- (1)

MIFIDPRU 7 applies to the following:

- (a)

- (b)

a UK parent entity of an investment firm group to which consolidation applies under MIFIDPRU 2.5; and

- (c)

a parent undertaking that operates a group ICARA process in accordance with MIFIDPRU 7.9.5R.

- (2)

MIFIDPRU 7.1.3R explains how each section of MIFIDPRU 7 applies to the undertakings in (1).

MIFIDPRU 7 Governance and risk management

You are viewing MIFIDPRU 7 Governance and risk management as of . MIFIDPRU 7 Governance and risk management was last updated on 23/10/2025.

MIFIDPRU 7.1 Application

01/12/2021G

01/01/2022G

The following table summarises the content of MIFIDPRU 7:

| Section | Summary of content |

|---|---|

| MIFIDPRU 7.2 | General requirements relating to a firm’s governance arrangements |

| MIFIDPRU 7.2A | Requirements relating to the risk management function |

| MIFIDPRU 7.3 | Requirements relating to risk, remuneration and nomination committees |

| MIFIDPRU 7.4 | The overall financial adequacy rule and a firm’s baseline obligations in relation to the ICARA process |

| MIFIDPRU 7.5 | The requirements of the ICARA process relating to capital and liquidity planning, stress testing and wind-down planning |

| MIFIDPRU 7.6 | Rules and guidance explaining how a firm should assess and monitor the adequacy of its own funds |

| MIFIDPRU 7.7 | Rules and guidance explaining how a firm should assess and monitor the adequacy of its liquid assets |

| MIFIDPRU 7.8 | Requirements relating to the periodic review of the ICARA process and record keeping requirements |

| MIFIDPRU 7.9 | Requirements for firms to monitor group risk and rules explaining when an investment firm group may operate a group-level ICARA process |

| MIFIDPRU 7.10 | Guidance explaining the FCA’s general approach to the SREP |

| MIFIDPRU 7 Annex 1G | General guidance on assessing potential harms that is potentially relevant to all MIFIDPRU investment firms |

| MIFIDPRU 7 Annex 2G | Additional guidance on assessing potential harms that is relevant for MIFIDPRU investment firms dealing on own account and firms with significant investments on their balance sheet |

| MIFIDPRU 7 Annex 3R to MIFIDPRU 7 Annex 6R | Notification forms |

| MIFIDPRU 7 Annex 7G | Table mapping the rules in MIFIDPRU 7 about the ICARA process to their associated guidance provisions |

23/10/2025R

MIFIDPRU 7 applies as follows:

| Section of MIFIDPRU 7 | Application to SNI MIFIDPRU investment firms | Application to non-SNI MIFIDPRU investment firms | Application at the level of an investment firm group |

|---|---|---|---|

| MIFIDPRU 7.2 (Internal governance) | Applies | Applies | Applies to the UK parent entity of an investment firm group to which consolidation applies under MIFIDPRU 2.5 |

| MIFIDPRU 7.2A (Risk management function) | Does not apply | Applies to a non-SNI MIFIDPRU investment firm that has a risk management function in accordance with SYSC 7.1.2-AR, SYSC 7.1.3R, SYSC 7.1.5R, SYSC 7.1.6R and SYSC 7.1.7R | Does not apply |

| MIFIDPRU 7.3 (Risk, remuneration and nomination committees) | Does not apply | Applies if the firm does not qualify for the exclusion in MIFIDPRU 7.1.4R | Does not apply |

| MIFIDPRU 7.4 (Overall financial adequacy rule and baseline ICARA obligations) | Applies | Applies | Applies if the investment firm group is operating a group ICARA process |

| MIFIDPRU 7.5 (Capital and liquidity planning, stress testing and wind-down planning) | Applies | Applies | Applies if the investment firm group is operating a group ICARA process |

| MIFIDPRU 7.6 (Assessing adequacy of own funds) | Applies | Applies | Applies if the investment firm group is operating a group ICARA process |

| MIFIDPRU 7.7 (Assessing adequacy of liquid assets) | Applies | Applies | Applies if the investment firm group is operating a group ICARA process |

| MIFIDPRU 7.8 (Periodic review of the ICARA process and record keeping) | Applies | Applies | Applies if the investment firm group is operating a group ICARA process |

| MIFIDPRU 7.9 (Group risks and the group ICARA process) | Applies | Applies | Applies if the investment firm group is operating a group ICARA process |

| MIFIDPRU 7.10 (The FCA’s general approach to the SREP) | Applies as guidance | Applies as guidance | Applies as guidance |

01/12/2021R

- (1)

MIFIDPRU 7.3 (Risk, remuneration and nomination committees) does not apply to a non-SNI MIFIDPRU investment firm:

- (a)

where the value of the firm’s on-balance sheet assets and off-balance sheet items over the preceding 4-year period is a rolling average of £100 million or less; or

- (b)

where:

- (i)

the value of the firm’s on-balance sheet assets and off-balance sheet items over the preceding 4-year period is a rolling average of £300 million or less; and

- (ii)

the conditions in (2) are (where they are relevant to a firm) satisfied.

- (i)

- (a)

- (2)

The conditions referred to in (1)(b)(ii) are that the:

- (a)

exposure value of the firm’s on- and off-balance sheet trading book business is equal to or less than £150 million; and

- (b)

exposure value of the firm’s on- and off-balance sheet derivatives business is equal to or less than £100 million.

- (a)

- (3)

For the purposes of paragraph (1), paragraph (4) applies where a non-SNI MIFIDPRU investment firm does not have monthly data covering the 4-year period referred to in that paragraph.

- (4)

Where this paragraph applies, a non-SNI MIFIDPRU investment firm must calculate the rolling averages referred to in paragraph (2) using the data points that it does have.

01/12/2021G

- (1)

For the purposes of MIFIDPRU 7.1.4R(3), the FCA expects a non-SNI MIFIDPRU investment firm to have insufficient data for a period only where it did not carry on any MiFID business during that period, or where (for periods prior to the application of MIFIDPRU) the firm did not record the relevant data on a monthly basis.

- (2)

Where a firm does not have all the monthly data points, the firm should use the data points it has in the way that paints the most representative picture of the period in question. For example, if a firm has monthly data for 2 years of the 4- year period, but prior to that only recorded the relevant data on a quarterly basis, the firm could sensibly calculate its rolling average by using the quarterly figure for each of the three monthly data points in each quarter.

01/12/2021R

- (1)

The amounts referred to in MIFIDPRU 7.1.4R must be calculated on an individual basis, and:

- (a)

in the case of on-balance sheet assets, in accordance with the applicable accounting framework;

- (b)

in the case of off-balance sheet items, using the full nominal value.

- (a)

- (2)

The value of the on-balance sheet assets and off-balance sheet items in MIFIDPRU 7.1.4R(1)(a) and (b) must be the arithmetic mean of the assets and items over the preceding 4 years, based on monthly data points.

- (3)

A firm may choose the day of the month that it uses for the data points in (2), but once that day has been chosen the firm may only change it for genuine business reasons.

01/12/2021R

- (1)

When calculating the amounts referred to in MIFIDPRU 7.1.4R(1)(a) and (b), a firm must use the total amount of its on-balance sheet assets and off-balance sheet items.

- (2)

A firm must calculate the exposure values referred to in MIFIDPRU 7.1.4R(2)(a) and (b) by adding together the following items:

- (a)

the positive excess of the firm’s long positions over its short positions in all trading book financial instruments, using the approach specified for K-NPR in MIFIDPRU 4.12.2R to calculate the net position for each instrument; and

- (b)

the exposure value of contracts and transactions referred to in MIFIDPRU 4.14.3R, calculated using the approach specified for K-TCD in MIFIDPRU 4.14.8R.

- (a)

- (3)

Any amounts in foreign currencies must be converted into sterling using the relevant conversion rate.

- (4)

A firm must determine the conversion rate in (3) by reference to an appropriate market rate and must record which rate was chosen.

01/12/2021G

An example of an appropriate market rate for the purposes of MIFIDPRU 7.1.7R(4) is the relevant daily spot exchange rate against sterling published by the Bank of England.

01/12/2021R

- (1)

This rule applies to a non-SNI MIFIDPRU investment firm that did not meet the conditions in MIFIDPRU 7.1.4R(1)(a) or (b) but subsequently does.

- (2)

MIFIDPRU 7.3 (Risk, remuneration and nomination committees) ceases to apply to the firm in (1) if:

- (3)

The notification in (2)(b) must be submitted through the online notification and application system using the form in MIFIDPRU 7 Annex 3R.

01/12/2021G

The effect of MIFIDPRU 7.1.9R(2)(a) is that a firm may move between meeting the conditions in MIFIDPRU 7.1.4R(3)(a) and (b) during the 6-month period.

