This chapter applies to:

- (1)

an authorised fund manager of an AUT, ACS or an ICVC;

- (2)

- (3)

a depositary of an AUT, ACS or an ICVC; and

- (4)

an ICVC,

where such AUT, ACS or ICVC is a UCITS scheme or a non-UCITS retail scheme.

This chapter applies to:

an authorised fund manager of an AUT, ACS or an ICVC;

a depositary of an AUT, ACS or an ICVC; and

an ICVC,

where such AUT, ACS or ICVC is a UCITS scheme or a non-UCITS retail scheme.

This chapter helps in achieving the statutory objective of protecting consumers by ensuring consumers have access to up-to-date detailed information about an authorised fund particularly before buying units and thereafter an appropriate level of investor involvement exists by providing a framework for them to:

participate in the decisions on key issues concerning the authorised fund; and

be sent regular and relevant information about the authorised fund.

This section applies to an authorised fund manager, an ICVC and any other director of an ICVC

A prospectus must be drawn up in English and published as a document by the authorised fund manager and, for an ICVC, it must be approved by the directors.

The authorised fund manager must ensure that the prospectus:

contains the information required by COLL 4.2.5 R (Table: contents of the prospectus);

for a non-UCITS retail scheme managed by a full-scope UK AIFM, contains the information required by:

FUND 3.2.2R and FUND 3.2.3R (Prior disclosure of information to investors); and

FUND 3.2.5R and FUND 3.2.6R (Periodic disclosure), unless the up-to-date information has been published in the scheme’s most recent annual report or half-yearly report;

does not contain any provision which is unfairly prejudicial to the interests of unitholders generally or to the unitholders of any class of units;

does not contain any provision that conflicts with any applicable rule; and

is kept up-to-date and that revisions are made to it, whenever appropriate.

The authorised fund manager of an AUT, ACS or an ICVC must:

provide a copy of the scheme's most recent prospectus drawn up and published in accordance with COLL 4.2.2 R (Publishing the prospectus) free of charge to any person on request; and

file a copy of the scheme's original prospectus, together with all revisions thereto, with the FCA.

Except where an investor requests a paper copy or the use of electronic communications is not appropriate, the prospectus may be provided in a durable medium or by means of a website that meets the website conditions.

[deleted]

An authorised fund manager must, upon the request of a unitholder in a UCITS scheme that it manages, provide information supplementary to the prospectus of that scheme relating to:

the quantitative limits applying to the risk management of that scheme;

the methods used in relation to (a); and

any recent development of the risk and yields of the main categories of investment.

[Note: articles 74, 75(1) and 75(2) of the UCITS Directive]

The authorised fund manager of a UCITS scheme that is a feeder UCITS must:

where requested by an investor, provide a copy of the prospectus of its master UCITS free of charge; and

file a copy of the prospectus of its master UCITS and any amendments thereto with the FCA.

Except where an investor requests a paper copy or the use of electronic communications is not appropriate, the prospectus of the master UCITS may be provided in a durable medium other than paper or by means of a website that meets the website conditions.

[Note: articles 63(3), 63(5), 75(1) and 75(2) of the UCITS Directive]

The authorised fund manager of a feeder NURS must, where requested by an investor or the FCA, provide such person with a copy of the prospectus of its qualifying master scheme free of charge.

Except where an investor requests a paper copy or the use of electronic communications is not appropriate, the prospectus of the qualifying master scheme may be provided in a durable medium other than paper, or by means of a website that meets the website conditions.

must ensure that the prospectus of the authorised fund does not contain any untrue or misleading statement or omit any matter required by the rules in this sourcebook to be included in it; and

is liable to pay compensation to any person who has acquired any units in the authorised fund and suffered loss in respect of them as a result of such statement or omission; this is in addition to any liability incurred apart from under this rule.

The authorised fund manager is not in breach of (1)(a) and is not liable to pay compensation under (1)(b) if, at the time when the prospectus was made available to the public, it had taken reasonable care to determine that the statement was true and not misleading, or that the omission was appropriate, and that:

it continued to take such reasonable care until the time of the relevant acquisition of units in the scheme; or

the acquisition took place before it was reasonably practicable to bring a correction to the attention of potential purchasers; or

it had already taken all reasonable steps to ensure that a correction was brought to the attention of potential purchasers; or

the person who acquired the units was not materially influenced or affected by that statement or omission in making the decision to invest.

The authorised fund manager is also not in breach of (1)(a) and is not liable to pay compensation under (1)(b) if:

before the acquisition a correction had been published in a manner calculated to bring it to the attention of persons likely to acquire the units in question; or

it took all reasonable steps to secure such publication and had reasonable grounds to conclude that publication had taken place before the units were acquired.

The authorised fund manager is not liable to pay compensation under (1)(b) if the person who acquired the units knew at the time of the acquisition that the statement was untrue or misleading or knew of the omission.

For the purposes of this rule a revised prospectus will be treated as a different prospectus from the original one.

References in this rule to the acquisition of units include references to contracting to acquire them.

