PERG 4 Guidance on regulated activities connected with mortgages

PERG 4.1 Application and purpose

Application

Purpose of guidance

Certain activities relating to mortgages are regulated by the FCA. The purpose of this guidance is to help persons decide whether they need authorisation and, if they do, to determine the scope of the Part 4A permission for which they will need to apply.

Effect of guidance

This guidance is issued under section 139A of Act (Guidance). It is designed to throw light on particular aspects of regulatory requirements, not to be an exhaustive description of a person's obligations. If a person acts in line with the guidance in the circumstances contemplated by it, then the FCA will proceed on the footing that the person has complied with aspects of the requirement to which the guidance relates.

Rights conferred on third parties cannot be affected by guidance given by the FCA. This guidance represents the FCA's view, and does not bind the courts, for example, in relation to an action for damages brought by a private person for breach of a rule (see section 138D of the Act (Action for damages)), or in relation to the enforceability of a contract where there has been a breach of the general prohibition on carrying on a regulated activity in the United Kingdom without authorisation (see sections 26 to 29 of the Act (Enforceability of agreements)). A person may need to seek his own legal advice.

Guidance on other activities

A person may be intending to carry on activities related to other forms of investment in connection with mortgages, such as advising on and arranging an endowment policy or ISA to repay an interest-only mortgage. Such a person should also consult the guidance in PERG 2 (Authorisation and regulated activities), PERG 5 (Guidance on insurance distribution activities) and PERG 8 (Financial promotion and related activities). In addition, PERG 14 (Guidance on home reversion and home purchase activities) has guidance on regulated activities relating to home reversion plans, home purchase plans and regulated sale and rent back agreements.

PERG 4.2 Introduction

Requirement for authorisation or exemption

In most cases, any person who carries on a regulated activity in the United Kingdom by way of business must either be an authorised person or an exempt person. Otherwise, the person commits a criminal offence and certain agreements may be unenforceable. PERG 2.2 (Introduction) contains further guidance on these consequences.

Professional firms

Certain professional firms are allowed to carry on some regulated activities without authorisation so long as they comply with specified conditions (see PERG 4.14 (Mortgage activities carried on by professional firms)).

Questions to be considered to decide if authorisation is required

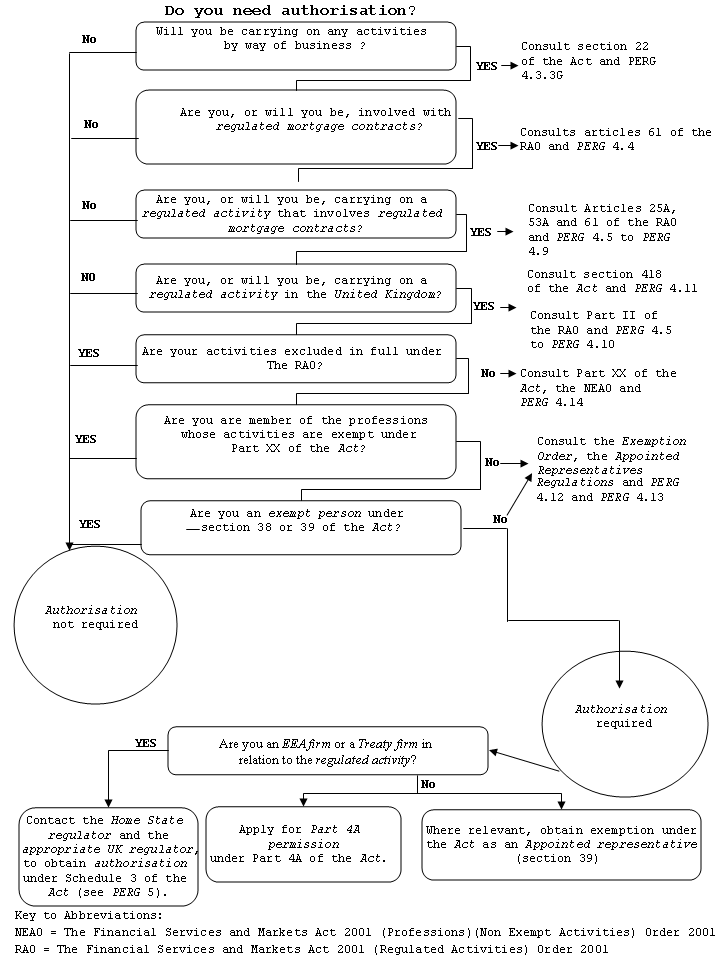

A person who is concerned to know whether his proposed activities may require authorisation will need to consider the following questions (these questions are a summary of the issues to be considered and have been reproduced, in slightly fuller form, in the flowchart in PERG 4.18):

- (1)

will I be carrying on my activities by way of business (see PERG 4.3.3 G (The business test))?

- (2)

if so, will my activities relate to regulated mortgage contracts (see PERG 4.4 (What is a regulated mortgage contract?))?

- (3)

if so, will I be carrying on any of the regulated mortgage activities (see PERG 4.5 (Arranging regulated mortgage contracts) to PERG 4.9 (Agreeing to carry on a regulated activity))?

- (4)

if so, there is the necessary link with the United Kingdom (see PERG 4.11 (Link between activities and the United Kingdom))?

- (4A)

is the only available exclusion the one for CBTL firms (see PERG 4.10B (Regulation of buy to let lending))?

- (5)

if so, will any or all of my activities be excluded (see PERG 4.5 (Arranging regulated mortgage contracts) to PERG 4.10 (Exclusions applying to more than one regulated activity))?

- (5A)

if so, is the exclusion on which I am relying disapplied because the business is subject to the Mortgage Credit Directive (see PERG 4.10A (Activities regulated under the Mortgage Credit Directive)?

- (6)

if the answer to 4A is “no” and it is not the case that all of my activities are excluded, am I a professional firm whose activities are exempted under Part XX of the Act (see PERG 4.14 (Mortgage activities carried on by professional firms))?

- (7)

if not, am I exempt as an appointed representative (see PERG 4.12 (Appointed representatives))?

- (8)

if not, am I otherwise an exempt person (see PERG 4.13 (Other exemptions))?

If a person gets as far as question (8) and the answer to that question is 'no', that person requires authorisation and should refer to the FCA website "Apply for authorisation": www.fca.org.uk/firms/authorisation/apply-authorisation for details of the application process.

However, if a person wishes to carry on CBTL business see PERG 4.10B (Regulation of buy to let lending) it may be able benefit from the exclusion for CBTL firms and be placed on the relevant register described in PERG 4.10B if:

(a) no other exclusion applies; and

(b) the answer to questions (6) to (8) is “no”.

Note that the person would need to apply to be included on the relevant register described in PERG 4.10B.

Financial promotion

An unauthorised person who intends to carry on activities connected with mortgages will also need to comply with section 21 of the Act (Restrictions on financial promotion). This guidance does not cover financial promotion s that relate to mortgages. Persons should refer to the general guidance on financial promotion in Appendix 1 to the Authorisation manual, PERG 8 (Financial promotion and related activities)) and, in particular, to PERG 8.17 (Financial promotions concerning agreements for qualifying credit).

PERG 4.3 Regulated activities related to mortgages

There are six regulated mortgage activities requiring authorisation or exemption if they are carried on in the United Kingdom. These are set out in the Regulated Activities Order. They are:

- (1)

arranging (bringing about) regulated mortgage contracts (article 25 A(1) and (2A) (Arranging regulated mortgage contracts));

- (2)

making arrangements with a view to regulated mortgage contracts (article 25A(2) (Arranging regulated mortgage contracts));

- (3)

advising on regulated mortgage contracts (article 53A (Advising on regulated mortgage contracts));

- (4)

entering into a regulated mortgage contract as lender (article 61(1) (Regulated mortgage contracts));

- (5)

administering a regulated mortgage contract where that contract is entered into by way of business on or after 31 October 2004 or the contract was entered into by way of business before that date and is a legacy CCA mortgage contract (article 61(2) (Regulated mortgage contracts)); and

- (6)

agreeing to carry on any of the above (article 64 (Agreeing to carry on specific kinds of activity)).

