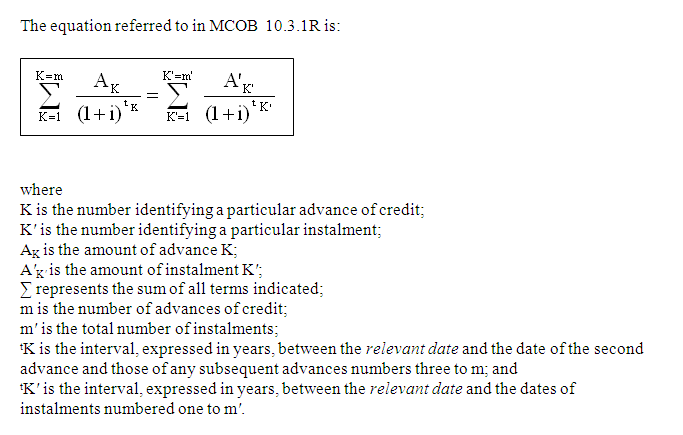

The APR must be calculated so that, subject to MCOB 10.3.1B R (2), the annual percentage rate of charge is the rate for i which satisfies the equation set out in MCOB 10.3.1A R, expressed as a percentage.

MCOB 10.3 Formula and assumptions for calculating the APR

You are viewing MCOB 10.3 Formula and assumptions for calculating the APR as of . MCOB 10.3 Formula and assumptions for calculating the APR was last updated on 23/03/2018.

MCOB 10.3 Formula and assumptions for calculating the APR

Formula for calculating the APR

01/10/2013R

31/10/2004R

Formula for calculating the APR

31/10/2004R

- (1)

In MCOB 10.3.1A R, references to instalments are references to any payment made by or on behalf of the customer which comprise:

- (a)

a repayment of all or part of the credit under the contract; or

- (b)

a payment of all or part of the total charge for credit; or

- (c)

both a repayment of all or part of the credit and a payment of all or part of the total charge for credit.

- (a)

- (2)

Where more than one rate is given under MCOB 10.3.1 R, the APR is the positive rate nearest to zero or, if no positive rate is given, the negative rate nearest to zero.

01/04/2014G

This calculation method is the same (with the exception of MCOB 10.3.8 R(1) and (2)) as that described in CONC App 1.1. Some of the terminology is different from that used elsewhere in MCOB, e.g. the references to 'transactions' should be read as relating to secured lending.

APR calculation: assumptions as to the credit provided

31/10/2004R

- (1)

The APR must be calculated on the basis of the following assumptions:

- (a)

the assumption that the customer will not be entitled to any income tax relief relating to the transaction other than relief under sections 266-7 of the Income and Corporation Taxes Act 1988 and Schedule 14-15 to the same Act without any deduction under section 274 of the Income and Corporation Taxes Act 1988;

- (b)

the assumption that no assistance is given under the Home Purchase Assistance and Housing Corporation Guarantee Act 1978;

- (c)

- (i)

in the case of a transaction which provides for repayment of the credit or of the total charge for credit at or not later than a specified time or times, the assumption that the mortgage lender or mortgage administrator will not exercise any right under the transaction to require repayment at any other time or times; and

- (ii)

in any other case, the assumption that the mortgage lender or mortgage administrator will not exercise any right under the transaction to require payment;the customer, in any case, performing all his obligations under the transaction;

- (i)

- (d)

unless (e) applies, in the case of a transaction which provides for variation of the rate or amount of any item included in the total charge for credit in consequence of the occurrence after the relevant date of any event, the assumption that the event will not occur; and, in this sub-paragraph, 'event' means an act or omission of the customer or of the mortgage lender or mortgage administrator or any other event (including, where the transaction makes provision for variation upon the continuation of any circumstance, the continuation of that circumstance) but does not include an event which is certain to occur and of which the date of occurrence, or the earliest date of occurrence, can be ascertained at the date of the making of the agreement; and

- (e)

in the case of a secured lending contract which provides for the possibility of any variation of the rate of interest in consequence of the occurrence after the relevant date of any event (being an event which is certain to occur and of which the date of occurrence, or the earliest date of occurrence, can be ascertained at the date of the making of the agreement), the assumption that such a variation will, when the event occurs, take place.

