product. The balance outstanding on such loans will need to be reported on the basis of the contractually defined balance according to the terms of the mortgage product. This might be the amount of loan excluding any offsetting funds, or it might be the net amount.

(ii) Foreign currencies

Firms should report in the currency of their annual audited accounts, where this is Sterling, Euro, US Dollars, Canadian Dollars, Swedish Kroner, Swiss Francs or Yen. Where annual audited accounts are reported in a currency outside those specified above, please translate these values into an equivalent within the list using an appropriate rate of exchange at the reporting date, or where appropriate, at the rates of exchange fixed under the terms of any relevant currency hedging transaction, and use that value in the return. Please report in thousands where stated on the return. Firms should apply the same accounting treatment as for their published accounts.

SECTION A: BALANCE SHEET

Balance sheet analysis

A1, A2 | The balance sheet is intended to reflect the practices used in compiling published or other accounts, although its format in the MLAR (with 'total assets' and 'total liabilities') will not necessarily be the same as that used by firms in their regular accounts. ‘Loans to customers’ is expected to be the customer balance after any write-offs have been taken. |

| A1.6 | Loans to customers may be a non-standard accounting sub-head for some firms whose business is not primarily mortgage related. But since this is an explicit MLAR data requirement, it should be split out from the sub-head under which it is routinely shown in the firm’s other accounts. Include HR and HPP products here. |

| A1.11 | Other current assets should include all assets measured at fair value not included in any other asset category on the return. Include any SRB assets here. |

| A2.1 | Shareholders' funds should include any unrealised gains or losses resulting from the fair valuation of available-for-sale financial assets, and any fair value gains or losses arising on cash flow hedges of financial instruments measured at cost or amortised cost. |

| A2.7 | Other liabilities should include all liabilities measured at fair value not included in any other liability category on the return. Include any liabilities incurred in acquiring SRB assets here. |

| A3 | Analysis of loans to customers This section recognises that some lenders may have securitised loans on their balance sheet, and hence provides for unsecuritised/securitised loans to be shown separately. Unsecuritised balances are analysed in terms of three elements: gross loan balances (before deduction of any provisions); provisions balances in respect of those balances; and the net balances after deduction of such provisions. Securitised balances are analysed in a similar way, except that 'gross' also means before the deduction of any linked non-recourse funding, the amount of which is also to be shown separately. |

| A3.1-4 | See Introduction (paragraphs 4(i) to (iv)) for details of the coverage of these terms. |

| A3.5 | Other loans refers to any lending secured on land and buildings outside of the UK, any loan for which security is provided other than by land and buildings, together with all unsecured loans (e.g. consumer credit, personal loans, or such loans to corporates). Loans and mortgages secured on land in the EEA other than the UK should be reported here. |

| A3.6 | It is expected that net balances on unsecuritised loans plus net balances on securitised loans will equal the entry shown at A1.6 in the main balance sheet analysis of assets. |

SECTION B: PROFIT & LOSS ACCOUNT

| B0 | Financial year to date In terms of reporting period, the analysis should be compiled on a ‘year to date’ basis, covering successively 3, 6, 9 or 12 months from the firm’s accounting reference date. |

| B1 | Profit & Loss Account The P&L section is intended to reflect the practices used in compiling accounts prepared under the Companies Acts, although its format in the MLAR (with explicit focus on financial items such as interest, fees & commissions etc) will not necessarily be the same as that used by firms in their regular accounts. The reason for this approach is that most lenders to which this section is applicable are mortgage specialists, and as such it is considered desirable to put their P&L format onto a similar basis as that used for banks and building societies. The analysis therefore requires the firm’s profit & loss account to be re-structured in a way that makes a number of items explicit in the interests of achieving consistency with other reporting firms. |

| B1.1 | Focuses on gross profit from non-financial activities |

| B1.2-1.7 | Covers a range of income elements which are more closely related to financial activities, including in particular those associated with mortgage lending. In particular B1.7 Other income should include unrealised gains in respect of assets and liabilities which have been measured on a fair value basis. |

| B1.9-1.13 | Covers a range of expenditure elements, including those related to non-financial and also to financial (including mortgage related) activities. In particular B1.13 Other expenses should include unrealised losses in respect of assets and liabilities which have been measured on a fair value basis. |

| B1.15 | Operating Profit is total income less total expenses. |

| B1.16 | Provisions covers write-offs and provisions charges on bad and doubtful debts, (including for example on mortgage loans); any suspended interest (i.e. any interest included in Interest receivable which, through loan default, impairment or otherwise, is deemed unlikely to be received); and any other provisions for contingent liabilities. |

| B2 | Provisions analysis This supplementary analysis draws together the key movements in provisions balances from the firm’s accounting reference date up to the reporting quarter end. The two ‘flow items’, namely write-offs and provisions charges, are those relating to the period from the firm’s accounting reference date up to the reporting date. The total of provisions charges in line B2.6 (column 3) will not necessarily be the same as the provisions charge in the Profit & Loss analysis at B1.16 (since this latter item may include further provisions against other asset items not included in B2.6, or provisions arising from other sources). |

SECTION C: CAPITAL

INTRODUCTION

The threshold conditions state that the resources of a firm must be adequate in the opinion of the FCA in relation to the regulated activities that the firm seeks to carry on or carries on. In addition, a firm is required to maintain 'adequate financial resources'. A home finance administrator or lender should have adequate capital and funding in order to be able to meet these requirements.