01/12/2021R

Where a non-SNI MIFIDPRU investment firm has met the conditions in MIFIDPRU 7.1.4R(1)(a) or (b) but then ceases to do so, it must comply with MIFIDPRU 7.3 within 6 months from the date on which the firm ceased to meet the conditions.

01/12/2021R

- (1)

Where a non-SNI MIFIDPRU investment firm ceases to meet the conditions in MIFIDPRU 7.1.4R(1)(a) or (b), it must promptly notify the FCA.

- (2)

The notification in (1) must be submitted through the online notification and application system using the form in MIFIDPRU 7 Annex 3R.

01/12/2021G

Where a firm ceases to meet the conditions in MIFIDPRU 7.1.4R(1)(a) or (b), but subsequently meets the conditions again within a period of 6 months, the firm will still be subject to MIFIDPRU 7.3 6 months after the date on which it first ceased to meet the conditions. The firm will only cease to be subject to MIFIDPRU 7.3 where it meets the conditions in MIFIDPRU 7.1.9R.

MIFIDPRU 7.2 Internal governance

01/12/2021R

- (1)

A MIFIDPRU investment firm must have robust governance arrangements, including:

- (a)

a clear organisational structure with well defined, transparent and consistent lines of responsibility;

- (b)

effective processes to identify, manage, monitor and report the risks the firm is or might be exposed to, or the firm poses or might pose to others; and

- (c)

adequate internal control mechanisms, including sound administration and accounting procedures.

- (a)

- (2)

The arrangements in (1) must:

- (a)

be appropriate and proportionate to the nature, scale and complexity of the risks inherent in the business model and the activities of the firm; and

- (b)

be compatible with the requirements in the FCA Handbook relating to risk management and internal governance, for example those in MIFIDPRU 7 and SYSC, that apply to the firm.

- (a)

01/12/2021G

When establishing and maintaining the arrangements in MIFIDPRU 7.2.1R(1), a firm should consider at least the following:

- (1)

the requirements that apply to the firm under MIFIDPRU 7 and SYSC 19G (MIFIDPRU Remuneration Code);

- (2)

the legal structure of the firm, including its ownership and funding structure;

- (3)

- (4)

the type of activities for which the firm is authorised, including the complexity and volume of those activities;

- (5)

the business model and strategy of the firm, including its risk strategy, risk appetite and risk profile;

- (6)

the types of client the firm has;

- (7)

the outsourced functions and distribution channels of the firm; and

- (8)

the firm’s existing IT systems, including continuity systems.

Governance for risk management

01/01/2022R

- (1)

The management body of a MIFIDPRU investment firm has overall responsibility for risk management. It must devote sufficient time to the consideration of risk.

- (2)

The management body of a MIFIDPRU investment firm must be actively involved in, and ensure that adequate resources are allocated to, the management of all material risks, including the valuation of assets, the use of external ratings and internal models relating to those risks.

- (3)

A MIFIDPRU investment firm must establish reporting lines to the management body that cover all material risks and risk management policies and changes thereof.

01/01/2022R

- (1)

A MIFIDPRU investment firm must ensure that the management body in its supervisory function and any risk committee that has been established have adequate access to information on the risk profile of the firm and, if necessary and appropriate, to the risk management function and to external expert advice.

- (2)

The management body in its supervisory function and any risk committee that has been established must determine the nature, the amount, the format, and the frequency of the information on risk which they are to receive.

MIFIDPRU 7.2A Risk management function

23/10/2025R

MIFIDPRU 7.2A.2R and MIFIDPRU 7.2A.3R apply to a non-SNI MIFIDPRU investment firm that has a risk management function in accordance with SYSC 7.1.2-AR, SYSC 7.1.3R, SYSC 7.1.5R, SYSC 7.1.6R and SYSC 7.1.7R.

01/01/2022R

- (1)

A firm must ensure that its risk management function is independent from its operational functions and has sufficient authority, stature, resources and access to the management body.

- (2)

The risk management function in (1) must ensure that all material risks are identified, measured and properly reported. It must be actively involved in elaborating the firm’s risk strategy and in all material risk management decisions, and it must be able to deliver a complete view of the whole range of risks of the firm.

- (3)

A firm in (1) must ensure that its risk management function is able to report directly to the management body in its supervisory function, independent from senior management, and that it can raise concerns and warn the management body, where appropriate, where specific risk developments affect or may affect the firm, without prejudice to the responsibilities of the management body in its supervisory and/or managerial functions.

01/01/2022R

The head of the risk management function must be an independent senior manager with distinct responsibility for the risk management function. Where the nature, scale and complexity of the activities of the MIFIDPRU investment firm do not justify a specially appointed person, another senior person within the firm may fulfil that function, provided there is no conflict of interest. The head of the risk management function must not be removed without prior approval of the management body and must be able to have direct access to the management body where necessary.

MIFIDPRU 7.3 Risk, remuneration and nomination committees

Risk committee

01/01/2022R

- (1)

Subject to (2), a non-SNI MIFIDPRU investment firm to which this rule applies must establish a risk committee.

- (2)

Subject to (3), a firm must ensure that:

- (a)

at least 50% of the members of the risk committee are members of the management body who do not perform any executive function in the firm; and

- (b)

the chair of the risk committee is a member of the management body who does not perform any executive function in the firm.

- (a)

- (3)

The requirements in (2) do not apply to a firm that, solely because of its legal structure, cannot have members of the management body who do not perform any executive function in the firm.

- (4)

Members of the risk committee must have the appropriate knowledge, skills and expertise to fully understand, manage and monitor the risk strategy and the risk appetite of the firm.

- (5)

The risk committee must advise the management body on the firm's overall current and future risk appetite and strategy and assist the management body in overseeing the implementation of that strategy by senior management.

- (5A)

In order to assist in the establishment of sound remuneration policies and practices, the risk committee must, without prejudice to the tasks of the remuneration committee, examine whether incentives provided by the remuneration system take into consideration risk, capital, liquidity and the likelihood and timing of earnings.

- (6)

Notwithstanding the role of the risk committee, the management body of a firm has overall responsibility for the firm’s risk strategies and policies.

01/12/2021G

- (1)

MIFIDPRU 7.3.1R(2) only applies to firms that are required to establish a risk committee under MIFIDPRU 7.3.1R(1).

- (2)

The chair may be included for the purposes of calculating the 50% referred to in MIFIDPRU 7.3.1R(2)(a).

- (3)

Where a firm has established a risk committee, its responsibilities should typically include:

- (a)

providing advice to the firm's management body on risk strategy, including the oversight of current risk exposures of the firm, with particular, but not exclusive, emphasis on prudential risks;

- (b)

developing proposals for consideration by the management body in respect of overall risk appetite and tolerance, as well as the metrics to be used to monitor the firm’s risk management performance;

- (c)

overseeing and challenging the design and execution of stress and scenario testing;

- (d)

overseeing and challenging the day-to-day risk management and the executive’s oversight arrangements;

- (e)

overseeing and challenging due diligence on risk issues relating to material transactions and strategic proposals that are subject to approval by the management body;

- (f)

providing advice to the firm’s remuneration committee, as appropriate, in relation to the development, implementation and review of remuneration policies and practices that are consistent with, and promote, effective risk management;

- (g)

providing advice, oversight and challenge necessary to embed and maintain a supportive risk culture throughout the firm.

- (a)

Remuneration committee

01/12/2021R

- (1)

Subject to (2), a non-SNI MIFIDPRU investment firm to which this rule applies must establish a remuneration committee.

- (2)

The obligation in (1) will be deemed to be satisfied where:

- (a)

the non-SNI MIFIDPRU investment firm is part of an investment firm group that is subject to prudential consolidation in accordance with MIFIDPRU 2.5; and

- (b)

the UK parent entity has established a remuneration committee that:

- (i)

meets the requirements of MIFIDPRU 7.3.3R(3) (read in conjunction with MIFIDPRU 7.3.3R(4));

- (ii)

has the power to comply with those obligations on behalf of the non-SNI MIFIDPRU investment firm; and

- (iii)

has members with the appropriate knowledge, skills and expertise in relation to the non-SNI MIFIDPRU investment firm.

- (i)

- (a)

- (3)

Subject to (4), a firm must ensure that:

- (a)

at least 50% of the members of the remuneration committee are members of the management body who do not perform any executive function in the firm; and

- (b)

the chair of the remuneration committee is a member of the management body who does not perform any executive function in the firm.

- (a)

- (4)

The requirements in (3) do not apply to a firm that, solely because of its legal structure, cannot have members of the management body who do not perform any executive function in the firm.

- (5)

A firm must ensure that the remuneration committee is constituted in a way that enables it to exercise competent and independent judgment on remuneration policies and practices and the incentives created for managing risk, capital and liquidity.