This table belongs to COLL 4.2.2 R (Publishing the prospectus).

| Document status | ||||||

| 1 | A statement that the document is the prospectus of the authorised fund valid as at a particular date (which shall be the date of the document). | |||||

| Authorised fund | ||||||

| 2 | A description of the authorised fund including: | |||||

| (a) | its name; | |||||

| (aa) | its FCA product reference number (PRN); | |||||

| (b) | whether it is an ICVC, ACS or an AUT; | |||||

| (ba) | whether it is a UCITS scheme or a non-UCITS retail scheme; | |||||

| (bb) | a statement that unitholders in an AUT, ICVC or co-ownership scheme are not liable for the debts of the authorised fund; | |||||

| (bc) | a statement that the scheme property of a co-ownership scheme is beneficially owned by the participants as tenants in common (or, in Scotland, is the common property of the participants); | |||||

| (bd) | a statement that a unitholder in a limited partnership scheme is not liable for the debts or obligations of the limited partnership scheme beyond the amount of the scheme property which is available to the authorised contractual scheme manager to meet such debts or obligations, provided that the unitholder does not take part in the management of the partnership business; | |||||

| (be) | a statement that the exercise of rights conferred on limited partners by FCA rules does not constitute taking part in the management of the partnership business; | |||||

| (c) | for an ICVC, the address of its head office and the address of the place in the United Kingdom for service on the ICVC of notices or other documents required or authorised to be served on it; | |||||

| (ca) | for an ACS that is a limited partnership scheme, the address of the proposed principal place of business of the limited partnership scheme; | |||||

| (d) | the effective date of the authorisation order made by the FCA and relevant details of termination, if the duration of the authorised fund is limited; | |||||

| (e) | its base currency; | |||||

| (f) | for an ICVC, the maximum and minimum sizes of its capital; | |||||

| (g) | the circumstances in which it may be wound up under the rules and a summary of the procedure for, and the rights of unitholders under, such a winding up; and | |||||

| (h) | if it is not an umbrella, a statement that it is a feeder UCITS, a feeder NURS, a fund of alternative investment funds or a property authorised investment fund, where that is the case. | |||||

| Umbrella ICVCs or co-ownership schemes | ||||||

| 2A | The following statements for an ICVC or a co-ownership scheme which is an umbrella: | |||||

| (a) | for an ICVC, a statement that its sub-funds are segregated portfolios of assets and, accordingly, the assets of a sub-fund belong exclusively to that sub-fund and shall not be used to discharge directly or indirectly the liabilities of, or claims against, any other person or body, including the umbrella, or any other sub-fund, and shall not be available for any such purpose; | |||||

| (aa) | for a co-ownership scheme, a statement that the property subject to a sub-fund is beneficially owned by the participants in that sub-fund as tenants in common (or, in Scotland, is the common property of the participants in that sub-fund) and must not be used to discharge any liabilities of, or meet any claims against, any person other than the participants in that sub-fund; and | |||||

| (b) | for an ICVC or a co-ownership scheme, a statement that while the provisions of the OEIC Regulations, and section 261P (Segregated liability in relation to umbrella co-ownership schemes) of the Act in the case of co-ownership schemes, provide for segregated liability between sub-funds, the concept of segregated liability is relatively new. Accordingly, where claims are brought by local creditors in foreign courts or under foreign law contracts, it is not yet known how those foreign courts will react to regulations 11A and 11B of the OEIC Regulations or, as the case may be, section 261P of the Act. | |||||

| Umbrella Schemes | ||||||

| 2B | For a UCITS scheme or non-UCITS retail scheme which is an umbrella: | |||||

| (a) | a statement detailing whether each specific sub-fund is a feeder UCITS, a feeder NURS, a fund of alternative investment funds or a property authorised investment fund, as appropriate; and | |||||

| (b) | the FCA product reference number (PRN) of each sub-fund. | |||||

| Investment objectives and policy | ||||||

| 3 | The following particulars of the investment objectives and policy of the authorised fund: | |||||

| (a) | the investment objectives, including its financial objectives; | |||||

| (b) | the authorised fund's investment policy for achieving those investment objectives, including the general nature of the portfolio and, if appropriate, any intended specialisation; | |||||

| (c) | an indication of any limitations on that investment policy; | |||||

| (c-b) | where: | |||||

| (i) | a target for a scheme’s performance has been set, or a payment out of scheme property is permitted, by reference to a comparison of one or more aspects of the scheme property or price with fluctuations in the value or price of an index or indices or any other similar factor (a “target benchmark”); or | |||||

| (ii) | without being a target benchmark, arrangements are in place in relation to the scheme according to which the composition of the portfolio of the scheme is, or is implied to be, constrained by reference to the value, the price or the components of an index or indices or any other similar factor (a “constraining benchmark”); or | |||||

| (iii) | without being a target benchmark or a constraining benchmark, the scheme’s performance is compared against the value or price of an index or indices or any other similar factor (a “comparator benchmark”), | |||||

| a statement providing sufficient information for investors to understand the choice and use of any target benchmark, constraining benchmark or comparator benchmark in relation to the scheme; | ||||||

| (c-a) | where no target benchmark, constraining benchmark or comparator benchmark is used, a statement to that effect and an explanation of how investors can assess the performance of the scheme; | |||||

| (ca) | for an authorised fund that has indicated in its name, investment objectives or fund literature (including in any financial promotions for the fund), through use of descriptions such as 'absolute return', 'total return' or similar, an intention to deliver positive returns in all market conditions (and where there is no actual guarantee of such returns), additional statements in the authorised fund's investment objectives specifying: | |||||