In addition, the FCA and the PRA are required to identify the main risks to their statutory objectives. In assessing firm-specific risks we are required to assess the risks arising from the financial failure of a firm (due to business risks from the external environment, or control risks arising from the firm itself) which might affect both the market and individual customers. The specific FCA objectives that are potentially impacted are those relating to market confidence and consumer protection.

Details provided in this section on Capital are drawn from the appropriate provisions of MIPRU 4 (Capital Resources).

| C1-2 | CAPITAL RESOURCES | |

C1 and C2 set out the individual components of eligible capital and the separate deductions that should be made to arrive at capital resources. Components of eligible capital are: | ||

(1) Share capital Share capital must be fully paid (i.e. the firm is under no obligation to repay this capital unless and until the firm is wound up) and may include ordinary share capital or preference share capital (excluding preference shares redeemable by shareholders within two years). See paragraph (7) Subordinated loans below for details of the limits that may apply to the inclusion of redeemable preference shares in capital resources. | ||

(2) Partnership or sole trader capital Partnership capital is capital made up of the partners’ capital account. The capital account is an account into which capital contributed by the partners is paid and from which, under the terms of the partnership agreement, an amount representing capital may be withdrawn by a partner only if he or she ceases to be a partner and an equal amount is transferred to another such account by his or her former partners or any person replacing him or her as their partner, or the partnership is otherwise dissolved or wound up. Sole trader capital is the net balance on the firm’s capital account and current account. | ||

(3) Reserves Reserves are accumulated profits retained by the firm (after deduction of tax, dividends and proprietors’ or partners’ drawings) and other reserves created by appropriations of share premiums and similar realised appropriations. Reserves also include gifts of capital, for example, from a parent company. For partnerships, reserves include partners’ current accounts according to the most recent financial statement. Reserves must be audited unless the firm is eligible to include unaudited reserves in its capital resources calculation under MIPRU 4.4.2R. The reserves figure is subject to the following adjustments, where appropriate: (a) any unrealised gains must be deducted or, where applicable, any unrealised losses added back in on cash flow hedges of financial instruments measured at cost or amortised cost; (b) any unrealised gains must be deducted or, where applicable, any unrealised losses added back in on debt instruments held in the available-for-sale financial assets category. Any unrealised gains or losses on equities held in the available-for-sale financial assets category should be reported at C1.5; (c) in respect of a defined benefit occupational pension scheme, any defined benefit asset must be derecognised; A firm may substitute for a defined benefit liability the firm's deficit reduction amount provided that that election is applied consistently in respect of any one financial year. | ||

(4) Interim net profits and partners’ interim current accounts A firm is not required to take into account interim net profits. However, if it does, the profits have to be verified by the firm’s external auditors, net of tax, anticipated dividends or proprietors’ drawings and other appropriations unless the firm is eligible to include unverified interim net profits in its capital resources calculation under MIPRU 4.4.2R. In terms of the verification for inclusion, for the first, second and third financial quarters firms may include interim profits in their MLAR, on the understanding that the firm will obtain the required verification from its external auditors within two months of the financial quarter end. (The FCA may ask for a copy of the verification statement.) For the fourth quarter the FCA will rely on the forthcoming audited accounts as providing verification and accordingly the full year’s profits should be included in the make-up of eligible capital under interim profits in the return. | ||

(5) Revaluation reserve Firms should report reserves relating to the revaluation of fixed assets. | ||

(6) General/collective provisions Firms should report general/collective provisions that are held against potential losses that have not yet been identified, but which experience indicates are present in the firm’s portfolio of assets. Such provisions must be freely available to meet these unidentified losses wherever they arise. General/collective provisions must be verified by external auditors and disclosed in the firm’s annual report and accounts annual report and accounts unless the firm is eligible to include unaudited general and collective provisions in its capital resources calculation under MIPRU 4.4.2R. | ||

(7) Subordinated loans Subordinated debt (i.e. the amount of principal outstanding before amortisation) must not form part of the capital resources of a firm unless it meets the following conditions: | ||

| (1) | it has an original maturity of at least five years or is subject to five years’ notice of repayment; | |

| (2) | the claims of the subordinated creditors must rank behind those of all unsubordinated creditors; | |

| (3) | the only events of default must be non-payment of any interest or principal under the debt agreement or the winding up of the firm; | |

| (4) | the remedies available to the subordinated creditor in the event of non-payment or other default in respect of the subordinated debt must be limited to petitioning for the winding up of the firm or proving the debt and claiming in the liquidation of the firm; | |

| (5) | the subordinated debt must not become due and payable before its stated final maturity date except on an event of default complying with (3); | |

| (6) | the agreement and debt are governed by the law of England and Wales, or of Scotland, or of Northern Ireland; | |