The scope of these activities is limited by certain exclusions contained in Parts II and III of the Regulated Activities Order. These exclusions are referred to in PERG 4.5 (Arranging regulated mortgage contracts) to PERG 4.10 (Exclusions applying to more than one regulated activity).

The business test

A person will only need authorisation or exemption if he is carrying on a regulated activity 'by way of business' (see section 22 of the Act (Regulated activities)). There are, in fact, three different forms of business test applied to the regulated mortgage activities. In the FCA's view, however, the difference in the business tests should have little practical effect.

There is power in the Act for the Treasury to change the meaning of the business test by including or excluding certain things. The Business Order has been made using this power (partly reflecting differences in the nature of the different activities). The result (which is summarised in PERG 4.3.5 G) is that:

- (1)

the 'by way of business' test in section 22 of the Act applies unchanged in relation to the activity of entering into a regulated mortgage contract;

- (2)

the 'by way of business' test in section 22 of the Act applies unchanged in relation to the activity of administering a regulated mortgage contract, but another 'by way of business' test arises because the contract being administered by way of business must itself have been entered into by way of business (see PERG 4.8.2 G); and

- (3)

in the case of arranging and advising, the effect of article 3A of the Business Order (Arranging and advising on regulated mortgage contracts) is that a person is not to be regarded as acting 'by way of business' unless he is 'carrying on the business of engaging in one or more of those activities'.

Summary of which variant of the business test applies to the different regulated mortgage activities. This table belongs to PERG 4.3.4 G.

| By way of business | Carrying on the business |

|---|---|

| Entering into a regulated mortgage contract (article 61(1)) | Arranging (bringing about) regulated mortgage contracts (article 25A(1)) and arranging (bringing about) mortgage contracts behalf of a lender (article 25A(2A)) |

| Administering a regulated mortgage contract (article 61(2)) (and the contract administered must have been entered into by way of business) | Making arrangements with a view to regulated mortgage contracts (article 25A(2)) |

| Advising on regulated mortgage contracts (article 53A) |

The 'carrying on the business' test in the Business Order is a narrower test than that of carrying on regulated activities 'by way of business' in section 22 of the Act as it requires the regulated activities to represent the carrying on of a business in their own right. Whether or not the business test is satisfied in any particular case is ultimately a question of judgement that takes account of a number of factors (none of which is likely to be conclusive). The nature of the particular regulated activity that is carried on will also be relevant to the factual analysis. The relevant factors include:

- (1)

the degree of continuity;

- (2)

the existence of a commercial element; and

- (3)

the scale of the activity and, for the 'by way of business' test, the proportion which the activity bears to the other activities carried on by the same person but which are not regulated.

In the case of the 'carrying on the business' test, these factors will need to be considered having regard to all the activities together.

The main factor that might cause an activity to satisfy the 'by way of business' test in section 22 but not the narrower 'carrying on the business' test in the Business Order is that of frequency or regularity. As a general rule, the activity would need to be undertaken with some degree of frequency or regularity to satisfy the narrower 'carrying on the business' test. Conversely, the 'by way of business' test in section 22 could be satisfied by an activity undertaken on an isolated occasion (provided that the activity would be regarded as done by 'way of business' in all other respects).

It follows that whether or not any particular person may be carrying on a regulated mortgage activity 'by way of business' will depend on his individual circumstances. However, some typical examples where the applicable business test would be likely to be satisfied are where a person:

- (1)

enters into one or more regulated mortgage contracts as lender in the expectation of receiving interest or another form of payment that would enable him to profit from his actions;

- (2)

administers a regulated mortgage contract in return for a payment of some kind (whether in cash or in kind); and

- (3)

arranges or advises on regulated mortgage contracts, or does both, on a regular basis and receives payment of some kind (whether in cash or in kind and whether from the borrower or from some other person).

Some typical examples where the business test is unlikely to be satisfied are:

- (1)

when an individual enters into or administers a one-off mortgage securing a loan to a friend or member of his family whether at market interest rates or not; or

- (2)

when a person provides a service without any expectation of reward or payment of any kind, such as advice given or arrangements made by many Citizens Advice Bureaux and other voluntary sector agencies (but see PERG 4.3.8G (3) where payment is received for advice).

PERG 4.4 What is a regulated mortgage contract?

The definition of "regulated mortgage contract"

Article 61(3)(a) of the Regulated Activities Order defines a regulated mortgage contract as a contract which, at the time it is entered into, satisfies the following conditions:

- (1)

the contract is one where a lender provides credit to an individual or trustees (the 'borrower');

- (2)

the contract provides for the obligation of the borrower to repay to be secured by a mortgage on land, where “land” for this purpose means:

- (a)

in relation to a contract entered into before IP completion day, land in the United Kingdom or, if the contract was entered into on or or after 21 March 2016, within the territory of an EEA State; and

- (b)

in relation to a contract entered into on or after IP completion day, land in the United Kingdom; and

- (a)

- (3)

at least 40% of that land is used, or is intended to be used, as or in connection with a dwelling.

This section sets out the FCA's understanding of some key concepts contained in article 61(3)(a). It should be noted that, where a contract meets the necessary requirements for both a regulated mortgage contract and a home purchase plan, it will be treated as a home purchase plan only and will not be a regulated mortgage contract. Guidance on the meaning of a home purchase plan is in PERG 14.4 (Guidance on home reversion and home purchase activities).

A contract is not a regulated mortgage contract if it is:

- (1)

a loan to a commercial borrower excluded under PERG 4.4.17 G or PERG 4.4.21 G; or

- (2)

a second charge loan by a credit union excluded under PERG 4.4.24 G; or

- (3)

a second charge bridging loan excluded under PERG 4.4.27 G;

- (4)

a CBTL credit agreement excluded as described in PERG 4.4.31G.

Provision of credit

- (1)

Article 61(3)(c) of the Regulated Activities Order states that credit includes a cash loan and any other form of financial accommodation. Although 'financial accommodation' has a potentially wide meaning, its scope is limited by the terms used in the definition of a regulated mortgage contract set out in PERG 4.4.1 G. Whatever form the financial accommodation may take, article 61(3)(a) envisages that it must include an obligation to repay on the part of the individual who receives it.

- (2)

In the FCA's view, an obligation to repay implies the existence, or the potential for the existence, of a debt owed by the individual to whom the financial accommodation is provided (the 'borrower') to the person who provides it (the 'lender').

- (3)

For example, a bank would be providing ‘credit’ which, subject to the other requirements being met, could amount to a regulated mortgage contract if it gives a guarantee that:

- (a)

creates a debt or a potential debt; and

- (b)

allows for deferred payment.

- (a)

Which borrowers?

The condition set out in PERG 4.4.1G (1) limits the range of borrowers to whom the protections of the mortgage regulation regime apply to individuals and trustees. If a company (which is not acting as a trustee) borrows money for the purpose of funding the company's business, and the loan is secured by a mortgage over the company's property, the mortgage contract is not a regulated mortgage contract. So a lender will not carry on a regulated activity by entering into that contract, nor will the lender carry on a regulated activity if it advises on, arranges or administers that contract. However, if the lender makes a loan for business purposes to an individual sole trader, or (in England and Wales) a partnership, and the loan is secured on the borrower's house or houses, the contract will be a regulated mortgage contract.

- (1)

A loan to a trustee is caught, even if the trustee or the beneficiary is not an individual.

- (2)

Therefore, it is possible that a loan to a trustee acting for a large commercial company is a regulated mortgage contract.

- (3)

In practice, the exclusions for loans to commercial borrowers (in particular, see PERG 4.4.17 G and PERG 4.4.21 G) are likely to prevent such loans from being regulated mortgage contracts.