| (i) | that capital is in fact at risk; | |||||

| (ii) | the investment period over which the authorised fund aims to achieve a positive return; and | |||||

| (iii) | there is no guarantee that this will be achieved over that specific, or any, time period; | |||||

| (d) | the description of assets which the capital property may consist of; | |||||

| (e) | the proportion of the capital property which may consist of an asset of any description; | |||||

| (f) | the description of transactions which may be effected on behalf of the authorised fund and an indication of any techniques and instruments or borrowing powers which may be used in the management of the authorised fund; | |||||

| (g) | a list of the eligible markets through which the authorised fund may invest or deal in accordance with COLL 5.2.10 R (2)(b) (Eligible markets: requirements); | |||||

| (h) | for an ICVC, a statement as to whether it is intended that the scheme will have an interest in any immovable property or movable property ((in accordance with COLL 5.6.4 R (2) (Investment powers: general) or COLL 5.2.8 R (2) (UCITS schemes: general)) for the direct pursuit of the ICVC's business; | |||||

| (i) | where COLL 5.2.12 R (3) (Spread: government and public securities) applies: | |||||

| (i) | a prominent statement as to the fact that more than 35% in value of the scheme property is or may be invested in transferable securities or approved money-market instruments issued or guaranteed by a single state, local authority or public international body; and | |||||

| (ii) | the names of the individual states, local authorities or public international bodies issuing or guaranteeing the securities in which more than 35% in value of the scheme property may be invested; | |||||

| (k) | for an authorised fund which may invest in other schemes, the extent to which the scheme property may be invested in the units of schemes which are managed by the authorised fund manager or by it s associate; | |||||

| (ka) | where a scheme is a feeder scheme (other than a feeder UCITS or a feeder NURS), which (in respect of investment in units in collective investment schemes) is dedicated to units in a single collective investment scheme, details of the master scheme and the minimum (and, if relevant, maximum) investment that the feeder scheme may make in it; | |||||

| (l) | where a scheme invests principally in scheme units, deposits or derivatives, or replicates an index in accordance with COLL 5.2.31 R or COLL 5.6.23 R (Schemes replicating an index), a prominent statement regarding this investment policy; | |||||

| (m) | where derivatives transactions may be used in a scheme, a prominent statement as to whether these transactions are for the purposes of efficient portfolio management (including hedging) or meeting the investment objectives or both and the possible outcome of the use of derivatives on the risk profile of the scheme; | |||||

| (n) | information concerning the profile of the typical investor for whom the scheme is designed; | |||||

| (o) | information concerning the historical performance of the scheme, comparing in particular its historical performance against each target benchmark and each constraining benchmark used in relation to the scheme, presented in accordance with COBS 4.6.2R (the rules on past performance); | |||||

| (p) | for a non-UCITS retail scheme which invests in immovables, a statement of the countries or territories of situation of land or buildings in which the authorised fund may invest; | |||||

| (pa) | for a fund investing in inherently illiquid assets at least the following (see FUND 3.2.2R(8) (Prior disclosure of information to investors)): | |||||

| (i) | an explanation of the risks associated with the scheme investing in inherently illiquid assets and how those risks might crystallise; | |||||

| (ii) | a description of the tools and arrangements the authorised fund manager would propose using, including those required by FCA rules, to mitigate the risks referred to in (i); and | |||||

| (iii) | an explanation of the circumstances in which those tools and arrangements would typically be deployed and the likely consequences for investors; | |||||

| (q) | for a UCITS scheme which invests a substantial portion of its assets in other schemes, a statement of the maximum level of management fees that may be charged to that UCITS scheme and to the schemes in which it invests; | |||||

| (qa) | where the authorised fund is a qualifying money market fund, a statement identifying it as such a fund and a statement that the authorised fund's investment objectives and policies will meet the conditions specified in the definition of qualifying money market fund; | |||||

| (r) | where the net asset value of a UCITS scheme is likely to have high volatility owing to its portfolio composition or the portfolio management techniques that may be used, a prominent statement to that effect; | |||||

| (s) | for a UCITS scheme, a statement that any unitholder may obtain on request the types of information (which must be listed) referred to in COLL 4.2.3R (3) (Availability of prospectus and long report); and | |||||

| (t) | for a UCITS scheme that is or is intended to be a master UCITS, a statement that it is not a feeder UCITS and will not hold units of a feeder UCITS. | |||||

| Reporting, distributions and accounting dates | ||||||

| 4 | Relevant details of the reporting, accounting and distribution information which includes: | |||||

| (a) | the accounting and distribution dates; | |||||

| (b) | procedures for: | |||||

| (i) | determining and applying income (including how any distributable income is paid); | |||||

| (ii) | unclaimed or unwanted distributions, including any arrangements for the transfer of: | |||||

| (A) | an unclaimed eligible distribution of income that is a dormant asset (see COLL 6.8.4R (Unclaimed, de minimis and joint unitholder distributions)); or | |||||

| (B) | unwanted asset money (see COLL 6.8.4AR (Unwanted asset money)); and | |||||

| (iii) | if relevant, calculating, paying and accounting for income equalisation; and | |||||