| (7) | to the fullest extent permitted under the rules of the relevant jurisdiction, creditors must waive their right to set off amounts they owe the firm against subordinated amounts owed to them by the firm; | |

| (8) | the terms of the subordinated debt must be set out in a written agreement or instrument that contains terms that provide for the conditions set out in (1) to (7); and | |

| (9) | the debt must be unsecured and fully paid up. | |

For a mortgage lender or mortgage administrator undertaking business connected to regulated mortgage contracts (unless its Part 4A permission prevents it from undertaking new business), MIPRU 4.4.8R limits the amount of subordinated loans and redeemable preference shares that can be included in eligible capital. In Table C of the MLAR the firm will deduct from capital resources under item C2.3a any amount by which the subordinated loans and redeemable preference shares exceed the limit in MIPRU 4.4.8R. | ||

| Treatment of eligible capital items (listed above) in section C1: | ||

| C1.1 | Reserves: include items • reserves • revaluation reserves | |

| C1.2 | Interim profits: include items • interim net profits • partners’ interim current accounts | |

| C1.3 | Issued capital: include items • share capital • partnership or sole trader capital | |

| C1.3a | Subordinated loans | |

| C1.4 | General/collective provisions | |

| C1.5 | Other eligible capital: includes • any other item of eligible capital not required to be included in items C1.1 to C1.4, including any unrealised gains or losses on equities held in the available for sale financial assets portfolio. | |

| C1.6 | Total eligible capital This is the sum of the components listed in C1.1 to C1.5. | |

| C2 | Deductions from capital | |

| C2.1 | Investments in own shares represents any investment in the shares of the company, quantified as fixed assets in the balance sheet. | |

| C2.2 | Intangible assets are the full balance sheet value of goodwill, capitalised development costs, brand names, trademarks and similar rights and licences. | |

| C2.3 | Interim net losses refers to the cumulative amount covering the period from the firm’s accounting reference date to the end of the current quarter. All the current year’s losses should be reported. Unpublished losses from the previous accounting period should also be shown here. | |

| C2.3a | Subordinated loan and redeemable preference share restriction This is the amount of any excess as computed under the restriction explained in paragraph (7) of the C1-2 CAPITAL RESOURCES section above. | |

| C2.4 | Other deductions from capital: include • Excess of drawings over profits for partnerships or sole traders: firms should report the difference between the personal drawings of a partnership or sole trader and the profit in the period, where the drawings exceed the profit for the period. | |

| C2.5 | Total deductions This is the sum of the components listed in C2.1 to C2.4. | |

| C3 | CAPITAL RESOURCES CALCULATION | |

| C3.1 | Capital resources This is total eligible capital less total deductions (C1.6 to C2.5). | |

| C3.2 | Capital requirement This is the amount calculated in sections C4.6(e) or C5.5(c), whichever is applicable. | |

| C3.3 | Surplus/(Deficit) of resources This is the capital resources less the capital requirement (C3.1 to C3.2). | |

| C4 | CAPITAL REQUIREMENTS Capital requirement for a lender, or an administrator with administered assets on its balance sheet | |

| C4.1 | The capital requirement for lenders or administrators that have the regulated mortgage contracts that they administer on their balance sheet is asset-based, and the information required is detailed in C4.2 to C4.6. | |

| C4.2 | Total assets: this is the total value of assets as shown at line A1.12 in section A of the MLAR. | |

| C4.2a | Assets subject to the credit risk requirement This is the amount of assets subject to the credit risk requirement computation as shown at line 6A in section L of the MLAR. This is relevant for a mortgage lender; or mortgage administrator with its administered assets on balance sheet, that undertakes business connected to regulated mortgage contracts and has one or more exposures which satisfy the conditions set out in MIPRU 4.2A.4R. | |

| C4.3 | Undrawn commitments Undrawn commitments means the total of those amounts which a borrower has the right to draw down from the firm but which have not yet been drawn down (see MIPRU 4.2.12R and MIPRU 4.2.13G). However, undrawn commitments should not be included in the calculation of capital requirements if they have an original maturity of up to one year or if they can be unconditionally cancelled at any time by the lender. Similarly, existing mortgage offers should not be included in the calculations of capital requirements if the offer has an original maturity of up to one year or can be unconditionally cancelled at any time by the lender. | |

| C4.4 | Intangible assets: this is the amount shown at C2.2. | |

| C4.5 | Total adjusted assets: this is the sum of C4.2 and C4.3, less C4.2a and C4.4. | |

| C4.6 | CAPITAL REQUIREMENT This section sets out how to calculate the capital requirement for a lender, or an administrator with administered assets on its balance sheet (seeMIPRU 4.2.12R, MIPRU 4.2.18R and MIPRU 4.2.23R): | |

| (a) | is the minimum requirement of £100,000; | |

| (b) | is 1% of the amount shown as total adjusted assets at C4.5, i.e. the assets that are not subject to the credit risk requirement calculation; | |

| (c) | is the credit risk requirement as shown at line 9E in section L of the MLAR; | |