- (4)

If:

- (a)

the loan is made to a trustee;

- (b)

the trustee is a bare trustee or nominee; and

- (c)

the beneficiary of the trust is acting for commercial purposes;

it is likely that the trustee will also be acting for commercial purposes.

- (a)

A loan to a partnership may be a loan to an individual if the partnership is made up of real people (that is natural, as opposed to legal, persons).

Date the contract is entered into

In order to meet the definition of a regulated mortgage contract, a mortgage contract must meet the conditions set out in PERG 4.4.1G (1) to PERG 4.4.1G (3) at the time it was entered into. The effect is that contracts which meet those conditions at that time remain regulated mortgage contracts throughout their remaining term, even if there are periods of time when some or all of the conditions are not satisfied. Conversely, contracts that do not start out as regulated mortgage contracts cannot subsequently become so, even if they meet all the conditions set out in PERG 4.4.1G (1) to PERG 4.4.1G (3). A person that only administers mortgage contracts which did not meet those conditions at the time they were entered into will not, therefore, need permission to administer regulated mortgage contacts.

There may, however, be instances where an existing contract, which was not a regulated mortgage contract at the time it was entered into, is replaced as a result of a variation (whether the variation is initiated by the customer or by the lender), and the new contract qualifies as a regulated mortgage contract. A person may therefore need to consider this possibility (which could affect contracts initially entered into before 31 October 2004 as well as subsequent loans) when deciding whether he needs permission to carry on any of the regulated mortgage activities.

Land

The condition set out in PERG 4.4.1G (2) means that a regulated mortgage contract must be secured on land, where "land" for this purpose means:

- (1)

in relation to a contract entered into before IP completion day, land in the United Kingdom or, if the contract was entered into on or or after 21 March 2016, within the territory of an EEA State; and

- (2)

in relation to a contract entered into on or after IP completion day, land in the United Kingdom.

Contracts which involve taking security over moveable property therefore cannot be regulated mortgage contracts. So a contract secured on a caravan will not be a regulated mortgage contract, unless the contract also involves a mortgage over the land on which the caravan stands.

Occupancy requirement

The condition set out in PERG 4.4.1G (3) means that loans secured on property which is entirely used for business purposes (such as an office block) cannot fall within the definition. However, loans secured on 'mixed use' property could be covered, provided that the occupier uses at least 40% of the total of the land as or in connection with a dwelling. Loans secured on a six-floor property, half of which was occupied by a family as their home and half let out for business purposes would therefore satisfy the definition. (Article 61(4)(b) makes it clear that 'land', in the context of a multi-storey building, means the aggregate of the floor area of each of the storeys.)

The most obvious example of a regulated mortgage contract is a loan made to an individual to enable the individual to buy a home for themselves where the loan is secured on that home. However, there is no requirement that the borrower should occupy the property. There is a requirement that at least 40% of the land should be used as a house, but no requirement that it is the borrower who uses it as a house. So, for example:

- (1)

a loan may be a regulated mortgage contract if the property on which it is secured is to be occupied by the borrower’s relatives as their home; or

- (2)

a loan may be a regulated mortgage contract if the borrower does not occupy the property on which the loan is secured and instead intends to sell the property to a third party, with the mortgage remaining on the house until then.

- (3)

However, if the borrower is acting on a commercial basis, the loan in (2) may be excluded as a loan to a commercial borrower under the exclusions in PERG 4.4.17 G or PERG 4.4.21 G.

- (4)

A buy-to-let loan secured on the property to be let is potentially a regulated mortgage contract. However, such a loan may be excluded as a loan to a commercial borrower under the exclusions referred to in (3) or under the buy-to-let exclusions described in PERG 4.4.31G and PERG 4.10B which refer to consumer borrowers.

The expression 'as or in connection with a dwelling' set out in PERG 4.4.1G (3) means that loans to buy a small house with a large garden would in general be covered. However, if at the time of entering into the contract the intention was for the garden to be used for some other purpose – for example, if it was intended that a third party were to have use of the garden – the contract would not constitute a regulated mortgage contract. Furthermore, the FCA would not regard a loan to purchase farmland and a farmhouse as constituting a regulated mortgage contract (where the farmhouse and garden amount to less than 40% of the land area), since it does not appear that the land could properly be said to be used 'in connection with' the farmhouse. The presence of the farmhouse is unconnected with the use to which the farmland is put (in contrast to a residential property's garden, which would have no existence independent of the property).

Purpose of the loan is irrelevant

The definition of regulated mortgage contract contains no reference to the purpose for which the loan is being made. So, in addition to loans made to individuals to purchase residential property, the definition is wide enough to cover other loans secured on land, such as loans to consolidate debts, or to enable the borrower to purchase other goods and services.

Type of lending

The definition of regulated mortgage contract also covers a variety of types of product. Apart from the normal mortgage loan for the purchase of property, the definition also includes other types of secured loan, such as secured overdraft facility, a bridging loan (although bridging loans described in PERG 4.4.27 G are not regulated mortgage contracts), a secured credit card facility and regulated lifetime mortgage contracts under which the borrower (usually an older person) takes out a loan where repayment of the capital (and in some cases the interest) is not required until the property is sold, usually on the death of the borrower.

Loans secured on commercial premises are not regulated mortgage contracts as the property will not be used as or in connection with a dwelling.

Type of security

A loan may be a regulated mortgage contract whether it is secured by a first, second or subsequent mortgage.

A mortgage has a wide meaning for the purpose of the definition of a regulated mortgage contract. It includes:

- (1)

a legal mortgage;

- (2)

equitable security;

- (3)

(in Scotland) a heritable security;

- (4)

[deleted]

It is possible for more than one mortgage contract to be secured by the same charge.

Exclusions for lending to commercial borrowers

A contract is excluded from the definition of regulated mortgage contract if, at the time it is entered into, it meets the following conditions:

- (1)

it meets the conditions in PERG 4.4.1G (1) to (3); and

- (2)

less than 40% of the land secured by the mortgage is used, or intended to be used, as or in connection with a dwelling by the borrower or (for credit provided to trustees) by an individual who is a beneficiary of the trust, or by a related person; and

- (3)

the agreement is entered into by the borrower wholly or predominantly for the purposes of a business carried on, or intended to be carried on, by the borrower.

The Regulated Activities Order refers to this as an “investment property loan”.

Under the Regulated Activities Order 'related person' means, in relation to the borrower or (for credit provided to trustees) a beneficiary of the trust:

- (1)

If less than 40% of the land secured by the mortgage is used, or intended to be used, as or in connection with a dwelling then the exclusion for loans to commercial borrowers described in PERG 4.4.17 G is irrelevant, as the loan falls outside PERG 4.4.1 G and so cannot be a regulated mortgage contract.

- (2)

The exclusion becomes relevant (if all the conditions in PERG 4.4.17 G are met) if at least 40% of the land secured by the mortgage is used, or intended to be used, as or in connection with a dwelling by:

- (a)

someone other than the borrower; or

- (b)

the borrower and someone else, if the percentage used by the borrower as residential property is less than 40%.

- (a)

- (3)

Therefore, the exclusion would, for example, cover a loan secured on residential property where a commercial borrower is not going to occupy any of the property but is going to sell it to a third party.

There is also an exclusion for loans to commercial borrowers secured by a second or subsequent security. A contract is excluded from the definition of regulated mortgage contract if, at the time it is entered into, it meets the following conditions:

- (1)

it meets the conditions in PERG 4.4.1G (1) to (3); and

- (2)

the lender provides the borrower with credit exceeding £25,000; and

- (3)

the mortgage ranks in priority behind one or more other mortgages affecting the land in question; and

- (4)

the agreement is entered into by the borrower wholly or predominantly for the purposes of a business carried on, or intended to be carried on, by the borrower.

The Regulated Activities Order refers to this as a “second charge business loan”.

- (1)

There is no exclusion from the £25,000 floor in PERG 4.4.21G (2) for an item entering into the total charge for credit.