- (6)

The remuneration committee must be responsible for preparing decisions regarding remuneration, including decisions which have implications for the risk and risk management of the firm and which are to be taken by the management body.

- (7)

When preparing the decisions, the remuneration committee must take into account the public interest and the long-term interests of shareholders, investors and other stakeholders in the firm.

01/12/2021G

- (1)

MIFIDPRU 7.3.3R(3) only applies to firms that are required to establish a remuneration committee under MIFIDPRU 7.3.3R(1).

- (2)

The chair may be included for the purposes of calculating the 50% referred to in MIFIDPRU 7.3.3R(3)(a).

Nomination committee

01/12/2021R

- (1)

A non-SNI MIFIDPRU investment firm to which this rule applies must establish a nomination committee.

- (2)

Subject to (3), a firm must ensure that:

- (a)

at least 50% of the members of the nomination committee are members of the management body who do not perform any executive function in the firm; and

- (b)

the chair of the nomination committee is a member of the management body who does not perform any executive function in the firm.

- (a)

- (3)

The requirements in (2) do not apply to a firm that, solely because of its legal structure, cannot have members of the management body who do not perform any executive function in the firm.

- (4)

A firm must ensure that the nomination committee:

- (a)

is able to use any forms of resources the nomination committee deems appropriate, including external advice; and

- (b)

receives appropriate funding.

- (a)

01/12/2021G

- (1)

MIFIDPRU 7.3.5R(2) only applies to firms that are required to establish a nomination committee under MIFIDPRU 7.3.5R(1).

- (2)

The chair may be included for the purposes of calculating the 50% referred to in MIFIDPRU 7.3.5R(2)(a).

Establishing committees at group level

01/12/2021G

- (1)

A firm may apply to the FCA for a modification under section 138A of the Act to permit the firm to establish a risk committee, remuneration committee, or nomination committee at group level instead of complying with the requirement on an individual basis.

- (2)

The FCA may grant a modification under section 138A of the Act if:

- (3)

To be satisfied that granting the modification would not affect the advancement of any of the FCA’s objectives under (2)(b), the FCA would normally expect the firm to demonstrate that the committee established at group level:

- (a)

meets the composition requirements in MIFIDPRU 7.3.1R(2), MIFIDPRU 7.3.3R(3) or MIFIDPRU 7.3.5R(2), as applicable; and

- (b)

has members with the appropriate knowledge, skills and expertise in relation to the firm subject to the requirement to establish a committee.

- (a)

MIFIDPRU 7.4 Internal capital adequacy and risk assessment (ICARA) process: overview and baseline obligations

01/12/2021R

This section applies to a MIFIDPRU investment firm.

Purpose

01/12/2021G

MIFIDPRU 7.4 to MIFIDPRU 7.9 contain rules and guidance which supplement the overarching requirements for MIFIDPRU investment firms under:

- (1)

the appropriate resources threshold condition in Schedule 6 to the Act (as explained in COND 2.4) under which a firm must have appropriate resources in relation to the regulated activities that it carries on; and

- (2)

Principle 4 (Financial prudence) under which a firm must maintain adequate financial resources.

01/12/2021G

- (1)

The overall purpose of the rules in MIFIDPRU 7.4 to MIFIDPRU 7.9, together with the other requirements in MIFIDPRU, is to ensure that a MIFIDPRU investment firm:

- (a)

has appropriate systems and controls in place to identify, monitor and, where proportionate, reduce all potential material harms that may result from the ongoing operation of its business or winding down its business; and

- (b)

holds financial resources that are adequate for the business it undertakes.

- (a)

- (2)

The requirement for adequate financial resources is designed to achieve 2 key outcomes for MIFIDPRU investment firms:

- (a)

to enable a firm to remain financially viable throughout the economic cycle, with the ability to address any potential material harms that may result from its ongoing activities (including both regulated activities and unregulated activities); and

- (b)

to enable the firm to conduct an orderly wind-down while minimising harm to consumers or to other market participants, and without threatening the integrity of the wider UK financial system.

- (a)

- (3)

The rules and guidance in MIFIDPRU 7.4 to MIFIDPRU 7.9 build on the FCA’s general approach to assessing the adequacy of financial resources explained in Finalised Guidance FG20/1. Firms should also refer to that guidance when considering their obligations under those sections of MIFIDPRU.

01/12/2021G

The FCA recognises that:

- (1)

there is a vast range of potential harms and it will not be possible for the FCA or firms to eliminate all potential risks and sources of harm;

- (2)

the FCA and firms should focus on material harms, adopting a proportionate and risk-based approach to each firm’s business and operating model; and

- (3)

some firms may still fail, but the FCA and firms should aim to ensure that any wind-down of those firms occurs in an orderly manner, minimising the impact on consumers and the wider market.

Proportionality and application to different business models

01/12/2021G

Although all MIFIDPRU investment firms are subject to the appropriate resources threshold condition and Principle 4, the practical steps that a firm must take to meet these requirements will vary according to the firm’s business model and operating model. Therefore, a firm with a more complex business or operating model should generally take a more detailed approach to the monitoring and management of a wider range of potential harms than a smaller firm carrying on simpler activities.

01/12/2021G

MIFIDPRU 7.4 to MIFIDPRU 7.8 contain a set of core requirements that every MIFIDPRU investment firm should incorporate into its ICARA process. This does not mean that the manner in which each firm implements these core requirements will be identical. When considering the appropriate way to satisfy these core requirements, a firm should focus on the potential material harms that may arise:

- (1)

from the ongoing operation of its business; and

- (2)

during a wind-down of its business.

Overall financial adequacy rule

01/12/2021R

- (1)

A firm must, at all times, hold own funds and liquid assets which are adequate, both as to their amount and their quality, to ensure that:

- (a)

the firm is able to remain financially viable throughout the economic cycle, with the ability to address any material potential harm that may result from its ongoing activities; and

- (b)

the firm’s business can be wound down in an orderly manner, minimising harm to consumers or to other market participants.

- (a)

- (2)

The requirement in (1) is known as the overall financial adequacy rule.

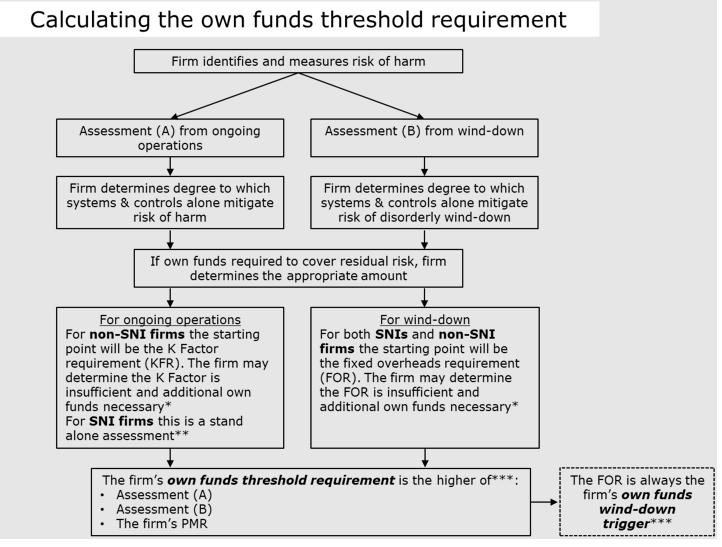

01/12/2021G

- (1)

The overall financial adequacy rule establishes the standard that the FCA applies to determine whether a MIFIDPRU investment firm has adequate financial resources. The amount and quality of own funds and liquid assets that each firm must hold will vary according to its business model and operating model, the environment in which it operates and the nature of its internal systems and controls.

- (2)

The remainder of this section explains the basic requirements of the ICARA process. The ICARA process is the collective term for the internal systems and controls that a firm must operate to identify and manage potential material harms that may arise from the operation of its business, and to ensure that its operations can be wound down in an orderly manner.

- (3)

A firm should use the ICARA process to identify whether it complies with the overall financial adequacy rule. The focus of the ICARA process is on identifying and managing risks that may result in material harms. Depending on the nature of the potential harms identified, the only realistic option to manage them and to comply with the overall financial adequacy rule may be to hold additional own funds or additional liquid assets above the firm’s own funds requirement or basic liquid assets requirement. However, in other cases, there may be more appropriate or effective ways to manage the potential harms. MIFIDPRU 7.4.16G contains further guidance on reducing the risk of material potential harms.

- (4)

MIFIDPRU 7.6 contains rules and guidance about how a firm should use the ICARA process to assess the own funds that the firm requires to comply with the overall financial adequacy rule.

- (5)

MIFIDPRU 7.7 contains rules and guidance about how a firm should use the ICARA process to assess the liquid assets that the firm requires to comply with the overall financial adequacy rule.