| (c) | the accounting reference date and when the long report will be published in accordance with COLL 4.5.14 R (Publication and availability of annual and half-yearly long report). | |||||

| (d) | [deleted] | |||||

| Characteristics of the units | ||||||

| 5 | Information as to: | |||||

| (a) | where there is more than one class of unit in issue or available for issue, the name of each such class and the rights attached to each class in so far as they vary from the rights attached to other classes; | |||||

| (b) | [deleted] | |||||

| (c) | how unitholders may exercise their voting rights and what these amount to; | |||||

| (d) | where a mandatory redemption, cancellation or conversion of units from one class to another may be required, in what circumstances it may be required; and | |||||

| (e) | for an AUT, the fact that the nature of the right represented by units is that of a beneficial interest under a trust. | |||||

| 5A | ACSs: UCITS and NURS eligible investors | |||||

| (a) | A statement that units may not be issued to a person other than a: | |||||

| (i) | professional ACS investor; or | |||||

| (ii) | large ACS investor; or | |||||

| (iii) | person who already holds units in the scheme. | |||||

| (b) | A statement that the authorised contractual scheme manager must redeem, or in respect of a direct dealing scheme effect the cancellation of, units as soon as practicable after becoming aware that those units are vested in anyone (whether as a result of subscription or transfer of units) other than a person meeting the criteria in paragraph 5A(a). | |||||

| 5B | ACSs: UCITS and NURS transfer of units | |||||

| (a) | A statement whether the transfer of units in the ACS scheme is either: | |||||

| (i) | prohibited; or | |||||

| (ii) | allowed; | |||||

| by the instrument constituting the fund and prospectus. | ||||||

| (b) | Where transfer of units is allowed by the instrument constituting the fund and prospectus in accordance with (a)(ii), a statement that units may only be transferred in accordance with the conditions specified by FCA rules, including that units may not be transferred to a person other than a: | |||||

| (i) | professional ACS investor; or | |||||

| (ii) | large ACS investor; or | |||||

| (iii) | person who already holds units in the scheme. | |||||

| (c) | For a co-ownership scheme which is an umbrella, a statement in accordance with (5B)(a)(i) or (ii) and, where appropriate, a statement in accordance with (5B)(b), must also be made for the sub-funds. Where individual sub-funds have differing policies in relation to transfer of units, separate statements are required. | |||||

| Authorised fund manager | ||||||

| 6 | The following particulars of the authorised fund manager: | |||||

| (a) | its name; | |||||

| (b) | the nature of its corporate form; | |||||

| (c) | the date of its incorporation; | |||||

| (d) | the address of its registered office; | |||||

| (e) | the address of its head office, if that is different from the address of its registered office; | |||||

| (f) | [deleted] | |||||

| (g) | if the duration of its corporate status is limited, when that status will or may cease; and | |||||

| (h) | the amount of its issued share capital and how much of it is paid up. | |||||

| Directors of an ICVC, other than the ACD | ||||||

| 7 | Other than for the ACD: | |||||

| (a) | the names and positions in the ICVC of any other directors (if any); and | |||||

| (b) | the manner, amount and calculation of the remuneration of such directors. | |||||

| Depositary | ||||||

| 8 | The following information and particulars concerning the depositary: | |||||

| (a) | its name; | |||||

| (b) | the nature of its corporate form; | |||||

| (c) | the address of its registered office; | |||||

| (d) | the address of its head office, if that is different from the address of its registered office; | |||||

| (e) | [deleted] | |||||

| (f) | a description of its duties and conflicts of interest that may arise between the depositary and: | |||||

| (i) | the scheme; or | |||||

| (ii) | the unitholders in the scheme; or | |||||

| (iii) | the authorised fund manager; | |||||

| (g) | (i) | a description of any safekeeping functions delegated by the depositary; | ||||

| (ii) | a description of any conflicts of interest that may arise from such delegation; and | |||||

| (iii) | for a UCITS scheme, a list showing the identity of each delegate and sub-delegate; and | |||||

| (h) | for a UCITS scheme, a statement that up-to-date information regarding the points covered under (a),(f) and (g), above, will be made available to unitholders on request. | |||||

| Investment adviser | ||||||

| 9 | If an investment adviser is retained in connection with the business of an authorised fund: | |||||

| (a) | its name; and | |||||

| (b) | where it carries on a significant activity other than providing services to the authorised fund as an investment adviser, what that significant activity is. | |||||

| Auditor | ||||||

| 10 | The name of the auditor of the authorised fund. | |||||

| Contracts and other relationships with parties | ||||||

| 11 | The following relevant details: | |||||

| (a) | for an ICVC: | |||||

| (i) | a summary of the material provisions of the contract between the ICVC and the ACD which may be relevant to unitholders including provisions (if any) relating to remuneration, termination, compensation on termination and indemnity; | |||||

| (ii) | the main business activities of each of the directors (other than those connected with the business of the ICVC) where these are of significance to the ICVC's business; | |||||

| (iii) | if any director is a body corporate in a group of which any other corporate director of the ICVC is a member, a statement of that fact; | |||||

| (iv) | the main terms of each contract of service between the ICVC and a director in summary form; and | |||||