- (2)

Giving time for payment of interest if the borrower gets into difficulty, does not affect the calculation of the sum as the definition relates to the time at which the contract is entered into.

- (3)

However, for example, if the credit includes a broker fee, that fee may be excluded in the calculation of the floor.

Exclusion for lending by credit unions

A contract is excluded from the definition of regulated mortgage contract if, at the time it is entered into, it meets the following conditions:

- (1)

it meets the conditions in PERG 4.4.1G (1) to (3); and

- (2)

the lender is a credit union; and

- (3)

it is a borrower-lender agreement; and

- (4)

the mortgage ranks in priority behind one or more other mortgages affecting the land in question; and

- (5)

the rate of the total charge for credit does not exceed 42.6 per cent.

The Regulated Activities Order refers to this as a “limited interest second charge credit union loan”.

The exclusion in PERG 4.4.24 G only applies if the loan meets the following conditions:

- (1)

the borrower receives timely information on the main features, risks and costs of the contract at the pre-contractual stage; and

- (2)

any advertising of the contract is fair, clear and not misleading.

Exclusion for second charge bridging loans

A contract is excluded from the definition of regulated mortgage contract if, at the time it is entered into, it meets the following conditions:

- (1)

it meets the conditions in PERG 4.4.1G (1) to (3); and

- (2)

it is a borrower-lender-supplier agreement financing the purchase of land; and

- (3)

it is used by the borrower as a temporary financing solution while changing to another financial arrangement for the land secured by the mortgage; and

- (4)

the mortgage ranks in priority behind one or more other mortgages affecting the land in question; and

- (5)

the number of payments to be made by the borrower under the contract is not more than four.

The Regulated Activities Order refers to this as a “limited payment second charge bridging loan”.

Exclusion for equitable mortgage bridging loans

A contract is excluded from the definition of regulated mortgage contract if, at the time is entered into, it meets the following conditions:

- (1)

it is a bridging loan described in PERG 4.13.6G;

- (2)

it is secured by an equitable mortgage on land; and

- (3)

it is an exempt agreement within the meaning of article 60B(3) (regulated credit agreements) of the Regulated Activities Order by virtue of article 60E(2): in summary, the lender is a local authority, or the agreement is specified in CONC App 1.3 and the lender is a person or within class of persons specified in CONC App 1.3 (see PERG 2.7.19FG(1) and (2)).

The Regulated Activities Order refers to such a contract as an ‘exempt equitable mortgage bridging loan’.

Exclusion for housing association and other housing authority loans

A contract is excluded from the definition of regulated mortgage contract if, at the time is entered into, it meets the following conditions:

- (1)

it provides for credit to be granted by a ‘housing authority’ within the meaning of article 60E of the Regulated Activities Order. The definition in article 60E includes housing associations registered under the relevant housing legislation (see PERG 2.7.19FAG);

- (2)

if entered into on or after 21 March 2016:

- (a)

it is an agreement an agreement to which section 423A(3) of the Act applies (in other words, it is an agreement listed in PERG 4.10A.5G(1) to (6); or it is a credit agreement which relates to the deferred payment, free of charge, of an existing debt and is not secured by a legal or equitable mortgage); or

- (b)

it is a bridging loan described in PERG 4.13.6G; or

- (c)

it is a restricted public loan described in PERG 4.13.7G.

- (a)

The Regulated Activities Order refers to such a contract as an ‘exempt housing authority loan’.

Certificate that borrower is not a consumer

The two exclusions for loans to commercial borrowers (PERG 4.4.17 G and PERG 4.4.21 G) depend on the borrower not being a consumer. For these purposes, if an agreement includes a declaration which:

- (1)

is made by the borrower; and

- (2)

includes:

- (a)

a statement that the agreement is entered into by the borrower wholly or predominantly for the purposes of a business carried on, or intended to be carried on, by the borrower;

- (b)

a statement that the borrower understands that the borrower will not have the benefit of the protection and remedies that would be available to the borrower under the Act if the agreement were a regulated mortgage contract under the Act; and

- (c)

a statement that the borrower is aware that if the borrower is in any doubts as to the consequences of the agreement not being regulated by the Act, then the borrower should seek independent legal advice;

- (a)

the agreement is to be presumed to have been entered into by the borrower wholly or predominantly for the purposes specified in (2)(a).

However, the presumption in PERG 4.4.29 G does not apply if, when the agreement is entered into:

- (1)

the lender (or, if there is more than one lender, any of the lenders); or

- (2)

any person who has acted on behalf of the lender (or, if there is more than one lender, any of the lenders) in connection with the entering into of the agreement;

knows, or has reasonable cause to suspect, that the agreement is not entered into by the borrower wholly or predominantly for the purposes of a business carried on, or intended to be carried on, by the borrower.

Exclusion for certain consumer buy-to-let mortgage contracts

There is an exclusion for what the RAO refers to as an “exempt consumer buy-to-let mortgage contract”. This is explained in PERG 4.10B (Regulation of buy-to-let lending).

For a buy-to-let credit agreement (described in PERG 4.10B.5G), article 61A(5) of the Regulated Activities Order says that a borrower is to be regarded as entering into an agreement, or intending to enter into an agreement, for the purposes of a business if (1) or (2) are met:

- (1)

- (a)

the borrower previously purchased, or is entering into the contract in order to finance the purchase by the borrower of, the land secured by the mortgage;

- (b)

at the time of the purchase the borrower intended that the land would be occupied as a dwelling on the basis of a rental agreement and would not at any time be occupied as a dwelling by the borrower or by a related person (see PERG 4.4.19G), or where the borrower has not yet purchased the land the borrower has such an intention at the time of entering into the contract; and

- (c)

where the borrower has purchased the land, since the time of the purchase the land has not at any time been occupied as a dwelling by the borrower or by a related person (see PERG 4.4.19G);

- (a)

- (2)

the borrower is the owner of land, other than the land secured by the mortgage, which is

- (a)

occupied as a dwelling on the basis of a rental agreement and is not occupied as a dwelling by the borrower or by a related person (see PERG 4.4.19G); or

- (b)

secured by a mortgage under a buy-to-let credit agreement.

- (a)

PERG 4.4A Mortgage contracts entered into before 21 March 2016

Prior to 21 March 2016, the definition of ‘regulated mortgage contract’ in article 61(3)(a) of the Regulated Activities Order was limited to mortgage contracts secured by a first legal mortgage (but not a second charge mortgage or an equitable mortgage) of land in the United Kingdom (rather than land in the EEA), and the regulated activity of administering a regulated mortgage contract was limited to mortgage contracts entered into on or after 31 October 2004, being the date on which mortgage regulation under the Act began. Accordingly, prior to 21 March 2016 some mortgage contracts were regulated mortgage contracts regulated under MCOB; some mortgage contracts were regulated credit agreements regulated under the CCA and, from 1 April 2014, CONC; and some mortgage contracts were outside regulation.

When the Regulated Activities Order was amended to implement the MCD, the limitations mentioned in PERG 4.4A.1AG were removed: the legislative intention was to provide a single regulatory regime for mortgage contracts under MCOB from 21 March 2016, subject to a six month transitional period for first charge mortgages entered into before 31 October 2004. Mortgage contracts that were regulated mortgage contracts before that date did not cease to be regulated mortgage contracts. But many mortgage contracts that were not regulated mortgage contracts immediately before 21 March 2016 became regulated mortgage contracts on that date provided that they met the conditions set out in PERG 4.4.1G(1) to (3), even though these conditions did not apply in that form at the time the contract was entered into.

- (1)

Mortgage contracts that potentially became regulated mortgage contracts on 21 March 2016 include, for example:

- (a)

mortgages entered into before 31 October 2004;

- (b)

second charge mortgages; and

- (c)

equitable mortgages.