- (6)

MIFIDPRU 7.10 contains guidance on how the FCA will normally conduct a SREP on a firm’s ICARA process or may conduct a thematic review of a sector in which multiple firms are active. Where the FCA considers that the firm’s ICARA process has not adequately identified and managed the risks of material harm, the FCA may require the firm to take corrective action. In appropriate cases, this may include requiring the firm to hold additional own funds or liquid assets to ensure that the firm is complying with the overall financial adequacy rule. The FCA may also take supervisory action in connection with the prudential requirements of a MIFIDPRU investment firm outside the context of a SREP. Where the FCA has conducted a sectoral review, it may impose additional requirements on some or all firms that are active in the relevant sector.

ICARA process: baseline obligations

01/12/2021R

- (1)

A firm must have in place appropriate systems and controls to identify, monitor and, if proportionate, reduce all material potential harms:

- (2)

If any material potential harms remain after a firm has implemented the systems and controls in (1), the firm must assess whether to:

- (a)

hold additional own funds to address the harms in accordance with MIFIDPRU 7.6.2R; and

- (b)

hold additional liquid assets to address the harms in accordance with MIFIDPRU 7.7.2R.

- (a)

- (3)

The requirements in this rule apply to a firm’s entire business, including:

- (a)

all regulated activities, irrespective of whether they are MiFID business; and

- (b)

- (a)

- (4)

The systems, controls and procedures operated by a firm to comply with the requirements in this rule are known as the ICARA process.

01/12/2021R

A firm’s ICARA process must be proportionate to the nature, scale and complexity of the business carried on by the firm.

01/12/2021R

A firm must ensure that its ICARA process complies with the requirements in MIFIDPRU 7.4 to MIFIDPRU 7.8 in a consistent and coherent manner.

01/12/2021G

- (1)

MIFIDPRU 7.4.11R requires a firm to ensure that the inputs to, analyses applied by, and conclusions arising from, its ICARA process are properly linked and reflect a consistent and coherent analysis of the firm’s business and operating model.

- (2)

The following are examples of the consistency and coherence required by the ICARA process:

- (a)

the potential material harms that the firm identifies under MIFIDPRU 7.4.13R are consistent with the firm’s articulation of its business model and strategy under MIFIDPRU 7.5.2R(1) and with the firm’s stated risk appetite under MIFIDPRU 7.5.2R(2);

- (b)

the firm’s analysis under MIFIDPRU 7.5.2R(4) of the own funds and liquid assets that are necessary to comply with the overall financial adequacy rule is consistent with:

- (i)

the potential impact of the potential material harms that the firm identifies under MIFIDPRU 7.4.13R;

- (ii)

the firm’s projections of its future requirements under MIFIDPRU 7.5.2R(4); and

- (iii)

the impact of the stressed scenarios that the firm has identified under MIFIDPRU 7.5.2R(5);

- (i)

- (c)

the potential recovery actions specified by the firm under MIFIDPRU 7.5.5R(2) are consistent with the firm’s projections of its future requirements under MIFIDPRU 7.5.2R(4) and the potential stressed scenarios that the firm has identified under MIFIDPRU 7.5.2R(5);

- (d)

the firm’s wind-down planning under MIFIDPRU 7.5.7R is consistent with the levels of own funds and liquid assets that the firm has assessed would be necessary to wind-down the firm for the purposes of the overall financial adequacy rule and with the firm’s assessment of the potential harms that might result from winding down its business under MIFIDPRU 7.4.13R; and

- (e)

the firm's wind-down planning is consistent with the potential recovery actions specified by the firm under MIFIDPRU 7.5.5R(2) and the circumstances in which the firm has concluded that no further recovery actions would be feasible or desirable.

- (a)

ICARA process: identifying harms

01/12/2021R

As part of its ICARA process, a firm must assess its business model and identify all material harms that could result from:

01/12/2021G

When assessing potential material harms for the purpose of MIFIDPRU 7.4.13R, the FCA considers that the following non-exhaustive list of considerations will be relevant:

- (1)

the level of detail required in the assessment is likely to vary depending on the complexity of the business and operating model. More complex business and operating models are likely to involve a wider range of potential material harms and so will generally require a more detailed assessment;

- (2)

the obligation under MIFIDPRU 7.4.13R is to identify all material harms that could result from the firm’s business, even if those harms can be appropriately mitigated. It is important that a firm starts by identifying all potential material harms that could arise from its business and operating model. The issue of how the identified harms can be mitigated should be considered separately, including assessing under MIFIDPRU 7.6 and 7.7 whether the firm should hold additional own funds and liquid assets;

- (3)

the potential for harm may evolve throughout the course of an economic cycle. Therefore, the assessment should consider how the risk of harm may develop in the future, rather than simply performing a static assessment based on current economic circumstances;

- (4)

risks to the firm itself may result in an increased risk of harm to the firm’s clients or counterparties and therefore should form part of the assessment. For example, if the firm is affected by a significant disruption or suffers a significant loss, this may prevent the firm from providing important services to clients or from being able to meet its liabilities to counterparties. Significant and unexpected financial losses sustained by a firm may also decrease the financial resources available to the firm to address other potential harms and may increase the risk of disorderly wind-down and sudden disruption of services to the firm’s clients; and

- (5)

firms should refer to the guidance in Finalised Guidance FG20/1 on “Identifying and assessing the risk of harm” when assessing the impact of potential harms.

01/12/2021G

(1)

MIFIDPRU 7 Annex 1 contains additional guidance on identifying potential material harms that are relevant to the business models of most firms.

(2)

MIFIDPRU 7 Annex 2 contains additional guidance on identifying potential material harms that are likely to be relevant to firms that deal on own account or hold significant investments on their balance sheets. This guidance is intended to apply in addition to the general guidance in MIFIDPRU 7 Annex 1.

(3)

The FCA may issue further guidance or publish additional information to reflect its observations of how firms are implementing the ICARA process or to take into account developments in relation to particular products or sectors. Firms should consider any additional guidance or information that the FCA has published when applying the requirements in this section.

ICARA process: risk mitigation

01/12/2021G

- (1)

The ICARA process is an internal risk management process that a MIFIDPRU investment firm must operate on an ongoing basis. As part of that process, a firm should consider whether the risk of material potential harms can be reduced through proportionate measures (other than holding additional financial resources) and, if so, whether it is appropriate to implement the measures. The nature of any potential measures will vary depending on the firm’s business and operating model. Examples may include implementing additional internal systems and controls, strengthening governance and oversight processes or changing the manner in which the firm conducts certain business. A firm will need to form a judgement about what is appropriate and proportionate for its particular circumstances. That judgement will be informed by the firm’s risk appetite.

- (2)

A firm must assess whether it should hold additional own funds or additional liquid assets to mitigate any material potential harms that it has identified. This may be the case where the firm cannot identify other appropriate, proportionate measures to mitigate harms, or where it has applied these measures, but a residual risk of material harm remains. Any assessment must be realistic and based on severe but plausible assumptions.

MIFIDPRU 7.5 ICARA process: capital and liquidity planning, stress testing, wind-down planning and recovery planning

01/12/2021R

This section applies to a MIFIDPRU investment firm.

Business model assessment and capital and liquidity planning

01/12/2021R

As part of its ICARA process, a firm must:

- (1)

have a clearly articulated business model and strategy;

- (2)

have a clearly articulated risk appetite that is consistent with the business model and strategy identified under (1);

- (3)

identify any material risks of misalignment between the firm’s business model and operating model and the interests of its clients and the wider financial markets, and evaluate whether those risks have been adequately mitigated;

- (4)

consider on a forward-looking basis the own funds and liquid assets that will be required to meet the overall financial adequacy rule, taking into account any planned future growth; and

- (5)

consider relevant severe but plausible stresses that could affect the firm’s business and consider whether the firm would still have sufficient own funds and liquid assets to meet the overall financial adequacy rule.

Stress testing and reverse stress testing requirement

01/12/2021G

MIFIDPRU 7.5.2R(5) requires a firm to use stress testing to identify whether it holds sufficient own funds and liquid assets. Firms should refer to Finalised Guidance FG20/1 for specific guidance on the FCA’s expectations in relation to stress testing.

01/12/2021G

- (1)

As part of their business model assessment and capital and liquidity planning under MIFIDPRU 7.5.2R, firms with more complex businesses or operating models should also undertake:

- (a)

more in-depth stress testing of their business model and strategy; and

- (b)

reverse stress testing.

- (a)

- (2)

Firms should refer to MIFIDPRU 7 Annex 1.15G to MIFIDPRU 7 Annex 1.20G for additional information about the FCA’s expectations in relation to more in-depth stress testing and reverse stress testing.