| (v) | for an ICVC that does not hold annual general meetings, a statement that copies of contracts of service between the ICVC and its directors, including the ACD, will be provided to a unitholder on request; | |||||

| (b) | the names of the directors of the authorised fund manager and the main business activities of each of the directors (other than those connected with the business of the authorised fund) where these are of significance to the authorised fund's business; | |||||

| (c) | a summary of the material provisions of the contract between the ICVC or the manager of the AUT and the depositary which may be relevant to unitholders, including provisions relating to the remuneration of the depositary; | |||||

| (ca) | in the case of an ACS, a summary of the material provisions of the contracts between: | |||||

| (i) | the authorised fund manager and the nominated partner (if any); and | |||||

| (ii) | the authorised fund manager and depositary; | |||||

| which may be relevant to unitholders, including provisions relating to the remuneration of the depositary; | ||||||

| (d) | if an investment adviser retained in connection with the business of the authorised fund is a body corporate in a group of which any director of the ICVC or the authorised fund manager of the AUT or ACS is a member, that fact; | |||||

| (e) | a summary of the material provisions of any contract between the authorised fund manager or the ICVC and any investment adviser which may be relevant to unitholders; | |||||

| (f) | if an investment adviser retained in connection with the business of the authorised fund has the authority of the authorised fund manager or the ICVC to make decisions on behalf of the authorised fund manager or the ICVC, that fact and a description of the matters in relation to which it has that authority; | |||||

| (g) | a list of: | |||||

| (i) | the functions which the authorised fund manager has delegated in accordance with FCA rules; and | |||||

| (ii) | the person to whom such functions have been delegated; and | |||||

| (h) | in what capacity (if any), the authorised fund manager acts in relation to any other regulated collective investment schemes and the name of such schemes. | |||||

| Register of Unitholders | ||||||

| 12 | Details of: | |||||

| (a) | the address in the United Kingdom where the register of unitholders, and where relevant the plan register is kept and can be inspected by unitholders; and | |||||

| (b) | the registrar's name and address. | |||||

| Payments out of scheme property | ||||||

| 13 | In relation to each type of payment from the scheme property, details of: | |||||

| (a) | who the payment is made to; | |||||

| (b) | what the payment is for; | |||||

| (c) | the rate or amount where available; | |||||

| (d) | how it will be calculated and accrued; | |||||

| (e) | when it will be paid; | |||||

| (f) | where a performance fee is taken, examples of its operation in plain English and the maximum it can amount to; and | |||||

| (g) | where donations are to be made to one or more registered charities for Sharia compliance purposes from the income property of the scheme (in this rule, ‘purification’), in addition to the details required above, the person who advises the authorised fund manager on the required percentage of the income property recognised for purification. | |||||

| Payments for research out of scheme property | ||||||

| 13A | In relation to payments from the scheme property relating to a research payment account (see COBS 18 Annex 1 (Research and inducements for collective portfolio managers)) or joint payments for third-party research and execution services (see COBS 18 Annex 1), the following: | |||||

| (a) | where a research payment account is used, the relevant details required by COBS 18 Annex 1 4.8R (Prior disclosure of the research account to investors); and | |||||

| (b) | where joint payments for third-party research and execution services are made out of scheme property, the relevant details required by COBS 18 Annex 1 4.25R (Prior disclosures relating to joint payments for research). | |||||

| Allocation of payments | ||||||

| 14 | If, in accordance with COLL 6.7.10 R (Allocation of payments to income or capital), the authorised fund manager and the depositary have agreed that all or part of any income expense payments may be treated as a capital expense: | |||||

| (a) | that fact; | |||||

| (b) | the policy for allocation of these payments; and | |||||

| (c) | a statement that this policy may result in capital erosion or constrain capital growth. | |||||

| Moveable and immovable property (ICVC only) | ||||||

| 15 | An estimate of any expenses likely to be incurred by the ICVC in respect of movable and immovable property in which the ICVC has an interest. | |||||

| Valuation and pricing of scheme property | ||||||

| 16 | In relation to the valuation of scheme property and pricing of units: | |||||

| (a) | either: | |||||

| (i) | in the case of a single-priced authorised fund, a provision that there must be only a single price for any unit as determined from time to time by reference to a particular valuation point; or | |||||

| (ii) | in the case of a dual-priced authorised fund, the authorised fund manager's policy for determining prices for the sale and redemption of units by reference to a particular valuation point and an explanation of how those prices may differ; | |||||

| (b) | details of: | |||||

| (i) | how the value of the scheme property is to be determined in relation to each purpose for which the scheme property must be valued; | |||||

| (ii) | how frequently and at what time or times of the day the scheme property will be regularly valued for dealing purposes and a description of any circumstance in which the scheme property may be specially valued; | |||||

| (iii) | where relevant, how the price of units of each class will be determined for dealing purposes; | |||||

| (iv) | where and at what frequency the most recent prices will be published; and | |||||

| (v) | where relevant in the case of a dual-priced authorised fund, an explanation of what is meant by large deals and the authorised fund manager's policy in relation to large deals; and | |||||

| (c) | if provisions in (a) and (b) do not take effect when the instrument constituting the fund or (where appropriate) supplemental trust deed takes effect, a statement of the time from which those provisions are to take effect or how it will be determined. | |||||