| (d) | is the total of (b) and (c); and | |

| (e) | is the capital requirement which is the higher of the fixed amount at (a) and the sum shown at (d). | |

| C5 | Capital requirements for an administrator not having administered assets on its balance sheet | |

| C5.1 | This section sets out the income-based capital requirements applicable to administrators that do not have the assets that they administer on their balance sheet. The information requirements are detailed in C5.2 – 5.5. Firms should report the following amounts from both their most recent annual financial statement and their estimated accounts for the current reporting year. | |

| C5.2 | Total income Firms should report the amount of total income in their most recent (or other) financial statements, and an estimate of income for the current reporting year. Total income should include both revenue and gains arising in the course of the ordinary activities of a firm. Revenue consists of commissions, fees, net interest income, dividends, royalties and rent. Only gains that are recorded in the profit and loss account should be included in income. What is relevant for the calculation of income is the amount of actual income generated rather than the gross cash streams of any one transaction (see MIPRU 4.3.7R). | |

| C5.3 | Relevant adjustments The following exceptional items must be deducted from the firm’s total income: | |

| (1) | profit on the sale or termination of an operation; | |

| (2) | profit arising from a fundamental reorganisation or restructuring having a material effect on the nature and focus of the firm’s operations; and | |

| (3) | profits on the disposal of fixed assets, including investments held in long-term portfolio. | |

| C5.4 | Total relevant income Is the sum of C5.2 minus C5.3. | |

| C5.5 | CAPITAL REQUIREMENT This sets out how to calculate the capital requirement for anadministrators administrator not having administered assets on its balance sheet (see MIPRU 4.2.19R): | |

| (a) | is the minimum requirement of £100,000; | |

| (b) | is 10% of the amount shown as total relevant income at C5.4 above; and | |

| (c) | is the capital requirement which is the higher of the minimum amount at (a) and the calculation shown at (b). | |

SECTION D1: LENDING – BUSINESS FLOWS AND RATES

| D1-D4 | For details of the terms ‘Residential lending to individuals’ (and regulated/unregulated), and ‘other secured loans’, see Introduction, paragraphs 4 (i) – (iv). | |||||

| D1 | Loans: Advances/Repayments – Row & Column Analysis For the two categories of loan assets, details are requested under various transaction columns that explain the transition from the previous quarter’s balances to the current quarter’s balances. | |||||

| D1 | Loans: Advances/Repayments – Transactions (columns) Advances made in quarter should include: | |||||

| (a) | instalments released in the quarter for instalment advances; | |||||

| (b) | re-advances, i.e. where previous charge cancelled; | |||||

| (c) | further advances; | |||||

| (d) | in the case of loans that have a facility to draw down extra amounts over and above the sum originally advanced, the total of any further amounts drawn down in the quarter; | |||||

| (e) | the deduction from advances made of advance cheques cancelled; | |||||

| but should exclude: | ||||||

| (f) | the amount of any loan books acquired in the quarter (which should be reported in ‘other debits/credits etc’): | |||||

| (g) | retentions imposed, which should be included as they are released; | |||||

| (h) | sundry debits, i.e. any items not approved and not included in commitments, e.g. insurance debits, fines, insurance guarantees, valuation fees, arrangement fees (unless formally treated as part of loan, that is where such amounts are repaid over the period of the loan); | |||||

| (i) | any movements on overdrafts. | |||||

| Repayment of principal should include: | ||||||

| (a) | repayment of principal including capital repayments, full or partial redemptions and the principal element of the normal monthly payment; | |||||

| (b) | mortgage receipts temporarily posted to investment accounts; | |||||

| (c) | transfers from investment accounts to mortgage accounts; | |||||

| but should exclude: | ||||||

| (d) | the amount of any loan book sold during the quarter (to be reported in ‘other debits/(credits) etc’); | |||||

| (e) | sundry credits to accounts, such as insurance premiums, fines, fees, etc; | |||||

| (f) | advance cheques cancelled; | |||||

| (g) | investment receipts temporarily posted to mortgage accounts; | |||||

| (h) | any movement in overdrafts. | |||||

| In determining the amount shown under repayment of principal, it is recognised that firms may need to estimate the amount of interest repaid where amounts repaid include both interest and principal, and/or where the amount of interest repayable is not the same as the amount charged (e.g. annual review or deferred interest schemes, or where a loan is not being fully serviced). | ||||||