- (3)

The FCA may request individual firms to carry out more in-depth stress testing or reverse stress testing. In appropriate cases, the FCA will consider whether it is necessary or desirable to impose a requirement on a firm to carry out such stress testing. This may involve inviting a firm to apply for the voluntary imposition of a requirement under section 55L(5) of the Act or the FCA imposing a requirement on the FCA’s own initiative under section 55L(3) of the Act.

Recovery actions

01/12/2021R

As part of its ICARA process, a firm must identify:

- (1)

levels of own funds and liquid assets that the firm considers, if reached, may indicate that there is a credible risk that the firm will breach its threshold requirements; and

- (2)

potential recovery actions that the firm would expect to take:

- (a)

to avoid a breach of the firm’s threshold requirements where the firm’s own funds or liquid assets fall below the levels identified in (1); and

- (b)

to restore compliance with its threshold requirements if the firm were to breach its threshold requirements during a period of financial difficulty.

- (a)

01/12/2021G

- (1)

When a firm is considering potential recovery actions that the firm may take for the purposes of MIFIDPRU 7.5.5R, it should consider at least the following:

- (a)

the governance arrangements of the firm, and in particular which individuals will be responsible for taking the relevant decisions within the required timeframe;

- (b)

the key business lines operated by the firm and the critical functions that the firm will need to maintain, and the steps necessary to ensure that these can continue to operate;

- (c)

the level of own funds and liquid assets that the firm is likely to need to restore compliance with the threshold requirements;

- (d)

the options available to the firm to raise additional own funds or liquid assets;

- (e)

the options available to the firm to conserve existing own funds or liquid assets;

- (f)

any significant risks that may arise in connection with proposed recovery actions; and

- (g)

any material impediments that may exist to implementing proposed recovery actions and whether these can be resolved or mitigated.

- (a)

- (2)

A firm should adopt a proportionate approach to identifying potential recovery actions, taking into account the nature, scale and complexity of the firm’s business and operating model. The actions that the firm proposes must be credible and justifiable, taking into account the circumstances in which the actions may be likely to be required.

Wind-down planning and wind-down triggers

01/12/2021R

As part of its ICARA process, a firm must:

01/12/2021G

When carrying out a wind-down planning assessment under MIFIDPRU 7.5.7R and determining the timeline and any required actions, a firm should refer to the guidance in the FCA’s Wind-Down Planning Guide and in Finalised Guidance FG20/1.

01/12/2021R

- (1)

A firm must use its wind-down analysis under MIFIDPRU 7.5.7R to assess the amount of own funds and liquid assets that would be required to ensure an orderly wind-down of its business for the purposes of the overall financial adequacy rule.

- (2)

The firm’s assessment in (1) must not result in amounts that are lower than:

- (a)

in the case of own funds, the firm’s fixed overheads requirement; and

- (b)

in the case of liquid assets, the firm’s basic liquid assets requirement.

- (a)

01/12/2021G

- (1)

The overall financial adequacy rule requires a MIFIDPRU investment firm to hold sufficient own funds and liquid assets to ensure that it can wind-down its business in an orderly manner (as well as operate its business on an ongoing basis). MIFIDPRU 7.5.9R requires a firm to use its wind-down analysis to assess the appropriate level of own funds and liquid assets for these purposes.

- (2)

A firm’s assessment of the amounts that it needs to hold under the overall financial adequacy rule to ensure that it can be wound down in an orderly manner must never be lower than its wind-down triggers. The firm may conclude that it requires amounts that are higher than these minimum amounts to ensure an orderly wind-down.

- (3)

In appropriate cases, the FCA may consider that either or both of a firm’s wind-down triggers should be set at a higher level. In this case, the FCA may invite a firm to apply for a requirement under section 55L(5) of the Act, or may impose a requirement on the FCA’s own initiative under section 55L(3) of the Act, for the firm to use an alternative wind-down trigger.

- (4)

If the firm’s own funds fall below the own funds wind-down trigger or if the firm’s liquid assets fall below the liquid assets wind-down trigger, the FCA would normally expect that the firm would commence winding down, unless the firm’s governing body has determined that there is an imminent and credible likelihood of recovery. The supervisory actions that the FCA may take in these circumstances are explained in further detail in MIFIDPRU 7.6 in relation to the own funds wind-down trigger and MIFIDPRU 7.7 in relation to the liquid assets wind-down trigger.

- (5)

Where a firm’s own funds or liquid assets fall below the level that is required to ensure an orderly wind-down of the firm, the firm will breach the overall financial adequacy rule. However, as explained further in MIFIDPRU 7.6 in relation to own funds and MIFIDPRU 7.7 in relation to liquid assets, this does not mean that a firm must commence winding down immediately. It is only when the firm breaches one or both of the wind-down triggers that there is a general presumption that the firm should wind-down. Where the firm has breached the overall financial adequacy rule but continues to hold own funds and liquid assets that exceed the wind-down triggers, the FCA would typically take the intervention measures set out in MIFIDPRU 7.6.15G and MIFIDPRU 7.7.17G. However, there may be cases where the firm’s financial position and the projections of its likely future financial resources mean that commencing a wind-down is appropriate, even though the firm has not yet breached the wind-down triggers. The FCA will consider the appropriate supervisory actions according to the facts in each case.

MIFIDPRU 7.6 ICARA process: assessing and monitoring the adequacy of own funds

01/12/2021R

This section applies to a MIFIDPRU investment firm.

01/12/2021R

As part of its ICARA process, a firm must produce a reasonable estimate of the own funds it needs to hold to address:

- (1)

any potential material harms that the firm has identified under MIFIDPRU 7.4.13R and in relation to which it has not taken any measures to reduce the impact of the harms under MIFIDPRU 7.4.9R; and

- (2)

any residual potential material harms that remain after the firm has taken measures to reduce the impact of the harms under MIFIDPRU 7.4.9R.

01/12/2021R

- (1)

A firm must assess on the basis of its analysis under MIFIDPRU 7.6.2R whether it should hold additional own funds in excess of its own funds requirement to comply with the overall financial adequacy rule.

- (2)

When carrying out the assessment in (1), a firm must not:

- (a)

determine that it needs a lower level of own funds for an activity or harm than is required by a rule in MIFIDPRU 4 (Own funds requirements) or MIFIDPRU 5 (Concentration risk); or

- (b)

use components of the own funds requirement to cover potential material harms that cannot reasonably be attributed to that component.

- (a)

31/03/2023G

- (1)

The overall financial adequacy rule requires a firm to hold adequate own funds to ensure that:

- (2)

To comply with the overall financial adequacy rule, a firm must therefore hold the higher of:

- (a)

the amount of own funds that the firm requires at any given point in time to fund its ongoing business operations, taking into account potential periods of financial stress during the economic cycle; and

- (b)

the amount of own funds that a firm would need to hold to ensure that the firm can be wound down in an orderly manner.

- (a)

- (3)

The own funds threshold requirement is the amount of own funds that a firm needs to hold at any given time to comply with the overall financial adequacy rule.

- (4)

The firm’s analysis of potential material harms under MIFIDPRU 7.6.2R is particularly relevant when it is considering the level of own funds that are necessary for the ongoing operation of its business. It is also be relevant when considering how the firm should address potential material harms as part of an orderly wind-down.

- (5)

The following diagram summarises the process that a firm should undertake to determine its own funds threshold requirement:

- (6)

MIFIDPRU TP 2.25AR and MIFIDPRU TP 2.25BG contain rules and guidance on the interaction between a firm’s own funds threshold requirement and the alternative requirement for its fixed overheads requirement, K-factor requirement or permanent minimum capital requirement.

* The own funds threshold requirement cannot be lower than the K-factor requirement or the fixed overheads requirement.

** The K-factor requirement does not apply to SNI MIFIDPRU investment firms and the permanent minimum capital requirement (PMR) is not linked to harm.

*** Unless otherwise specified by the FCA.

01/12/2021R

- (1)

Unless (2) applies, a firm must meet its own funds threshold requirement with own funds that satisfy the following conditions:

- (a)

subject to (b), at least 75% of the own funds threshold requirement must be met with any combination of common equity tier 1 capital and additional tier 1 capital; and

- (b)

at least 56% of the own funds threshold requirement must be met with common equity tier 1 capital.

- (a)

- (2)

The FCA may specify an alternative combination of own funds for the purpose of (1) in a requirement applied to a firm.

01/12/2021G

- (1)

MIFIDPRU 7.6.7G and 7.6.8G explain the approach a non-SNI MIFIDPRU investment firm should apply to carry out the assessment in MIFIDPRU 7.6.3R.

- (2)

MIFIDPRU 7.6.9G explains the approach that an SNI MIFIDPRU investment firm should apply to carry out the assessment in MIFIDPRU 7.6.3R.