| Dealing | ||||||

| 17 | The following particulars: | |||||

| (a) | the procedures, the dealing periods and the circumstances in which the authorised fund manager will effect: | |||||

| (i) | the sale and redemption of units and the settlement of transactions (including the minimum number or value of units which one person may hold or which may be subject to any transaction of sale or redemption) for each class of unit in the authorised fund; and | |||||

| (ii) | any direct issue or cancellation of units: | |||||

| (A) | by an ICVC or in the case of an AUT or ACS by the depositary through the authorised fund manager or, where permitted by the instrument constituting the fund, the authorised fund manager in accordance with COLL 6.2.7R (2) (Direct issue and cancellation of units); or | |||||

| (B) | in relation to a direct dealing scheme, by an ICVC or, for an AUT or ACS, by the depositary or, where permitted by the instrument constituting the fund, the authorised fund manager in accordance with COLL 6.2.7AR (Issue and cancellation of units by a direct dealing scheme); | |||||

| (b) | the circumstances in which the redemption or cancellation of units may be suspended; | |||||

| (c) | whether certificates will be issued in respect of registered units; | |||||

| (d) | the circumstances in which the authorised fund manager may arrange for, and the procedure for the issue or cancellation of units in specie; | |||||

| (e) | the investment exchanges (if any) on which units in the scheme are listed or dealt; | |||||

| (f) | the circumstances and conditions for issuing units in an authorised fund which limit the issue of any class of units in accordance with COLL 6.2.18 R (Limited issue); | |||||

| (g) | the circumstances and procedures for the limitation or deferral of redemptions or cancellations in accordance with COLL 6.2.19 R (Limited redemption) or COLL 6.2.21 R (Deferred redemption); | |||||

| (h) | in a prospectus available during the period of any initial offer: | |||||

| (i) | the length of the initial offer period; | |||||

| (ii) | the initial price of a unit, which must be in the base currency; | |||||

| (iii) | the arrangements for issuing units during the initial offer, including the authorised fund manager's intentions on investing the subscriptions received during the initial offer; | |||||

| (iv) | the circumstances when the initial offer will end; | |||||

| (v) | whether units will be sold or issued in any other currency; and | |||||

| (vi) | any other relevant details of the initial offer; | |||||

| (i) | whether a unitholder may effect transfer of title to units on the authority of an electronic communication and if so the conditions that must be satisfied in order to effect a transfer; | |||||

| (j) | if the authorised fund manager deals as principal in units of the scheme and holds them for that purpose, a statement of its policy for doing so and, where applicable: | |||||

| (i) | a description of when the authorised fund manager may retain any profits it earns and absorb any losses it incurs for these activities; and | |||||

| (ii) | a statement of non-accountability as referred to in COLL 6.7.16G; and | |||||

| (k) | if an issue and cancellation account is used, an explanation of the potential consequences if a person with whom money in the issue and cancellation account has been placed on deposit becomes insolvent or is otherwise unable to make payments. | |||||

| Transfers to a dormant asset fund operator | ||||||

| 17A | If the authorised fund manager or the depositary of the authorised fund has a power under the instrument constituting the fund to transfer an eligible CIS amount that is a dormant asset to a dormant asset fund operator in accordance with sections 8 to 10 of the Dormant Assets Act 2022, particulars as to: | |||||

| (a) | the types of such eligible CIS amounts which the authorised fund manager or the depositary may transfer; | |||||

| (b) | the circumstances in which an amount in (a) is a dormant asset, and any steps that the authorised fund manager or the depositary must take before making a transfer; | |||||

| (c) | if the authorised fund manager or the depositary has a power to convert a unit into a right to payment of an amount in accordance with section 9(3) and (5) of the Dormant Assets Act 2022, an explanation of that power, including the circumstances in which the power may be exercised; | |||||

| (d) | the consequences for the unitholder of a transfer of an eligible CIS amount, including how the amount of a repayment claim will be determined; | |||||

| (e) | information about the steps a person would need to take to establish and make a repayment claim, and to receive payment of the money; and | |||||

| (f) | the basis on which a person who has made a repayment claim may apply for the repaid amount or any part of it to be reinvested in units. | |||||

| 17B | If the authorised fund manager or the depositary has a power under the instrument constituting the fund to transfer unwanted asset money to a dormant asset fund operator in accordance with section 21 of the Dormant Assets Act 2022, particulars as to: | |||||

| (a) | the circumstances in which a person may inform the authorised fund manager or the depositary that they wish an eligible CIS amount to be transferred as unwanted asset money to a dormant asset fund operator; | |||||

| (b) | how a person in (a) may obtain information from the authorised fund manager or the depositary about the procedure by which they may ask for such money to be transferred; | |||||

| (c) | the declaration that the person will need to make before the money can be transferred as unwanted asset money; | |||||

| (d) | the consequences of the money being transferred to a dormant asset fund operator; and | |||||

| (e) | what happens if the dormant asset fund operator does not consent to the transfer of the money. | |||||

| Dilution | ||||||

| 18 | In the case of a single-priced authorised fund, details of what is meant by dilution including: | |||||

| (a) | a statement explaining: | |||||

| (i) | that it is not possible to predict accurately whether dilution is likely to occur; and | |||||