- (a)

- (2)

However:

- (a)

a mortgage contract entered into before 21 March 2016, which was not already a regulated mortgage contract only became a regulated mortgage contract if it was a ‘consumer credit back book mortgage contract’ within the meaning of article 2 of the MCD Order (and see paragraph (a)(iii) of the Glossary definition of regulated mortgage contract). Briefly, this means a regulated credit agreement that would have been a regulated mortgage contract if it had been entered into on or after 21 March 2016, with the exception of certain buy-to-let mortgages (which will remain regulated credit agreements if they were regulated credit agreements at the time they were entered into);

- (b)

the exclusions set out in article 61A of the Regulated Activities Order and reflected in paragraph (a)(ii) of the Glossary definition of regulated mortgage contract replicate various consumer credit exemptions, for example equitable mortgage bridging loans; and

- (c)

the regulated activities of administering a regulated mortgage contract, advising on regulated mortgage contracts and arranging (bringing about) regulated mortgage contracts are limited, in their application to mortgage contracts entered into before 21 March 2016, to mortgage contracts which were already regulated mortgage contracts or which are ‘consumer credit back book mortgage contracts’ within the meaning of article 2 of the MCD Order (see (a)).

- (a)

PERG 4.5 Arranging regulated mortgage contracts

Definition of the regulated activities involving arranging

Article 25A of the Regulated Activities Order describes two types of regulated activities concerned with arranging regulated mortgage contracts. These are:

- (1)

making arrangements:

- (a)

for another person to enter into a regulated mortgage contract as borrower; or

- (b)

to enter into a regulated mortgage contract with a borrower on behalf of a lender; or

- (c)

for another person to vary the terms of a regulated mortgage contract entered into by that person as borrower on or after 31 October 2004 or a legacy CCA mortgage contract entered into by that person as borrower in such a way as to vary that person’s obligations under the contract; and

- (a)

- (2)

making arrangements with a view to a person who participates in the arrangements entering into a regulated mortgage contract as borrower.

The first activity (article 25A(1) and (2A)) is referred to in this guidance as arranging (bringing about) regulated mortgage contracts. Various points arise:

- (1)

It is not necessary for the potential borrower himself to be involved in making the arrangements.

- (2)

This activity is carried on only if the arrangements bring about, or would bring about a regulated mortgage contract. This is because of the exclusion in article 26 (see PERG 4.5.4 G). As explained in PERG 4.5.4A G, this exclusion does not apply to the activity in PERG 4.5.1G (1)(b).

- (3)

This activity therefore includes the activities of brokers who make arrangements on behalf of a borrower to enter into or vary a regulated mortgage contract where these arrangements go beyond merely introducing (see PERG 4.5.10 G) or advising (although giving advice may be the regulated activity of advising on regulated mortgage contracts). Such arrangements might include, for instance, negotiating the terms of the regulated mortgage contract with the eventual lender, on behalf of the borrower. It also includes the activities of certain so-called 'packagers' (see PERG 4.15 (Mortgage activities carried on by 'packagers'.)

- (4)

PERG 4.6.2 G contains examples of variations that are, in the FCA's view, within the definition of advising on regulated mortgage contracts and would also be covered by article 25A(1) arrangements.

The second activity (article 25A(2)) is referred to in this guidance as making arrangements with a view to regulated mortgage contracts. This activity is different from article 25A(1) and (2A)) because it requires a potential borrower to actively participate by utilising the arrangements to enter into a regulated mortgage contract. It does not require that the arrangements would bring about a regulated mortgage contract. Nor does it cover arrangements leading to contract variations. It includes the activities of introducers (see PERG 4.5.10 G below) introducing potential borrowers to brokers and lenders. It may also, in certain circumstances, extend to the activities of a publisher, broadcaster, or website operator, albeit subject to exclusions in the Regulated Activities Order (see PERG 4.5.5 G and PERG 4.5.6 G).

Exclusion: article 25A(1) arrangements not causing a deal

Article 26 of the Regulated Activities Order (Arrangements not causing a deal) excludes from article 25A(1) arrangements which do not bring about or would not bring about the regulated mortgage contract in question. In the FCA's view, a person brings about or would bring about a regulated mortgage contract if his involvement in the chain of events leading to the transaction is of enough importance that without that involvement it would not take place.

- (1)

Article 26 does not apply to the activity described in PERG 4.5.1G (1)(b).

- (2)

As the activity in PERG 4.5.1G (1)(b) covers a person that concludes a regulated mortgage contract with a borrower on behalf of a lender, in many cases the activity will only apply if the arrangements bring about, or would bring about, a regulated mortgage contract. Therefore, in many cases the fact that article 26 does not apply will make no difference.

- (3)

However, if a person enters into a regulated mortgage contract on behalf of a lender, that person carries out the regulated activity described in PERG 4.5.1G (1)(b). That activity is not excluded just because most of the work is done by another.

Exclusion: article 25(A)2 arrangements enabling parties to communicate

Article 27 of the Regulated Activities Order (Enabling parties to communicate) contains an exclusion that applies to arrangements which might otherwise fall within article 25A(2) merely because they provide the means by which one party to a regulated mortgage contract (or potential regulated mortgage contract) is able to communicate with other parties. Simply providing the means by which parties to a regulated mortgage contract (or potential regulated mortgage contract) are able to communicate with each other is excluded from article 25(A)2 only. This will ensure that persons such as Internet service providers or telecommunications networks are excluded if all they do is provide communication facilities (and these would otherwise be considered to be arrangements made with a view to regulated mortgage contracts).

In the FCA's view, the crucial element of the exclusion in article 27 is the inclusion of the word "merely". When a publisher, broadcaster or Internet website operator goes beyond what is necessary for him to provide his service of publishing, broadcasting or otherwise facilitating the issue of promotions, he may well bring himself within the scope of article 25A(2). Further detailed guidance relating to the scope of the exclusion in article 27 is contained in PERG 8.32.6 G to PERG 8.32.11 G.

Exclusion: article 25A(1) and (2) arranging of contracts to which the arranger is a party

Arranging a regulated mortgage contract (or contract variation) to which the arranger is to be a party is excluded from both article 25A(1) and (2) by article 28A of the Regulated Activities Order (Arranging contracts to which the arranger is a party). As a result, a person cannot both be entering into a regulated mortgage contract and arranging a regulated mortgage contract under article 25A as regards a particular regulated mortgage contract. This means that a direct sale by a mortgage lender does not involve the regulated activity of arranging but, if the transaction is completed, does involve the regulated activity of entering into a regulated mortgage contract. The FCA's rules on arranging regulated mortgage contracts, however, do apply to direct sales.

Article 28A does not apply to the activity described in PERG 4.5.1G (1)(b). This is because the activity described in PERG 4.5.1G (1)(b) is defined so that it cannot apply to an activity carried out by the lender. There is, therefore, no need to apply article 28A.

Exclusion: article 25A(1) and (2) arrangements with or through authorised persons

An unauthorised person who makes arrangements for or with a view to a regulated mortgage contract between a borrower and an authorised person, is excluded from article 25A(1) and (2), 25A(2A) and by article 29 of the Regulated Activities Order (Arranging deals with or through authorised persons) if specified conditions as to advice and remuneration are satisfied. For example, the exclusion is dependent on the borrower not receiving any advice on the regulated mortgage contract from the unauthorised person making the arrangements. Additionally, payment must not be received unless it is accounted for to the borrower (which, in the FCA's view, means that it must be paid over to, or treated as belonging to and held to the order of, the borrower).

Article 29 does not apply if applying the exclusion would take activities outside article 25A that should be regulated under the MCD. Please see PERG 4.10A (Activities regulated under the Mortgage Credit Directive) for more details.

Exclusion: article 25A(1)(b) arrangements made in the course of administration by authorised person

Article 29A of the Regulated Activities Order excludes from article 25A(1)(b) (which covers making arrangements for another person to vary the terms of a regulated mortgage contract) certain activities of an unauthorised person who is taking advantage of the exclusion from administering a regulated mortgage contract in article 62 (Exclusion: arranging administration by authorised persons) see PERG 4.8.4 G).