Write-offs in quarter This is the amount of written off mortgage balances in the quarter (and of provisions charged to the income and expenditure account) and is to be on a basis consistent with amounts shown in the firm's published accounts as 'written off' within the analysis of changes in loss provision usually appearing as Notes to the Accounts. The amount written off may arise for example from: | ||||||

| (a) | sale of a property in possession where there is a shortfall; or | |||||

| (b) | a decision to write down the mortgage debt on a loan still on the books. This may arise where the firm has taken the view that it is certain that a loss will arise and that it is prudent to write down the mortgage debt rather than carry the full debt and an offsetting provision. Examples might include certain fraud cases, or where arrangements have been reached with the borrower to reduce the mortgage debt repayable; | |||||

| (c) | the amount should be net of any write-backs in the quarter. If there are more write-backs than write-offs the net figure should be shown as a negative. | |||||

| Other debits/(credits) and transfers (net) should include: | ||||||

| (a) | interest charged to the loan account in the period; | |||||

| (b) | interest repaid during the period; | |||||

| (c) | amounts charged to loan accounts and amounts received from borrowers in respect of such items as insurance premiums, valuation fees, and fines etc; | |||||

| (d) | mortgage balances acquired following takeover / merger; | |||||

| (e) | loan books acquired from other lenders in the quarter; | |||||

| (f) | loan books sold to other lenders in the quarter; | |||||

| (g) | loan books securitised during the quarter; | |||||

| (h) | the transfer of any securitised assets back onto the balance sheet (e.g. following the closure of a securitised pool of loans); | |||||

| (i) | transfers (net) should include any reclassified loans (e.g. where there has been a change in the use of the land on which the loan is secured to/from residential; or a change in status of loan from/to regulated/non-regulated etc); | |||||

| (j) | all movements on overdrafts (that is, net change in overdraft balances), other than write-offs. | |||||

NB: Balances on loan books acquired/sold/securitised should be as at the date of the relevant event and not be subject to any revaluation factors. Overdraft analysis (final 3 columns of D1): The term “overdraft” here and in other columns of D1, is used to cover two types of revolving credit facilities: overdrafts and credit cards. The balance at end of quarter in column 6 is further analysed into loan balances excluding overdrafts and, separately, balances on overdrafts. The final column in D1 represents the sum total, across all overdraft accounts included in the penultimate column, of the individual credit limits on each such overdraft. | ||||||

| D2 | Loans: Book movements The 'transactions in the quarter' columns are analyses of amounts already included within the 'other debits/(credits) and transfers (net)' column of section D1. | |||||

| (a) | 'loans acquired' represents balances on any relevant loan books acquired during the quarter from other lenders; | |||||

| (b) | 'loans sold' represents balances on any relevant loan book (i.e. parcel of loans) sold during the quarter to another lender; | |||||

| (c) | 'loans securitised' represents balances on any loans that the firm has securitised in the quarter. It includes balances on loans subject to securitisation transactions which should follow MIPRU 4.2.14R to MIPRU 4.2.16G. Securitised loans brought back onto the balance sheet in the quarter should also be included and the amount here should be net of them. If the amount of securitised loans brought back onto the balance sheet is greater than the securitised balance then the net figure should be reported as a negative; and | |||||

| (d) | 'other' represents the net amount of other transaction amounts included in 'other debits/(credits) and transfers (net)' in D1. | |||||

NB: As a result, D2 (item (a) – item (b) – item (c) + item (d)) should equal D1 (item ‘other debits/(credits) and transfers (net)). The final column 'balance at end quarter on loan assets subject to non-recourse funding' represents all such loan assets (and not just the amount treated as transactions in the quarter), and requires the 'gross amount' of such loan assets to be reported against relevant line item categories. Non-recourse funding can be established either by contract or in-substance. The 'gross amount' is the amount of any such loan that would be shown in a firm's published or other balance sheet as X in the example below: | ||||||

| gross loan asset | = | X | ||||

| less non-recourse funding | = | Y | ||||

| net loan asset | = | X-Y | ||||

| In the analysis here at D2, it is therefore the gross loan asset at the end of the reporting quarter that should be reported in the final column. Once securitised, it is recognised that end quarter gross balances will not necessarily remain constant (due either to borrower repayments, the possibility of any further advances, or other arrangements for 'topping up' a pool of securitised loans, etc). | ||||||

| D3 | Loans: Interest rates Basis Interest rates in this table are nominal annual rates charged to the customer on loan accounts excluding overdrafts (as defined in D1). They should ignore the effect of any interest rate swaps or other hedging contracts that might exist, and also ignore the effect of any offsetting deposit account (as for example in the case of an offset mortgage). This provides an analysis of weighted average interest rates for the loan assets reported under ’Loans excluding overdrafts’ in column 7 of D1 above. 'Interest rates at end of quarter' (columns 4, 5, and 6 of section D3) means rates applying at least throughout the last day of the quarter, so firms should not use rates which only come into operation at the beginning of the next quarter. Points to note on specific columns are: | |||||