| (ii) | which of the policies the authorised fund manager is adopting under COLL 6.3.8 (1) (Dilution) together with an explanation of how this policy may affect the future growth of the authorised fund; and | |||||

| (b) | if the authorised fund manager may require a dilution levy or make a dilution adjustment, a statement of: | |||||

| (i) | the authorised fund manager's policy in deciding when to require a dilution levy, including what is meant by large deals and the authorised fund manager's policy on large deals, or when to make a dilution adjustment; | |||||

| (ii) | the estimated rate or amount of any dilution levy or dilution adjustment based either on historical data or future projections; and | |||||

| (iii) | the likelihood that the authorised fund manager may require a dilution levy or make a dilution adjustment and the basis (historical or projected) on which the statement is made. | |||||

| SDRT provision | ||||||

| 19 | ||||||

| [deleted] | ||||||

| Forward pricing | ||||||

| 20 | An explanation of forward pricing under COLL 6.3.9 (Forward pricing). | |||||

| Preliminary charge | ||||||

| 21 | Where relevant, a statement authorising the authorised fund manager to make a preliminary charge and specifying the basis for and current amount or rate of that charge. | |||||

| Redemption charge | ||||||

| 22 | Where relevant, a statement authorising the authorised fund manager to deduct a redemption charge out of the proceeds of redemption; and if the authorised fund manager makes a redemption charge: | |||||

| (a) | the current amount of that charge or if it is variable, the rate or method of calculating it; | |||||

| (b) | if the amount, rate or method has been changed, that details of any previous amount, rate or method may be obtained from the authorised fund manager on request; and | |||||

| (c) | how the order in which units acquired at different times by a unitholder is to be determined so far as necessary for the purposes of the imposition of the redemption charge. | |||||

| Property Authorised Investment Funds | ||||||

| 22A | For a property authorised investment fund, a statement that: | |||||

| (1) | [deleted] | |||||

| (2) | no body corporate may seek to obtain or intentionally maintain a holding of more than 10% of the net asset value of the fund; and | |||||

| (3) | in the event that the authorised fund manager reasonably considers that a body corporate holds more than 10% of the net asset value of the fund, the authorised fund manager is entitled to delay any redemption or cancellation of units if the authorised fund manager reasonably considers such action to be: | |||||

| (a) | necessary in order to enable an orderly reduction of the holding to below 10%; and | |||||

| (b) | in the interests of the unitholders as a whole. | |||||

| General information | ||||||

| 23 | Details of: | |||||

| (a) | the address at which copies of the instrument constituting the fund, any amending instrument and the most recent annual and half-yearly long reports may be inspected and from which copies may be obtained; | |||||

| (b) | the manner in which any notice or document will be served on unitholders; | |||||

| (c) | the extent to which and the circumstances in which: | |||||

| (i) | the scheme is liable to pay or suffer tax on any appreciation in the value of the scheme property or on the income derived from the scheme property; and | |||||

| (ii) | deductions by way of withholding tax may be made from distributions of income to unitholders and payments made to unitholders on the redemption of units; | |||||

| (d) | for a UCITS scheme, any possible fees or expenses not described in paragraphs 13 to 22, distinguishing between those to be paid by a unitholder and those to be paid out of scheme property; and | |||||

| (e) | for an ICVC, whether or not annual general meetings will be held. | |||||

| Information on the umbrella | ||||||

| 24 | In the case of a scheme which is an umbrella with two or more sub-funds, the following information: | |||||

| (a) | that a unitholder is entitled to exchange units in one sub-fund for units in any other sub-fund (other than a sub-fund which has limited the issue of units); | |||||

| (b) | that an exchange of units in one sub-fund for units in any other sub-fund is treated as a redemption and sale and will, for persons subject to United Kingdom taxation, be a realisation for the purposes of capital gains taxation; | |||||

| (c) | that in no circumstances will a unitholder who exchanges units in one sub-fund for units in any other sub-fund be given a right by law to withdraw from or cancel the transaction; | |||||

| (d) | the policy for allocating between sub-funds any assets of, or costs, charges and expenses payable out of, the scheme property which are not attributable to any particular sub-fund; | |||||

| (e) | what charges, if any, may be made on exchanging units in one sub-fund for units in any other sub-fund; and | |||||

| (f) | for each sub-fund, the currency in which the scheme property allocated to it will be valued and the price of units calculated and payments made, if this currency is not the base currency of the scheme which is an umbrella. | |||||

| (g) | [deleted] | |||||

| Application of the prospectus contents to an umbrella | ||||||

| 25 | For a scheme which is an umbrella, information required must be stated: | |||||

| (a) | in relation to each sub-fund where the information for any sub-fund differs from that for any other; and | |||||

| (b) | for the umbrella as a whole, but only where the information is relevant to the umbrella as a whole. | |||||

| Information on a feeder UCITS | ||||||

| 25A | In the case of a feeder UCITS, the following information: | |||||

| (a) | a declaration that the feeder UCITS is a feeder of a particular master UCITS and as such permanently invests at least 85% in value of the scheme property in units of that master UCITS; | |||||

| (b) | the investment objective and policy, including the risk profile; and whether the performance records of the feeder UCITS and the master UCITS are identical, or to what extent and for which reasons they differ, including a description of how the balance of the scheme property which is not invested in units of the master UCITS is invested in accordance with COLL 5.8.3 R (Balance of scheme property: investment restrictions on a feeder UCITS); | |||||