Exclusion: article 25A(2) arrangements and introducing

Article 33A of the Regulated Activities Order (Introducing to authorised persons) excludes from article 25A(2) arrangements under which a borrower is introduced to certain persons. Introducing is only a regulated activity under article 25A(2) as it does not of itself bring about regulated mortgage contracts (see PERG 4.5.2 G).

The exclusion applies for introductions to:

- (1)

an authorised person who has permission to carry on a regulated activity specified in article 25A (Arranging regulated mortgage contracts) or article 53A (Advising on regulated mortgage contracts) or article 61(1) (Entering into a regulated mortgage contract as lender); introducers can check the status of an authorised person and its permission by visiting the Financial Services Register at http://www.fsa.gov.uk/register/;

- (2)

an appointed representative who is appointed to carry on a regulated activity specified in article 25A or article 53A of the Regulated Activities Order; introducers can check the status of an appointed representative by visiting the FCA's register at www.fca.org.uk/firms/financial-services-register; the FCA would normally expect introducers to request and receive confirmation of the regulated activities that the appointed representative is appointed to carry on, prior to proceeding with an introduction; and

- (3)

an overseas person who carries on a regulated activity specified in article 25A (Arranging regulated mortgage contracts) or article 53A (Advising on regulated mortgage contracts) or article 61(1) (Entering into a regulated mortgage contract).

The exclusion in article 33A only applies when the introducer satisfies two conditions:

- (1)

he does not receive any money paid by the borrower in connection with any transaction that the borrower enters into with or through the person to whom the borrower is introduced as a result of the introduction, other than money payable to him on his own account; and

- (2)

before making the introduction he discloses to the borrower all relevant information described in PERG 4.5.14 G.

In the FCA's view, money payable to an introducer on his own account includes money legitimately due to him for services rendered to the borrower, whether in connection with the introduction or otherwise. It also includes sums payable to an introducer (for example, a housebuilder) by a buyer in connection with a transfer of property. For example, article 33A allows a housebuilder to receive the purchase price on a property that he sells to a borrower, whom he previously introduced to an authorised person or appointed representative to help him finance the purchase and still take the benefit of the exclusion. This is because the sums that the housebuilder receives in connection with the introduction and with the sale of his property to the borrower are both "payable to him on his own account". The housebuilder may also receive a commission from the person introduced to. He may not, however, receive any sums payable by the borrower to the person to whom the borrower is introduced, for example valuation fees, as those sums are not payable to the housebuilder on his own account.

The information that the introducer must disclose to the borrower prior to making the introduction is, where relevant:

- (1)

that he is a member of the same group as the person (N) to whom the borrower is introduced;

- (2)

details of any payment which he will receive from N, by way of fee or commission, for introducing the borrower to N; and

- (3)

an indication of any other reward or advantage arising out of his introducing to N.

In the FCA's view, details of fees or commission referred to in PERG 4.5.14G (2) does not require an introducer to provide an actual sum to the borrower, where it is not possible to calculate the full amount due prior to the introduction. This may arise in cases where the fee or commission is a percentage of the eventual loan taken out and the amount of the required loan is not known at the time of the introduction. In these cases, it would be sufficient for the introducer to disclose the method of calculation of the fee or commission, for example the percentage of the eventual loan to be made by N.

In the FCA's view, the information condition in PERG 4.5.14G (3) requires the introducer to indicate to the borrower any other advantages accruing to him as a result of ongoing arrangements with N relating to the introduction of borrowers. This may include, for example, indirect benefits such as office space, travel expenses, subscription fees and this and other relevant information may be provided on a standard form basis to the borrower, as appropriate.

The FCA would normally expect an introducer to keep a written record of disclosures made to the borrower under article 33A of the Regulated Activities Order including those cases where disclosure is made on an oral basis only.

In addition to the exclusion in article 33A, introducers may be able to take advantage of the exclusion in article 33 of the Regulated Activities Order (Introducing). This excludes arrangements where:

- (1)

they are arrangements under which persons will be introduced to another person;

- (2)

the person to whom the introduction is to be made is:

- (a)

an authorised person; or

- (b)

an exempt person acting in the course of business comprising a regulated activity in relation to which he is exempt; or

- (c)

a person who is not unlawfully carrying on regulated activities in the United Kingdom and whose ordinary business involves him in engaging in certain activities; and

- (a)

- (3)

the introduction is made with a view to the provision of independent advice or the independent exercise of discretion in relation to investments generally or in relation to any class of investments (including mortgages) to which the arrangements relate.

Other exclusions

The Regulated Activities Order contains a number of other exclusions which have the effect of preventing certain activities from amounting to regulated activities within article 25. These are referred to in PERG 4.10 (Exclusions applying to more than one regulated activity). There is also an exclusion where both the arranger and borrower are overseas, which is referred to in PERG 4.11 (Link between activities and the United Kingdom).

PERG 4.6 Advising on regulated mortgage contracts

Definition of 'advising on regulated mortgage contracts'

Article 53A of the Regulated Activities Order (Advising on regulated mortgage contracts) makes advising on regulated mortgage contracts a regulated activity. This covers advice which is both:

- (1)

given to a person in his capacity as borrower or potential borrower; and

- (2)

advice on the merits of the borrower:

- (a)

entering into a particular regulated mortgage contract (whether or not the entering into is done by way of business); or

- (b)

varying the terms of a regulated mortgage contract entered into by the borrower on or after 31 October 2004, or a legacy CCA mortgage contract entered into by the borrower, in such a way as to vary the borrower's obligations under the contract.

- (a)

In the FCA's view, the circumstances in which a person is giving advice on the borrower varying the terms of a regulated mortgage contract so as to vary his obligations under the contract include (but are not limited to) where the advice is about:

- (1)

the borrower obtaining a further advance secured on the same land as the original loan; or

- (2)

a rate switch or a product switch (that is, where the borrower does not change lender but changes the terms for repayment from, say, a variable rate of interest to a fixed rate of interest or from one fixed rate to another); or

- (3)

the borrower transferring from a repayment mortgage to an interest-only mortgage or the reverse situation.

Although advice on varying the terms of a regulated mortgage contract is not a regulated activity if the contract was entered into before 31 October 2004, unless the contract is a legacy CCA mortgage contract, there may be instances where the variation to the old contract is so fundamental that it amounts to entering into a new regulated mortgage contract (see PERG 4.4.4 G). In that case, giving the advice would be a regulated activity.

For advice to fall within article 53A as set out in PERG 4.6.1 G it must:

- (1)

relate to a particular mortgage contract (that is, one that the borrower may enter into or, in the case of advice on a variation, one that he has already entered into);

- (2)

be given to a person in his capacity as a borrower or potential borrower;

- (3)

be advice (that is, not just information); and

- (4)

relate to the merits of the borrower entering into, or varying the terms of, the contract.

Each of these aspects is considered in greater detail in PERG 4.6.5 G (Advice must relate to a particular regulated mortgage contract) to PERG 4.6.17 G (Advice must relate to the merits (of entering into as borrower or varying)). Additionally, the following should be borne in mind:

- (1)

a person may be carrying on regulated activities involving arranging, whether or not that person is advising on regulated mortgage contracts (see PERG 4.5);

- (2)

the provision of advice or information may involve the communication of a financial promotion (see PERG 8 (Financial promotion and related activities); and

- (3)

PERG 8.25 (Advice must relate to an investment which is a security or contractually based investment) to PERG 8.31 (Exclusions for advising on investments) will be relevant to any person who may be advising on other forms of investment at the same time as they advise on regulated mortgage contracts; this includes, for example, a person advising on the merits of using a particular endowment policy or ISA as the means for repaying the capital under an interest-only mortgage.