(1) Balances at end quarter Accrued interest should be included (even though it is excluded when computing the weighted average rate). The first 'of which' analysis is designed to obtain information on balances subject to fixed rates of interest and balances subject to variable rates of interest. (The two amounts should add to the balance in column 1). For these purposes: 'fixed' means the rate of interest is fixed for a stated period. It should also include any products with a 'capped rate' (i.e. subject to a guaranteed maximum rate) and any products that are 'collared loans' (i.e. subject to a minimum and a maximum rate). Annual review or stabilised payment loans should be excluded (since the purpose is merely to smooth cash flow on variable rate loans); 'variable' includes all other interest rate bases (i.e. other than those defined above as 'fixed') applying to particular products, including those at, or at a discount or premium to, one of the firm's administered lending rates and those linked to an index. However if any such loan products are subject to a 'capped rate', then treat as 'fixed'. The second 'of which' analysis is designed to obtain information on loan balances according to whether the nominal annual interest rate charged to the customer at the quarter-end is higher than the prevailing Bank of England Base (or repo) Rate (BBR). For these purposes the BBR is that applying on the last day of the reporting quarter. The analysis is subdivided into four categories: | ||||||

| (a) | loan balances where the rate charged is less than 2% above BBR. Include here also all loan balances where the rate charged is less than BBR (as a result the sum of these four columns will equal the figure in the TOTAL column); | |||||

| (b) | loan balances where the rate charged is 2% or up to 3% above BBR; | |||||

| (c) | loan balances where the rate charged is 3% or up to 4% above BBR; | |||||

| (d) | loan balances where the rate charged is 4% or more above BBR. | |||||

| (2) Weighted average nominal annual rates | ||||||

| (a) | Interest rates reported in Table D3 provide a broad indication of market rates. They should ignore the effect of any interest rate swap or hedging. For each line item the weighted average rate should be derived as follows: | |||||

| (i) | identify the various nominal/quoted interest rates that apply to elements of this line item; then | |||||

| (ii) | for each separate nominal/quoted rate, multiply that rate by the amount of end quarter balances (excluding accrued interest) for which that rate applies; and | |||||

| (iii) | add up the results of (ii) for all the different rates for this line item; and | |||||

| (iv) | divide the total calculated in (iii) by the corresponding end quarter balance in column 1, 2 or 3 less accrued interest (against the line item concerned). | |||||

| NB: in the 'of which' analysis that requires separate reporting of weighted 'fixed' and 'variable' rates, a cross check for each row is that the weighted average nominal rate on all balances is equal to the weighted average of the reported fixed and variable rates in the subsequent two columns. | ||||||

| D3.1 – 3.8 | Other Points The interest rate to be used is the rate charged to the loan account, which in certain circumstances will differ from the interest rate 'payable' by a borrower. These circumstances include deferred interest loans, interest roll-up loans, annual review schemes or where the loan is not performing. Advances in quarter refers to the same amount as covered under 'advances in quarter' in the Loans: Advances/Repayments analysis in Section D1 above. | |||||

| D4 | Loans: Commitments (columns) Commitments made since end of previous quarter should include: | |||||

| (a) | the aggregate of formally agreed advances (whether or not the mortgage offer has been accepted by the prospective borrower), including amounts recommended for retention, all instalment elements, and further advances; | |||||

| but should exclude: | ||||||

| (b) | commitments from previous quarters that have been cancelled in the current quarter; | |||||

| (c) | retentions imposed and subsequently not released; | |||||

| (d) | instalment commitments that have not been taken up; | |||||

| (e) | advance cancellations that are not re-issued; | |||||

| (f) | sundry debits, e.g. insurance debits, fines, insurance guarantees, valuation fees, arrangement fees etc (unless formally treated as part of the loan, that is where such amounts are repaid over the period of the loan). | |||||

Cancellations in quarter Includes (b), (c), (d) and (e) above. Advances made in quarter This refers to the same amount as covered under ‘advances in quarter’ in section D1 above. Other debits/(credits) and transfers (net) This is unlikely to be needed on a routine basis. It is intended to cover less frequent events such as loan commitments acquired on merger with another firm or acquisition of a loan book; or transferred on sale of a package of loans; or where 'commitments outstanding' need adjusting for reasons not attributable to other columns. | ||||||

SECTION E: RESIDENTIAL LOANS TO INDIVIDUALS - New business profile

| E1-6 | Gross advances in quarter Covers actual advances made in the quarter. For these purposes separate advances (e.g. stage payments) made in the period on the same mortgage should count as a single advance for the 'number' column in sections E3, E4, E5 and E6. NB: 'gross advances' should be compiled on the same basis as in section D1 above and therefore relevant totals for each section in E1 to E6 should also agree with the amount of gross advances reported in D1. | |||

| E3-6 | Balances outstanding Covers balances at end of the quarter. Relevant sub-totals should agree with corresponding balances shown under ‘Loans excluding overdrafts’ in column 7 of D1. | |||

| E1/2 | By Income Multiple and LTV (Loan to Valuation ratio) The amount to be included in the table is the gross advance, but its allocation to a specific cell is determined according to income multiple and LTV which are both defined using the size of the loan (as defined below). For second charge regulated mortgage contracts, the calculation of income multiples and LTVs are to also include the outstanding balance of the first charge regulated mortgage contract and any higher priority second charge regulated mortgage contracts. | |||

| E1/2 | By Income Multiple and LTV Income multiple based on single or joint incomes For this analysis, 'income' should be taken as gross annual income before tax or any other deductions. The loan should first of all be categorised to 'single' or 'joint' income basis, and the income multiple calculated as described below: | |||

| (i) | Single income basis. This means only one person's income was taken into account when making the lending assessment/decision. The income multiple here is the total loan amount divided by the borrower's total income (total of the borrower's main income and any other reckonable income, e.g. overtime, to the extent that the firm takes such additional income into account in whole or in part). | |||

| (ii) | Joint income basis. This means that two or more persons' incomes were used in the lending assessment/decision. The income multiple here is the total loan amount divided by the aggregate income of the two or more borrowers. | |||

| (iii) | Other. This category is to be used when the loan assessment is based, only partly or not at all, on one or more persons' incomes. Thus include here: | |||