- (3)

MIFIDPRU G explains the approach that all MIFIDPRU investment firms should apply when assessing their own funds threshold requirement.

01/12/2021G

- (1)

MIFIDPRU 4 and 5 explain how a firm must determine its own funds requirement. Where, as part of its ICARA process, a firm has identified potential material harms that cannot be fully mitigated, the firm should first consider the extent to which the impact of the residual harm on own funds is covered (wholly or partly) by the framework in MIFIDPRU 4 and 5.

- (2)

Example 1: If the potential material harm arises from the ordinary course of the firm’s portfolio management business, a non-SNI MIFIDPRU investment firm should consider the potential impact of the harm by comparison with the firm’s K-AUM requirement. If the harm is a harm that might typically arise from portfolio management, the firm may treat the harm as covered by the K-AUM requirement. However, if the harm is unusual in nature or might be particularly severe (for example, fraud or other irregularities), it would be unreasonable for the firm to treat the harm as fully covered by the K-AUM requirement. This is because the K-AUM requirement is designed to address typical harms from ordinary portfolio management, and not every conceivable material harm that might result from this activity.

- (3)

Example 2: If the potential material harm arises from the ordinary course of the firm investing its own proprietary capital in positions allocated to the trading book, a non-SNI MIFIDPRU firm should consider the nature of that harm. For example, if the harm relates to the ordinary operational aspects of dealing on own account, the firm may treat the harm as covered by the K-DTF requirement, unless the harm is unusual or particularly severe. If the harm arises from adverse market movements in relation to the firm’s trading book positions, the firm may treat the harm as covered by the K-NPR requirement (or K-CMG requirement if the position arises in a portfolio for which the firm has received a K-CMG permission), unless the relevant positions have particular features that mean the harm may be unusual or particularly severe.

- (4)

Example 3: Some components of the K-factor requirement, such as the K-CON requirement, reflect specific types of harm. In this case, the firm should consider the purpose of the relevant requirement. As the K-CON requirement is designed to address the potential harm arising from a firm having concentrated exposures to a counterparty or group of connected counterparties, a non-SNI MIFIDPRU investment firm should only compare a harm to the K-CON requirement where that harm arises from, or is connected to, these concentrated exposures.

- (5)

Example 4: When assessing harms that may occur during a wind-down of the firm’s business, a non-SNI MIFIDPRU investment firm should consider the potential impact of the harm by comparison with its fixed overheads requirement. In this case, the firm should identify the likely costs of winding down the firm and the potential financial impact of any material harms that might occur while doing so and compare the aggregate amount with the fixed overheads requirement. This will allow a firm to determine whether they are holding sufficient own funds to ensure an orderly wind-down, as required by the overall financial adequacy rule.

01/01/2022G

- (1)

Some harms may not fit within the own funds requirement framework in MIFIDPRU 4 or 5 because they cannot reasonably be attributed to the activities or risks that the rules in those chapters are designed to address. Where the harms are potentially material in nature, a non-SNI MIFIDPRU investment firm will need to assess their potential financial impact separately and cannot treat those harms as covered (either wholly or partly) by a requirement under MIFIDPRU 4 or 5. This includes potential material harms resulting from any regulated activities that are not MiFID business and from any unregulated activities.

- (2)

Example 1: A non-SNI MIFIDPRU investment firm undertakes significant amounts of corporate finance business. The K-factor requirement does not include any components which are designed to address the potential harms arising from this type of business, as none of the K-factor metrics relate to corporate finance business. If the firm identifies potential material harms that may arise from its corporate finance activities, it cannot therefore compare that harm to any part of the K-factor requirement. In this case, the firm will need to assess the potential financial impact of that harm and will need to hold additional own funds to cover that impact.

- (3)

Example 2: A non-SNI MIFIDPRU investment firm holds client money in connection with designated investment business that is not MiFID business. The K-CMH requirement applies only to MiFID client money. If the firm identifies potential material harms that result from holding client money for non-MiFID business, it will therefore need to assess the potential financial impact of that harm and hold additional own funds to cover that impact. Similarly, if there are material issues arising from currency mismatches in relation to MiFID client money, this may be a risk that is not adequately covered by the K-CMH requirement.

- (4)

A firm is not required to map the financial impact of every potential material harm to components of its K-factor requirement. In some circumstances, it may be impractical or disproportionate to allocate the potential financial impact of harms in this way. Alternatively, it may not be clear that a harm can be allocated to one or more components of the K-factor requirement. A firm may therefore hold an amount that is additional to its K-factor requirement to address a particular harm without determining whether that harm might already be partly covered by the K-factor requirement.

- (5)

Example 3: A non-SNI MIFIDPRU investment firm determines that there is a risk of material harm from a cyber incident affecting its IT systems. The firm’s IT systems are used across all its business lines and the firm considers that it is impractical to allocate the financial impact of the cyber incident between particular components of the K-factor requirement. In this situation, the firm may hold an additional amount of own funds (i.e. over and above its K-factor requirement) to cover the potential financial impact of the cyber incident without mapping the impact of the harm to specific components of the K-factor requirement. However, the firm should clearly record the basis on which it has determined the amount of additional own funds that are required.

- (6)

Example 4: A non-SNI MIFIDPRU investment firm is appointed as a depositary. The K-CMH requirement and the K-ASA requirement apply only in relation to MiFID business, and therefore do not apply to its activities as a depositary. If the firm identifies a potential material harm that results from its activities as a depositary, it will need to assess the potential financial impact of that harm and hold additional own funds to cover that impact. A firm may have regard to the general methodology for calculating the K-CMH requirement and the K-ASA requirement when carrying out the assessment in MIFIDPRU 7.6.3R for its activities as a depositary.

01/12/2021G

- (1)

An SNI MIFIDPRU investment firm is not subject to the K-factor requirement. In practice, this means that its own funds requirement is typically determined by the fixed overheads requirement, although for smaller firms, the permanent minimum capital requirement may be determinative.

- (2)

An SNI MIFIDPRU investment firm should therefore identify all relevant potential material harms from its ongoing business operations that cannot be mitigated by other means and estimate their impact on the firm’s own funds. It should then compare the aggregate financial impact on own funds with the firm’s fixed overheads requirement (or, if higher, the permanent minimum capital requirement).

- (3)

Separately, an SNI MIFIDPRU investment firm should also identify the likely costs of winding down the firm and the potential financial impact of any material harms that might occur while doing so and should compare the aggregate amount with the fixed overheads requirement. This will allow the firm to determine if it is holding sufficient own funds to ensure an orderly wind-down, as required by the overall financial adequacy rule.

- (4)

Where an SNI MIFIDPRU investment firm is close to exceeding one or more of the thresholds in MIFIDPRU 1.2.1R that would result in the firm being reclassified as a non-SNI MIFIDPRU investment firm, the firm should begin to compare its assessment of the own funds that it needs to comply with the overall financial adequacy rule with the K-factor requirement that would apply to the firm if it were a non-SNI MIFIDPRU investment firm. The guidance in MIFIDPRU 7.6.7G and 7.6.8G is relevant in these circumstances. Comparison with the future K-factor requirement will ensure that the firm is better prepared to comply with the additional obligations in MIFIDPRU 4 and 5, and that its ICARA process is calibrated appropriately, at the point at which the firm becomes a non-SNI MIFIDPRU investment firm.

01/12/2021G

- (1)

MIFIDPRU 7.6.7G to MIFIDPRU 7.6.9G explain the approach that a firm should take to determine if a potential harm is covered by the firm’s own funds requirement. Where a firm has identified potential harms that are not covered by its own funds requirement, or are covered only partly by its own funds requirement, the firm should aggregate the estimated financial impact of those harms to determine the overall additional amount of own funds (i.e. above its own funds requirement) that the firm needs to comply with the overall financial adequacy rule.

- (2)

Where the FCA disagrees with a firm’s assessment of the amount of own funds that is required by the overall financial adequacy rule, the FCA may provide individual guidance to that firm about the amount of own funds that the FCA considers is necessary to comply with that rule. Alternatively, the FCA may apply a requirement to the firm that specifies an amount of own funds that the firm must hold for that purpose.

- (3)

The effect of MIFIDPRU 7.6.3R(2) is that a firm must not:

- (a)

determine that it needs a lower level of own funds for an activity or harm than is required by a component of the own funds requirement that addresses that risk or harm; or

- (b)

use components of the own funds requirement to cover harms that cannot be attributed to that component.

This is illustrated by the example in (4).