Advice must relate to a particular regulated mortgage contract

Advice will come within the regulated activity in article 53A of the Regulated Activities Order only if it relates to a particular regulated mortgage contract (or several different regulated mortgage contracts). Generic or general advice is not covered: examples of generic advice are shown in PERG 4.6.7G (but see PERG 4.6.7AG as well). Generic or general advice may, however, be a financial promotion (see PERG 8.4 (Invitation or inducement)).

PERG 4.6.21G to 4.6.25BG includes material about guiding a person through a decision tree.

Advice relates to a particular contract if it recommends that a person should take out a mortgage with ABC Building Society without (expressly or by implication) specifying any particular ABC Building Society mortgage because it is advice on the merits of specific identifiable mortgages and compared to all others. The advice is essentially saying that there is a feature of each individual ABC Building Society mortgage that makes it better than a mortgage from any other lender. Advice may be regulated even though it relates to more than one possible mortgage. Advice also relates to a particular contract if it recommends that a person should not take out a mortgage with ABC Building Society.

Typical recommendations and whether they will be regulated as advice under article 53A of the Regulated Activities Order

This table belongs to PERG 4.6.5 G and PERG 4.6.6 G.

| Recommendation | Regulated or not? |

|---|---|

| I recommend you take out the ABC Building Society 2 year fixed rate mortgage at 5%. | Yes. This is advice on a particular mortgage which the borrower could enter into. |

| I recommend you do not take out the ABC Building Society 2 year fixed rate mortgage at 5%. | Yes. This is advice on a particular mortgage which the borrower could have entered into. |

| I recommend that you take out either the ABC Building Society 2 year fixed rate mortgage at 5% or the XYZ Bank standard variable rate mortgage. | Yes. This is advice on more than one particular mortgage which the borrower could enter into. |

| I recommend you take out (or do not take out) an ABC Building Society fixed rate mortgage. | Yes. See PERG 4.6.6 G. |

| I suggest you take out (or do not take out) a mortgage with ABC Building Society. | Yes. See PERG 4.6.6 G. |

| I suggest you change (or do not change) your current mortgage from a variable rate to a fixed rate. | Yes. This is advice in respect of the advice about varying the terms of the particular mortgage that the borrower had already entered into. |

| I suggest you take out (or do not take out) a variable rate mortgage. | No. This is not advice on a particular mortgage which the borrower could enter into. |

| I recommend you take out (or do not take out) a mortgage. | No. This is not advice on a particular mortgage which the borrower could enter into. |

| I would always recommend buying a house and taking out a mortgage as opposed to renting a property. | No. This is an example of generic advice which is not advice on a particular mortgage that the borrower could enter into. |

| I recommend you do not borrow more than you can comfortably afford. | No. This is an example of generic advice. |

| If you are looking for flexibility with your mortgage I would recommend you explore the possibilities of either a flexible mortgage or an off-set mortgage. There are a growing number of lenders offering both. | No. This is an example of generic advice. |

- (1)

Although giving generic advice is generally not a regulated activity, if it is given in the course of or in preparation for a regulated activity it can form part of that regulated activity.

- (2)

For example, if a firm gives generic advice (for instance about the merits of a fixed rate mortgage rather than a variable rate mortgage) and then goes on to identify a particular fixed rate mortgage, the generic advice will form part of the regulated activity of advising on regulated mortgage contracts.

- (3)

Another example is a firm that provides generic advice to a customer or a potential customer prior to or in the course of carrying on the regulated activity of arranging (bringing about) regulated mortgage contracts for the customer. That generic advice is part of that regulated activity of arranging (bringing about) deals in investments.

Advice given to a person in their capacity as a borrower or potential borrower

For the purposes of article 53A, advice must be given to or directed at someone who is acting as borrower or potential borrower. As indicated in PERG 4.4.2 G (Which borrowers?), this means the individual or trustee to whom the credit has been provided by the lender or who is looking to obtain the credit on the security of his property. Advice given to a body corporate will not generally be caught because the advice will not concern a regulated mortgage contract, as defined. But this does not apply where the body corporate is acting as trustee.

Article 53A will not, for example, apply where advice is given to persons who receive it as:

- (1)

a lender under or administrator of a regulated mortgage contract; or

- (2)

an adviser who may use it to inform advice given by him to others; or

- (3)

a journalist or broadcaster; or

- (4)

an agent of a borrower unless appointed as the borrower's attorney and therefore entering into the regulated mortgage contract as agent (or proxy) for the borrower.

Advice will still be covered by article 53A even though it may not be given to or directed at a particular borrower (for example advice given in a periodical publication or on a website).

Advice or information

In the FCA's view, advice requires an element of opinion on the part of the adviser. In effect, it is a recommendation as to a course of action. Information on the other hand, involves objective statements of facts and figures.

- (1)

In general terms, simply giving information without making any comment or value judgement on its relevance to decisions which a borrower may make is not advice.

- (2)

The provision of purely factual information does not become regulated advice merely because it feeds into the customer’s own decision-making process and is taken into account by them.

- (3)

Regulated advice includes any communication with the customer which, in the particular context in which it is given, goes beyond the mere provision of information and is objectively likely to influence the customer’s decision whether or not to enter into a particular regulated mortgage contract or to vary an existing regulated mortgage contract.

- (4)

A key to the giving of advice is that the information:

- (a)

is either accompanied by comment or value judgement on the relevance of that information to the customer’s decision; or

- (b)

is itself the product of a process of selection involving a value judgement so that the information will tend to influence the decision.

- (a)

- (5)

Advice can still be regulated advice if the person receiving the advice:

- (a)

is free to follow or disregard the advice; or

- (b)

may receive further advice from another person before making a final decision.

- (a)

Information relating to entering into regulated mortgage contracts may often involve one or more of the following:

- (1)

an explanation of the terms and conditions of a regulated mortgage contract, whether given orally or in writing or by providing leaflets and brochures;

- (2)

a comparison of the features and benefits of one regulated mortgage contract with another;

- (3)

[deleted]

- (4)

tables that compare the interest rates and other features of different mortgages;

- (5)

leaflets or illustrations that help borrowers to decide which type of mortgage to take out;

- (6)

the provision, in response to a request from a borrower who has identified the main features of the type of mortgage he seeks, of several leaflets together with an indication that all the regulated mortgage contracts described in them have those features.

In the FCA's opinion, however, such information may take on the nature of advice if the circumstances in which it is provided give it the force of a recommendation. For example:

- (1)

a person may provide information on a selected, rather than balanced, basis that would tend to influence the decision of the borrower; and

- (2)

a person, as a result of going through the sales process, may discuss the merits of one regulated mortgage contract over another, resulting in advice to enter into or not enter into a particular one.

An explicit recommendation to enter into a particular regulated mortgage contract is likely to be advice. However, something falling short of an explicit recommendation can be advice too. Any significant element of evaluation, value judgement or persuasion is likely to mean that advice is being given.

- (1)

A person can give advice without saying (or implying) categorically that the customer should enter into a particular regulated mortgage contract. The adviser does not have to offer a definitive recommendation as to whether the customer should enter into that particular regulated mortgage contract.

- (2)

For example, saying the following can still be advice:

- (a)

“this regulated mortgage contract is a very good deal but it is your decision whether or not to enter into it”; or

- (b)

“this regulated mortgage contract is a very good deal but I am going to leave it to you to decide because I don’t know how important it is to you to have certainty about your monthly mortgage payments”.

- (a)

- (3)

The examples in (2):

- (a)

involve advice and not just information; and

- (b)

involve advice on the merits of entering into a particular regulated mortgage contract (see PERG 4.6.17G to 4.6.20G (Advice must relate to the merits (of entering into as borrower or varying)).

- (a)

One factor in deciding whether what was said by an adviser in a particular situation did or did not amount to advice is to look at the inquiry to which the adviser was responding. If a customer asks for a recommendation, any response is likely to be regarded as advice.

On the other hand, if a customer makes a purely factual inquiry it may be the case that a reply which simply provides the relevant factual information is no more than that. In this case it is relevant whether the adviser makes it clear that they do not give advice, or whether the adviser runs an advisory business.