- (a)

- (2)

For the purposes of this chapter:

- (a)

an item included in the total charge for credit must not be treated as credit, even if time is allowed for its payment;

- (b)

subject to (c) and to MCOB 10.3.13 R, in the case of any agreement, each provision of credit and each repayment of the credit and of the total charge for credit must be taken to be made:

- (i)

at the earliest time provided under the transaction; and

- (ii)

in a case where any such provision or repayment is to be made at or not later than a specified time, at that time;

and, where any such repayment is to be made before the relevant date, it must be taken to be made on the relevant date;

- (i)

- (c)

where, under an agreement for running-account credit or an agreement for fixed-sum credit where the credit is not repayable at specified intervals or in specified amounts, a constant period rate of charge in respect of periods of equal or of nearly equal length is charged, it must be assumed, despite MCOB 10.3.12 R, that:

- (i)

the amount of credit outstanding at the beginning of a period is to remain outstanding throughout the period;

- (ii)

the amount of any credit provided during a period is provided immediately after the end of the period; and

- (iii)

any repayment of credit or of the total charge for credit made during a period is made immediately after the end of the period; and

- (i)

- (d)

it must be assumed that the amount of any repayment of credit or of the total charge for credit will, at the time when the repayment is made, be the smallest for which the agreement provides.

- (a)

APR calculation: rounding

31/10/2004R

Where the APR, as calculated in accordance with MCOB 10.3.1 R, has more than one decimal place it must be rounded to one decimal place as follows:

- (1)

where the figure at the second decimal place is greater than or equal to five, the figure at the first decimal place must be increased by one and the decimal place (or places) following the first decimal place must be disregarded; and

- (2)

where the figure at the second decimal place is less than five, that decimal place and any decimal places following it must be disregarded.

APR calculation: the calculation of any period

31/10/2004R

For the purposes of calculations under this chapter, the length of any period must be calculated as follows:

- (1)

a period which is not a whole number of calendar months or a whole number of weeks must be counted in years and days;

- (2)

subject to (3), a period which is a whole number of calendar months or a whole number of weeks must be counted in calendar months or in weeks, as the case may be;

- (3)

where a period is both a whole number of calendar months and a whole number of weeks and:

- (4)

a period which is to be counted:

- (5)

a day may be taken to be either:

- (6)

Every day must be taken to be a business day

APR calculation: necessary assumptions

31/10/2004R

- (1)

MCOB 10.3.7 R to MCOB 10.3.13 R apply for the purpose of the calculation of the total charge for credit and of the rate of that charge in respect of matters necessary for the calculation which cannot be ascertained by the mortgage lender or mortgage administrator at the date of the making of the agreement.

- (2)

In a case where MCOB 10.3.7 R and one or more of MCOB 10.3.8 R to MCOB 10.3.13 R are applicable, MCOB 10.3.7 R must be applied first.

APR calculation: assumptions as to the amount of credit

31/10/2004R

- (1)

Where the amount of the credit to be provided under the agreement cannot be ascertained at the date of the making of the agreement:

- (a)

in the case of an agreement for running-account credit under which there is a credit limit, that amount must be taken to be that credit limit; and

- (b)

in any other case, that amount shall be taken to be £100.

- (a)

- (2)

Where a mortgage lender makes a further advance to the customer in addition to the amount originally borrowed under the regulated mortgage contract, the APR for the further advance must be calculated in respect of the further advance alone (and any related charges), and not in respect of the total amount borrowed.

APR calculation: assumptions as to the period for which credit is provided

23/03/2018R

- (1)

In relation to a lifetime mortgage, where the APR is calculated for the purpose of a financial promotion it must be assumed that the credit is being provided for a period of 15 years beginning with the relevant date.

- (2)

In relation to a lifetime mortgage, where the APR is calculated for the purpose of an illustration, the period for which the credit is to be provided must be calculated in accordance with MCOB 9.4.10 R or MCOB 9.4.12 R.