- (a)

- (4)

Example: A non-SNI MIFIDPRU investment firm carries on portfolio management and determines that its K-AUM requirement is £50,000. However, the firm estimates that the actual financial impact of potential harm that may result from its portfolio management activities is only £30,000. The firm also carries on corporate finance advisory business (which does not give rise to a K-factor requirement) and estimates that the financial impact of the potential harm arising from this business is £40,000. The firm should not conclude that its own funds threshold requirement is £70,000. This is because the firm is not permitted to:

- (a)

conclude that the amount of own funds that it holds in relation to its portfolio management activities is less than the K-AUM requirement. This means that the firm is not permitted to substitute its own estimate of £30,000 for the minimum K-AUM requirement of £50,000; or

- (b)

use part of the K-AUM requirement to cover potential material harms that do not arise in connection with portfolio management. This means that the firm cannot reallocate part of the own funds that should be held to cover the K-AUM requirement to cover risks arising from its corporate finance business.

- (a)

- (5)

Instead, assuming that there are no other relevant potential materials harms to be taken into account, the firm should conclude that its own funds threshold requirement is £90,000, which is the sum of the K-AUM requirement and the firm’s estimate of the potential financial impact of harms arising from its corporate finance business.

29/09/2023G

- (1)

Where a MIFIDPRU investment firm is also subject to another prudential regime for its non-MiFID business, its own funds threshold requirement can be no lower than the total financial resources requirement under that prudential regime. This is illustrated by the examples in (2) and (3).

- (2)

Firm A is a collective portfolio management investment firm that is required under IPRU-INV 11.6 to comply with the applicable requirements of MIFIDPRU in parallel with its requirements under IPRU-INV 11. Firm A has an own funds requirement of £2,000,000 under MIFIDPRU 4 and, through its ICARA process, assesses that it needs £500,000 of additional own funds to cover potential material harms. However, Firm A also has a total requirement for own funds of £3,000,000 under IPRU-INV 11.2. In this case, Firm A’s own funds threshold requirement would be £3,000,000, because its own funds threshold requirement can be no lower than the total resources requirement under any other prudential regime that applies to it (IPRU-INV 11).

- (3)

Firm B is a collective portfolio management investment firm that is required under IPRU-INV 11.6 to comply with the applicable requirements of MIFIDPRU in parallel with its requirements under IPRU-INV 11. Firm B has an own funds requirement of £2,000,000 under MIFIDPRU 4 and, through its ICARA process, assesses that it needs £1,500,000 of additional own funds to cover potential material harms. Firm B also has a total requirement for own funds of £3,000,000 under IPRU-INV 11.2. In this case, Firm B’s own funds threshold requirement would be £3,500,000. This is because Firm B’s assessment of its own funds threshold requirement is higher than the total resources requirement under the other prudential regime that applies to it (IPRU-INV 11).

Requirement to notify the FCA of certain levels of own funds

01/12/2021R

- (1)

A firm must notify the FCA immediately in each case where its own funds fall below the level of the firm’s:

- (a)

- (b)

- (c)

own funds wind-down trigger, or the firm considers that there is a reasonable likelihood that its own funds will fall below that level in the foreseeable future.

- (2)

A notification under (1) must include the following information:

- (a)

a clear statement of the current level of the firm’s own funds in comparison to:

- (i)

its own funds threshold requirement; and

- (ii)

in the case of a notification under (1)(c), the firm’s own funds wind-down trigger;

- (i)

- (b)

an explanation of why the firm’s own funds have reached the current level;

- (c)

in the case of a notification made under (1)(a), where the firm has identified that its own funds may fall below a level specified by the firm for the purposes of MIFIDPRU 7.5.5R(1), the recovery actions that the firm intends to take, as identified under MIFIDPRU 7.5.5R(2)(a) and 7.5.6G;

- (d)

in the case of a notification made under (1)(a), confirmation of whether the firm expects that its own funds could fall below its own funds threshold requirement in the foreseeable future and an explanation of why the firm expects this to happen;

- (e)

in the case of a notification made under (1)(b), the recovery actions specified for the purposes of MIFIDPRU 7.5.5R(2)(b) and 7.5.6G that the firm has already taken or will take to restore compliance with its own funds threshold requirement; and

- (f)

in the case of a notification made under (1)(c), the firm’s intentions in relation to activating its wind-down plan.

- (a)

- (3)

A firm must submit the notification in (1) through the online notification and application system using the form in MIFIDPRU 7 Annex 4R.

01/12/2021G

In appropriate cases, the FCA may consider that the early warning indicator should be set at a different level from 110% of a firm’s own funds threshold requirement. In this case, the FCA may invite a firm to apply for a requirement in accordance with section 55L(5) of the Act, or may impose a requirement on the FCA’s own initiative in accordance with section 55L(3) of the Act, to provide for notification to the FCA if the firm’s own funds reach the alternative level.

01/12/2021G

- (1)

The notification requirement in MIFIDPRU 7.6.11R does not replace a firm’s obligations under:

- (2)

Where a firm has submitted a notification under MIFIDPRU 7.6.11R, the notification will generally discharge a firm’s obligations under Principle 11 and the general notification requirements in SUP 15.3 in relation to the matters contained in the notification. However, a firm must still consider whether the FCA should be notified of developments before any of the notification indicators in MIFIDPRU 7.6.11R occur. In addition, Principle 11 and SUP 15.3 may require a firm to notify the FCA of additional material information that is not specifically referenced in MIFIDPRU 7.6.11R.

- (3)

A MIFIDPRU investment firm should notify the FCA at an early stage of any significant event which creates a material risk of a firm ceasing to hold adequate financial resources, even if the impact of that event has not yet fully materialised.

FCA approach to intervention in relation to own funds

01/12/2021G

- (1)

The table in MIFIDPRU 7.6.15G explains the interventions that the FCA would generally expect to make where there is evidence that a MIFIDPRU investment firm may be at risk of breaching the requirements that apply to its own funds. The table sets out the points at which the FCA would normally intervene and what actions it would normally take.

- (2)

The FCA would generally expect that the interventions in the table would be cumulative – i.e. in a declining prudential situation, as the firm hits each intervention point in turn, the FCA would take some or all of the actions associated with that particular point. The actions are intended to be proportionate and progressively stronger responses to address the prudential concerns raised by each intervention point.

- (3)

However, if a firm experiences a sudden adverse event which causes the firm to hit multiple intervention points simultaneously, the FCA may immediately take the actions associated with the most severe point.

- (4)

The actions specified in the table do not prevent the FCA from taking alternative or additional actions in appropriate cases. The purpose of the table is to provide greater clarity for firms on the FCA’s general expectations and approach to interventions, to assist firms’ own planning and responses.

01/12/2021G

This table belongs to MIFIDPRU 7.6.14G.

| Intervention point | Purpose | Potential FCA supervisory actions | |

|---|---|---|---|

Early warning indicator: When the early warning indicator is triggered, the firm must notify the FCA under MIFIDPRU 7.6.11R(1)(a) | This is intended as an early warning to the FCA that the firm may be at risk of breaching its own funds threshold requirement. This will allow the firm and the FCA to consider any preventative action that may be appropriate. | Where the notification is not the expected result of planned action by the firm, the FCA would normally expect the following to occur: | |

| (a) | a dialogue between the FCA and the firm based on the information provided in the notification to understand the reason for the decline in the firm’s own funds and the firm’s future plans; and | ||

| (b) | enhanced monitoring and supervision of the firm by the FCA. | ||

| After having considered the information provided by the firm about its proposed actions, if the FCA reasonably considers that the firm may breach its own funds threshold requirement in the foreseeable future, the FCA may consider the following additional actions: | |||

| (c) | requesting that the firm cease making discretionary distributions of capital, loans to affiliated entities, payments of dividends or payments of variable remuneration; | ||

| (d) | requesting that the firm take some or all of the recovery actions identified by the firm under MIFIDPRU 7.5.5R(2) and 7.5.6G; | ||

| (e) | requesting that the firm report additional information to the FCA; | ||

| (f) | requesting that the firm improve its internal risk management and systems and controls; | ||

| (g) | requesting that the firm cease making acquisitions; or | ||

| (h) | where appropriate, inviting the firm to apply for a requirement under section 55L(5) of the Act, or imposing a requirement on the FCA’s own initiative under section 55L(3) of the Act, in relation to (c) – (g) above. | ||