Advice must relate to the merits (of entering into as borrower or varying)

Advice under article 53A must relate to the pros or cons of entering into a regulated mortgage contract as borrower.

An explanation of the implications under a regulated mortgage contract of, for example, exercising certain rights or failing to make interest payments on time, need not, itself, involve advice on the merits of entering into that contract or varying its terms.

Neither does advice on the merits of using a particular mortgage broker or adviser in his capacity as such amount to advice for the purposes of article 53A. It is not advice on the merits of entering into or varying the terms of a regulated mortgage contract.

Without an explicit or implicit recommendation on the merits of entering into as borrower or varying the terms of a regulated mortgage contract, advice will not fall under article 53A if it is advice on:

- (1)

the likely meaning of uncertain provisions in a regulated mortgage contract; or

- (2)

how to complete an application form; or

- (3)

the effect of contractual terms and their consequences; or

- (4)

terms which are common in the market.

Pre-sale questioning (including decision trees)

Pre-sale questioning involves putting a sequence of questions in order to extract information from a person to help them best select a mortgage that meets their needs. A decision tree is an example of pre-sale questioning. The process of going through the questions will usually narrow down the range of options that are available.

- (1)

There are two aspects of the definition of advising on regulated mortgage contracts that are particularly relevant to whether pre-sale questioning involves advising on regulated mortgage contracts:

- (a)

the fact that advice must relate to a particular regulated mortgage contract (see PERG 4.6.5G); and

- (b)

the distinction between information and advice (see PERG 4.6.13G).

- (a)

- (2)

Whether or not pre-sale questioning in any particular case is advising on regulated mortgage contracts will depend on all the circumstances.

- (3)

The pre-sale questioning process may involve identifying one or more particular regulated mortgage contracts. If so, to avoid advising on regulated mortgage contracts, the critical factor is likely to be whether the process is limited to, and likely to be perceived by the borrower as, assisting the borrower to make their own choice of product which has particular features which the borrower regards as important. The questioner will need to avoid making any judgement on the suitability of one or more products for the borrower. See also PERG 4.6.4G for other matters that may be relevant.

There is considerable potential for variation in the form, content and manner of pre-sale questioning, but there are two broad types, as described in PERG 4.6.23G and 4.6.24G.

The first type involves identifying regulated mortgage contracts based on factual matters. For example, the purpose may be to identify whether a borrower wishes to pay a fixed or variable rate of interest or the size of deposit available. There are various possible scenarios, including the following:

- (1)

the questioner may go on to identify several particular regulated mortgage contracts which match features identified by the pre-sale questioning; provided these are presented in a balanced and neutral way (for example, they identify all the matching regulated mortgage contracts, without making a recommendation as to a particular one) this need not of itself involve advising on regulated mortgage contracts;

- (2)

the questioner may go on to advise the borrower on the merits of one particular regulated mortgage contract over another; this would be advising on regulated mortgage contracts;

- (3)

the questioner may, before or during the course of the pre-sale questioning, give information that considered on its own would not involve advising on regulated mortgage contracts, but may, following the pre-sale questioning, identify one or more particular regulated mortgage contracts. The factors described in PERG 4.6.25G are relevant to deciding whether or not the questioner is advising on regulated mortgage contracts.

The second type of pre-sale questioning involves providing questions and answers incorporating opinion, judgement or recommendations. There are various possible scenarios, including the following:

- (1)

the pre-sale questioning may not lead to the identification of any particular regulated mortgage contract; in this case, the questioner has provided advice, but it is generic advice and does not amount to advising on regulated mortgage contracts; or

- (2)

the pre-sale questioning may lead to the identification of one or more particular regulated mortgage contracts. In principle, this is likely to involve advising on regulated mortgage contracts as regulated advice includes any communication with the customer which, in the particular context in which it is given, goes beyond the mere provision of information and is objectively likely to influence the customer’s decision whether or not to enter into the regulated mortgage contract (see PERG 4.6.14G). However, the factors described in PERG 4.6.25G are still relevant to deciding whether or not the questioner is advising on regulated mortgage contracts.

When the scripted pre-sale questioning identifies particular regulated mortgage contracts (see PERG 4.6.23G(3) and PERG 4.6.24G(2)), the FCA considers that it is necessary to look at the process and outcome of the pre-sale questioning as a whole in deciding whether the process involves advising on regulated mortgage contracts. Factors that may be relevant include:

- (1)

any representations made by the questioner at the start of the questioning relating to the service they are to provide;

- (2)

the context in which the questioning takes place;

- (3)

the stage in the questioning at which the opinion is offered and its significance;

- (4)

the role played by any questioner who guides a person through the pre-sale questions;

- (5)

the outcome of the questioning (whether particular regulated mortgage contracts are highlighted, how many of them, who provides them, their relationship to the questioner and so on); and

- (6)

whether the pre-sale questions and answers have been provided by, and are clearly the responsibility of, an unconnected third party, and all that the questioner has done is help the borrower understand what the questions or options are and how to determine which option applies to their particular circumstances.

A firm selling regulated mortgage contracts through its website might make its list of the regulated mortgage contracts it sells easier to search by allowing the customer to filter mortgages based on factors presented by the website and selected by the customer. Only products that meet the search criteria input by the customer are displayed.

- (1)

The filtering described in PERG 4.6.25AG might be based upon simple objective factors like price or eligibility criteria. This should not generally involve advising on regulated mortgage contracts, as explained in PERG 4.6.23G(1).

- (2)

The filtering described in PERG 4.6.25AG might, however, be based upon factors such as balancing customer preferences on price, interest rate and term. This is not a simple objective factor like price alone.

- (3)

Where all a firm is doing is listing product features of its own regulated mortgage contracts, for example by ranking objectively by the cost of any arrangement fee, that firm is unlikely to be advising on regulated mortgage contracts as long as it is clear to the customer that this objective ranking is all that the firm is doing. A description of a product’s features is not advice.

- (4)

Where a firm is describing regulated mortgage contracts offered by a third party and the product features are drawn directly from information made available to the firm by that third party, the firm is also unlikely to be advising on regulated mortgage contracts as long as it is clear to the customer that all the firm is doing is describing regulated mortgage contracts offered by a third party. A description of the product features is the factual representation of the regulated mortgage contracts and therefore likely to be information and not advice.

- (5)

Similarly, an eligibility tool can draw on information supplied by third parties (such as eligibility criteria provided by lenders, or the results of a credit reference search) to provide an indication of whether a customer is likely to qualify for mortgage lending. Where it is clear to the customer that the tool is simply applying details provided by the customer to that information, to provide a view on whether a customer’s application is likely to meet that criteria (and not giving a view on the merits of entering into that particular mortgage), the firm is unlikely to be advising on regulated mortgage contracts.

- (6)

If the input from the customer is much more extensive, and the way that those inputs interact on the website is much more complicated, than the processes described in (3) and (4), the website is not simply displaying factual information about the design of the product. In that case the production of a list of results uses an element of opinion and skill (albeit automated) in translating the customer’s input into a display of a particular product or products. Either explicitly or implicitly this is presented as meeting the customer’s requirements and wishes as input into the system. The result is that the filtering process is closer to the one in (2) than the one in (3) and so it is more likely that the firm is advising on regulated mortgage contracts.

Medium used to give advice

With the exception of periodicals, broadcasts and other news or information services (see PERG 4.6.30 G (Exclusion: periodical publications, broadcasts and websites)) the medium used to give advice should make no material difference to whether or not the advice is caught by article 53A.

Taking electronic commerce as an example, the use of electronic decision trees does not present any novel problems. The firm will be giving advice for the purpose of advising on regulated mortgage contracts only if the service goes beyond the mere provision of information and is objectively likely to influence the customer’s decision whether or not to enter into the regulated mortgage contract (see PERG 4.6.21G to PERG 4.6.25BG (Pre-sale questioning (including decision trees))).