Under Single Income section (E1.6/E1.13) • Buy to let loans where the loan assessment is based on the rental yield of the property (but not buy to let loans based solely on one or more persons’ incomes which should be shown against the relevant income multiple category); • Lifetime mortgages since in most if not all instances, the concept of a supporting income is not applicable; • Other products (no current examples) | ||||

Under Joint Income section (E2.6/E2.13) • Business loans, where typically the loan assessment will be based on mixed sources of business/personal income or perhaps just on the capacity of a person’s business to support the loan; • Other products that have similar characteristics, that is where the loan assessment is based on either mixed income sources or non-personal incomes. | ||||

| (iv) | Not evidenced. This 'of which' analysis applies to loans made on the basis of one or more persons' incomes, and therefore should exclude any loans reported in "Other" (defined in (iii) above). It covers loans where: the lender has no independent documentary evidence to verify income (e.g. as provided by an employer's reference, a bank statement, a salary slip, a P60, or audited/certified accounts. | |||

For the purpose of income multiples, the multiple is of loan to income where loan is as defined below. Loan to valuation ratio LTV Should be based on the following: | ||||

| (i) | loan is defined for: | |||

| (a) | new borrowers - as the amount of actual advance or, in the case of loans where the amount advanced in the period is less than the total amount of the loan which the firm has agreed to lend (for example loans with additional drawing facilities or loans involving instalments/stage payments/retentions), is the amount of committed advance (including any committed drawing facilities); | |||

| (b) | existing borrowers - as the total amount of debt outstanding including the further advance plus any committed drawing facilities at the time of the further advance; | |||

| and will include MIG ("mortgage indemnity guarantee"), building and other insurance premiums and other sundry items if these are included in the amount advanced; | ||||

| (ii) | valuation is to be taken as the most recent valuation of the property which is subject to the mortgage (the existence of additional collateral on any other property should be ignored when calculating LTV). For these purposes, "recent valuation" can either be based on an actual valuation, or an estimated valuation using indexed valuation methodology applied to an original actual valuation. In the case of staged construction or self-build schemes, valuation means 'expected final value of the property' at the time the firm is committed to making the loan (i.e. takes the lending decision). | |||

| E3 | Credit history This seeks to categorise lending in terms of a borrower’s previous credit history, as measured at the point when the new advance is made. For these purposes, it is only necessary to establish a borrower’s credit history at a single point in time, i.e. at the time of making the loan. In practice this will usually be done at the ‘offer’ stage of making a loan. It is not intended that credit history should be reassessed after the loan has been made. However, if a further advance is made, then it will be necessary to re-assess. In particular the aim is to separately identify under the heading 'Impaired credit history', those loans where it appears that the borrower has some form of adverse credit history: | |||

| (i) | at the point when the new advance is made and the loan is reported under 'Gross advances'; | |||

| (ii) | subsequently for reporting under 'Balances outstanding', the amount of the loan at the quarter end to such a borrower (who at the point when the present loan was advanced, was deemed to have had an adverse credit history). | |||

| However, if there is subsequently a further advance on the loan (which will be reported under ‘Gross advances’ in E3), this is an occasion to re-assess the borrower’s credit history. At that stage, the total amount of the loan (including further advance) should be classified under ‘Balances outstanding’ on the basis of the credit history as determined at the time of making the further advance. This means that the further advance and total loan amount will be reported on a consistent basis. | ||||

| E3.1 | Impaired credit history If any of the following conditions are met at the time of making the loan, the borrower should be reported as having an impaired credit history: | |||

| (i) | arrears on a previous (or current) mortgage or other secured loan within the last two years, where the cumulative amount overdue at any point reached three or more monthly payments; | |||

| (ii) | arrears on a previous (or current) unsecured loan within the last two years, where the cumulative amount overdue at any point reached three or more monthly payments; | |||

| (iii) | one or more county court judgments (CCJs), with a total value greater than £500, within the last three years; | |||

| (iv) | being subject to an Individual voluntary arrangement (IVA) at any time within the last three years; | |||

| (v) | being subject to a bankruptcy order at any time within the last three years; | |||

but firms should not include technical arrears as part of the above definition. Technical arrears means circumstances where the borrower has been the victim of a banking error giving rise to late payment. NB: In (i) to (v), firms should ignore whether the borrower has subsequently paid off arrears, or has satisfied/discharged a CCJ or IVA or bankruptcy. In the case of loans involving two or more borrowers, the impaired credit test is whether any one of the borrowers individually meets any of the five listed impaired credit conditions. | ||||