Threshold requirement notification: Firm holding insufficient own funds to meet its own funds threshold requirement | In the FCA’s view, where a firm is failing to hold sufficient own funds to comply with its own funds threshold requirement, the firm will be failing to meet the appropriate resources threshold condition. This trigger is intended to prompt the firm and the FCA to address the breach of threshold conditions in a timely manner. Where appropriate, the focus should be on recovery of the firm (unless the firm chooses to exit the market by voluntarily winding down). However, any proposed actions for recovery must be credible and achievable within a reasonable and realistic timeframe. | The FCA would normally expect that: | |

| (a) | the firm will have taken any relevant recovery actions identified by the firm under MIFIDPRU 7.5.5R(2)(a) and 7.5.6G before breaching its own funds threshold requirement and will be preparing to take, or will have taken, any relevant recovery actions identified under MIFIDPRU 7.5.5R(2)(b); and | ||

| (b) | the firm will cease making discretionary distributions of capital, loans to affiliated entities, payments of dividends or payments of variable remuneration. | ||

| After having considered the information provided by the firm about its proposed actions, if the FCA reasonably considers that the firm may fail to restore its own funds to the level required by the own funds threshold requirement within a reasonable timeframe, the FCA may consider the following additional actions: | |||

| (c) | requesting that the firm cease taking on new business; | ||

| (d) | requesting that the firm report additional information to the FCA; | ||

| (e) | requesting that the firm’s parent undertaking provides additional own funds for the firm; | ||

| (f) | where appropriate, inviting the firm or its parent undertaking to apply for a requirement under section 55L(5) or section 143K(1) of the Act, or imposing a requirement on the FCA’s own initiative under section 55L(3) or section 143K(2) of the Act, in relation to (a) – (e) above; or | ||

| (g) | where appropriate, inviting the firm to apply for variation or cancellation of permission under section 55H of the Act, or varying or cancelling the firm’s permission on the FCA’s own initiative under section 55J of the Act. | ||

| The FCA would also expect the firm to consider whether it is appropriate to trigger the firm’s wind-down plan under MIFIDPRU 7.5.7R to ensure an orderly wind-down of its business. This may be the case where the firm’s identified wind-down actions will require a reasonable length of time to execute, such as where the firm will need to transfer customers or close out its own positions. | |||

Wind-down trigger notification: Firm’s own funds fall below its own funds wind-down trigger | The own funds wind-down trigger is intended to specify a level of own funds that is sufficient to ensure an orderly wind-down of the firm. Where the firm’s own funds requirement is determined by the fixed overheads requirement and the firm has not identified that it needs to hold additional own funds to comply with the overall financial adequacy rule, the own funds wind-down trigger may be equal to the firm’s own funds threshold requirement. In that case, the FCA may proceed directly to applying the interventions in this row, rather than those specified for a breach of the own funds threshold requirement above. In order to maximise the potential for an orderly wind-down, the FCA expects that firms that breach this trigger should normally commence winding down immediately, unless the firm’s governing body and the FCA determine that there is an imminent and credible likelihood of recovery. | The FCA would normally expect the following to occur: | |

| (a) | the firm’s governing body will make a formal decision to initiate the firm’s wind-down plan, unless the governing body has a reasonable basis for determining that there is an imminent and credible likelihood of the firm’s recovery; and | ||

| (b) | where the firm decides to initiate its wind-down plan, the FCA will invite the firm to apply for a requirement under section 55L(5) of the Act, or will impose a requirement on the FCA’s own initiative under section 55L(3) of the Act, that prevents the firm from taking on any new business. | ||

| The FCA may consider the following additional actions if it has concerns that without such actions, the potential risk of harm to consumers or the markets is likely to increase: | |||

| (c) | taking appropriate action to protect any client money or client assets, including, where appropriate, inviting the firm to apply for a requirement under section 55L(5) of the Act, or imposing a requirement on the FCA’s own initiative under section 55L(3) of the Act, to achieve any necessary protection; and | ||

| (d) | where appropriate, inviting the firm to apply for variation or cancellation of permission under section 55H of the Act, or varying or cancelling the firm’s permission on the FCA’s own initiative under section 55J of the Act. | ||

| If a firm refuses to commence an orderly wind-down despite its governing body or the FCA having concluded that there is no imminent and credible likelihood of recovery, the FCA will consider the full range of its supervisory powers. In particular, the FCA may use a combination of its own initiative powers under section 55L(3) and section 55J of the Act to: | |||

| (e) | prevent the firm from continuing to carry on any regulated activities; and | ||

| (f) | require the firm to take appropriate actions to ensure the fair treatment and appropriate protection of clients and counterparties during any run-off period for its existing regulated business. | ||

MIFIDPRU 7.7 ICARA process: assessing and monitoring the adequacy of liquid assets

01/12/2021R

This section applies to a MIFIDPRU investment firm.

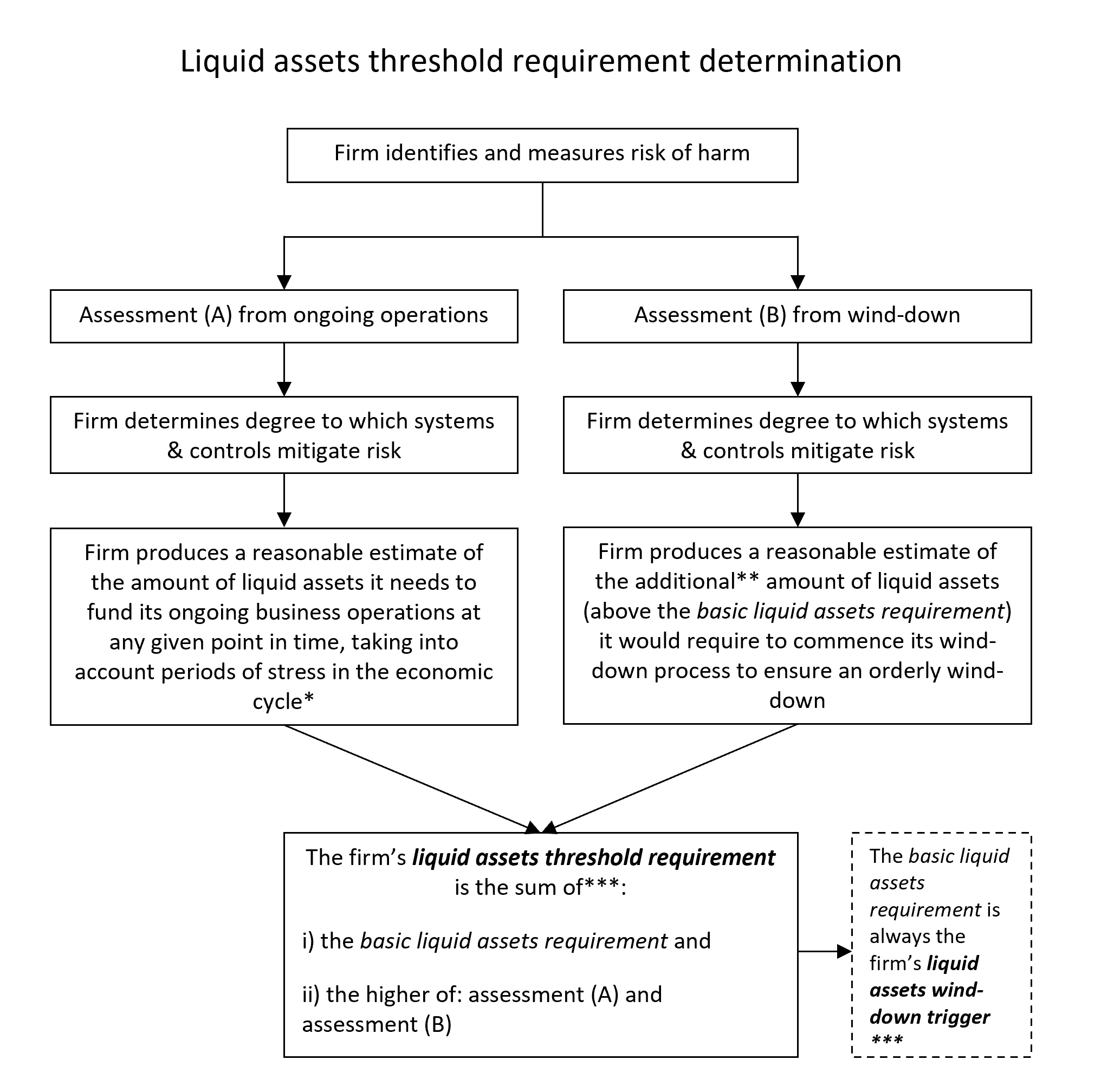

01/12/2021R

- (1)

As part of its ICARA process, a firm must produce a reasonable estimate of the maximum amount of liquid assets that the firm would require to:

- (2)

The assessment in (1) must take into account any potential material harms that the firm has identified under MIFIDPRU 7.4.9R and been unable to reduce appropriately through its systems and controls.

- (3)

Without prejudice to the ongoing nature of the ICARA process, the firm must update the analysis in (1) immediately following any material change in the firm’s business model or operating model.

- (4)

To produce the estimate in (1), the firm must ensure that it has in place reliable management information systems to provide timely and forward-looking information on its liquidity position.

01/12/2021G

- (1)