- (2A)

In relation to a retirement interest-only mortgage, where the APR is calculated for the purposes of an illustration the period for which the credit is to be provided must be determined in accordance with MCOB 5.6.6R(4).

- (3)

Where, in any other case, the period for which credit is to be provided is not ascertainable at the date of the making of the agreement, it must be assumed that credit is provided for one year beginning with the relevant date.

APR calculation: assumption where rate or amount is referenced to another factor

31/10/2004R

Subject to MCOB 10.3.10 R, where the rate or amount of any item included in the total charge for credit, or the amount of any repayment of credit under a transaction, is to be ascertained by reference to the level of any index or other factor in accordance with a specified formula, the rate or amount must be taken to be the rate or amount so ascertained. The formula must be applied as if the level of the index or other factor subsisting at the date of the making of the agreement were that subsisting at the date by reference to which the formula is to be applied.

APR calculation: assumptions where secured lending contracts provide for the variation in the rate of interest

31/10/2004R

- (1)

The assumptions in MCOB 10.3.10 R(3) and (4) apply to any secured lending contracts which provide for the possibility of any variation of the rate of interest if it is to be assumed, under MCOB 10.3.3 R(1)(e), that the variation will take place but the amount of the variation cannot be ascertained at the date of the making of the agreement.

- (2)

In this paragraph:

- (a)

'initial standard variable rate' means:

- (i)

the standard variable rate of interest which would be applied by the mortgage lender or mortgage administrator to the agreement on the date of the making of the agreement if the agreement provided for interest to be paid at the mortgage lender or mortgage administrator's standard variable rate with effect from that date; or

- (ii)

if there is no such rate, the standard variable rate of interest applied by the mortgage lender or mortgage administrator on the day of the making of the agreement in question to other secured lending contracts or, where there is more than one such rate, the highest such rate;

taking no account of any discount or other reduction to which the customer would or might be entitled; and

- (i)

- (b)

'varied rate' means any rate of interest charged when a variation of the rate of interest under MCOB 10.3.3 R(1)(e) is to be assumed.

- (a)

- (3)

Where a secured lending contract provides a formula for calculating a varied rate by reference to a standard variable rate of interest applied by the firm, or any other fluctuating rate of interest, but does not enable the varied rate to be ascertained at the date of the making of the agreement because it is not known on that date what the standard variable rate will be or (as the case may be) at what level the fluctuating rate will be fixed when the varied rate falls to be calculated, it must be assumed that that rate or level will be the same as the initial standard variable rate.

- (4)

Where a secured lending contract provides for the possibility of any variation in the rate of interest (other than a variation referred to in MCOB 10.3.10 R(3)) which it is to be assumed, under MCOB 10.3.3 R(1)(e), will take place, but does not enable the amount of that variation to be ascertained at the date of the making of the agreement, it must be assumed that the varied rate will be the same as the initial standard variable rate.

APR calculation: further assumptions

31/10/2004R

Where:

- (1)

the period for which the credit, or any of it, is to be or may be provided cannot be ascertained at the date of the making of the agreement; and

- (2)

the rate or amount of any item included in the total charge for credit will change at a time provided in the transaction within one year beginning with the relevant date;

the rate or amount must be taken to be the highest rate or amount under the transaction at any time in that year.

31/10/2004R

Where the earliest date on which credit is to be provided cannot be ascertained at the date of making of the agreement, it must be assumed that credit is provided on that date.

31/10/2004R

In the case of any transaction, it must be assumed:

- (1)

that a charge payable at a time which cannot be ascertained at the date of the making of the agreement is to be payable on the relevant date or, where it may reasonably be expected that a customer will not make payment on that date, on the earliest date at which it may reasonably be expected that he will make payment; or

- (2)

where more than one payment of a charge of the same description is to be made at times which cannot be ascertained at the date of the making of the agreement, that the first such payment will be payable on the relevant date (or, where it may reasonably be expected that a customer will not make payment on that date, at the earliest date on which it may reasonably be expected that he will make payment), that the last such payment will be payable at the end of the period for which credit is provided and that all other such payments (if any) will be payable at equal intervals between those times.