| E4 | Payment type This section analyses loans in terms of how the borrower is contractually expected to service the loan, and is split into four categories: • repayment; • interest only; • combined; and • other. | |||

| E4.1 | Repayment (capital and interest) This is the traditional payment option available to borrowers. Such loans involve regular periodic payments covering interest for the period and some repayment of capital. | |||

| E4.2 | Interest only This is the type of loan which requires the borrower to make regular payments of interest only (i.e. without any obligation to make periodic payments of capital). It includes 'endowment' type loans, others having an independent ultimate repayment vehicle (e.g. PEP, ISA or pension mortgages), as well as other interest-only loans where there is either no specific ultimate repayment vehicle in place or where the lender does not formally require one to be in place. | |||

| E4.3 | Combined This section is for loans where both of the above payment types are in place (i.e. part of the loan is ‘repayment’, and part is ‘interest only’). | |||

| E4.4 | Other This category will contain loans where no regular periodic payment obligation is in place, for example secured overdraft facilities or secured credit cards, and lifetime mortgages. | |||

| E5 | By drawing facility These are loans which include an option to draw down further amounts (i.e. where, at the outset of the loan, extra drawing rights exist over and above the original amount advanced, but not those arising only in relation to previous overpayments). The drawing facility category is also meant to indicate a facility that is only exercisable by the borrower (e.g. via a cheque book, on line transaction or on demand). It would therefore not apply to situations where a loan is merely subject to retentions or stage payments, since the borrower does not have a draw-down option that they can exercise. | |||

| E5.1 | Extra drawing facility These are loans which in general are structured as follows: Example structure when flexible loan contract agreed | |||

| Amount of loan advanced | £65,000 | |||

| Amount of extra drawing facility agreed to (but not advanced at outset of loan) | £15,000 | |||

| Total loan facility up to | £80.000 | |||

| E5.1 | (a) Loans including unused facility This means the total loan facility i.e. the sum of the amount of loan advanced and the amount of extra drawing facility agreed (but not advanced at the outset of the loan): | |||

| (i) | gross advances in quarter should detail those loans that include an extra drawing facility: show the number and amount of such loans; | |||

| (ii) | loans outstanding means the end quarter balances (on original advance plus any subsequent draw downs) plus the residual amount of any unused drawing facility that remains available to the borrower: show the number and amount of such loans. | |||

| (b) Unused facility This is the amount of the extra drawing facility that has not been drawn down by the borrower: | ||||

| (i) | gross advances in quarter should detail the unused facility element of such loans: show the amount; | |||

| (ii) | loans outstanding means the end quarter balances of any unused extra drawing facility that remains available to the borrower: show the amount. | |||

(c) Net loans This can be calculated by subtracting the entry in row b) from the entry in row a). | ||||

| E5.2 | Loans with no extra drawing facility Firms should report all other loans here. | |||

| E5.3 | TOTAL This figure should be calculated as follows: | |||

| (i) | for 'Number' by adding E5.1(a) and E5.2, and | |||

| (ii) | for 'Amount' by adding E5.1(c) and E5.2. | |||

| E6 | By purpose | |||

| E6.1/2 | House purchase Loans where the borrower is purchasing a house (or flat etc). Firms should include stage payments on such transactions here and not in 'further advances'. A distinction is drawn between loans for house purchase where the purpose is for owner occupation, or for buying with a view to letting ('buy to let'). Loans for owner occupation are required to be sub divided into those to first time buyers (FTBs, that is where the tenure of the main borrower immediately before this advance was not owner-occupier) and those to other buyers. | |||

| E6.2 | Buy to let (BTL) Such loans typically involve the borrower purchasing a residential property with the intention of letting it out on a rental basis. The majority of BTL loans will be those used by the borrower to acquire a property with the intention of letting it on a commercial basis to unrelated third parties. That is to persons who, in relation to the borrower, are not ‘related persons’ (where ‘related persons’ are those set out in subsections (A), (B) and (C) of section 4 (iv) of the Introduction). These BTL loans are not regulated mortgage contracts and hence should be shown in columns 5 to 8 of E6.2 under ‘Non regulated loans’. However, where a BTL loan is used by the borrower to acquire a residential property that will be occupied by a related person, such a loan will normally be a regulated mortgage contract (providing it satisfies the other requirements of a regulated mortgage contract) and should therefore be shown in columns 1 to 4 of E6.2 under ‘Regulated loans’. An example of such a loan is where a parent buys a house or flat for use by a student son or daughter, with a plan to take in other students on a rental basis. Further advances and remortgages on any BTL loans should be included within E6.2. | |||

| E6.3 | Further advances and drawdowns A further loan (either as a further advance, or as a second charge loan where the firm has the first charge) to an existing borrower of the firm, secured on the same property; or a drawdown on a flexible mortgage. The underlying purpose of the further advance or drawdown is not relevant and could include e.g. purchasing freehold interest in a currently owned leasehold property; buying a second property on the security of the first; as a consumer loan fully secured on residential property. However, further advances and drawdowns on existing buy to let loans, and on lifetime mortgage loans should instead be reported against E6.2 and E6.6 respectively. | |||