| (c) | a brief description of the master UCITS, its organisation, its investment objective and policy, including the risk profile, and an indication of how the prospectus of the master UCITS may be obtained; | |||||

| (d) | a summary of the master-feeder agreement or where applicable, the internal conduct of business rules referred to in COLL 11.3.2 R (2) (Master-feeder agreement and internal conduct of business rules); | |||||

| (e) | how the unitholders may obtain further information on the master UCITS and the master-feeder agreement; | |||||

| (f) | a description of all remuneration or reimbursement of costs payable by the feeder UCITS by virtue of its investment in units of the master UCITS, as well as the aggregate charges of the feeder UCITS and the master UCITS; and | |||||

| (g) | a description of the tax implications of the investment into the master UCITS for the feeder UCITS. | |||||

| [Note: article 63(1) of the UCITS Directive] | ||||||

| Information on a feeder NURS | ||||||

| 25B | In the case of a feeder NURS, the following information: | |||||

| (a) | a declaration that the feeder NURS is a feeder of a particular qualifying master scheme and as such is dedicated to units in a single qualifying master scheme and the minimum (and, if relevant, maximum) investment that the feeder NURS may make in its qualifying master scheme; | |||||

| (b) | the investment objective and policy of the feeder NURS, including its risk profile; and whether the performance records of the feeder NURS and the qualifying master scheme are identical, or to what extent and for which reasons they differ, including a description of how the balance of the scheme property which is not invested in units of the qualifying master scheme is invested in accordance with COLL 5.6.7 R (6A) (Spread: general); | |||||

| (c) | a brief description of the qualifying master scheme, its organisation, its investment objective and policy, including the risk profile, and an indication of how the prospectus of the qualifying master scheme may be obtained; | |||||

| (d) | how the unitholders may obtain further information on the qualifying master scheme; | |||||

| (e) | a description of all remuneration or reimbursement of costs payable by the feeder NURS by virtue of its investment in units of the qualifying master scheme, as well as the aggregate charges of the feeder NURS and the qualifying master scheme; and | |||||

| (f) | a description of the tax implications of the investment into the qualifying master scheme for the feeder NURS. | |||||

| Marketing in another EEA state | ||||||

| 26 | [deleted] | |||||

| Investment in overseas property through an intermediate holding vehicle | ||||||

| 26A | If investment in an overseas immovable is to be made through an intermediate holding vehicle or a series of intermediate holding vehicles, a statement disclosing the existence of that intermediate holding vehicle or series of intermediate holding vehicles and confirming that the purpose of that intermediate holding vehicle or series of intermediate holding vehicle is to enable the holding of overseas immovables by the scheme. | |||||

| Sustainability information | ||||||

| 26B | The following information, as applicable: | |||||

| (a) | where a sustainability label is used in relation to a scheme, the information set out at ESG 5.3.3R and ESG 5.3.6R, in accordance with ESG 5.3.2R(1); | |||||

| (b) | where a sustainability label is not used in relation to a scheme, but that scheme uses the terms in ESG 4.3.2R(2) under ESG 4.3.2R(1) in the product’s name or in a financial promotion relating to that scheme, the information required under ESG 5.3.2R(2). | |||||

| Additional information | ||||||

| 27 | Any other material information which is within the knowledge of the directors of an ICVC or the authorised fund manager of an AUT or ACS, or which the directors or authorised fund manager would have obtained by making reasonable enquiries, including but not confined to, the following matters: | |||||

| (a) | information which investors and their professional advisers would reasonably require, and reasonably expect to find in the prospectus, for the purpose of making an informed judgement about the merits of investing in the authorised fund and the extent and characteristics of the risks accepted by so participating; | |||||

| (b) | a clear and easily understandable explanation of any risks which investment in the authorised fund may reasonably be regarded as presenting for reasonably prudent investors of moderate means; | |||||

| (c) | if there is any arrangement intended to result in a particular capital or income return from a holding of units in the authorised fund or any investment objective of giving protection to the capital value of, or income return from, such a holding: | |||||

| (i) | details of that arrangement or protection; | |||||

| (ii) | for any related guarantee, sufficient details about the guarantor and the guarantee to enable a fair assessment of the value of the guarantee; | |||||

| (iii) | a description of the risks that could affect achievement of that return or protection; and | |||||

| (iv) | details of the arrangements by which the authorised fund manager will notify unitholders of any action required by the unitholders to obtain the benefit of the guarantee; and | |||||

| (d) | whether any notice has been given to unitholders of the authorised fund manager intention to propose a change to the scheme and if so, its particulars. | |||||

| Remuneration Policy | ||||||

| 28 | For a UCITS scheme and in relation to UCITS Remuneration Code staff: | |||||

| (a) | up-to-date details of the remuneration policy including, but not limited to: | |||||

| (i) | a description of how remuneration and benefits are calculated; and | |||||

| (ii) | the identities of persons responsible for awarding the remuneration and benefits, including the composition of the remuneration committee, where such a committee exists; or | |||||

| (b) | a summary of the remuneration policy and a statement that: | |||||

| (i) | up-to-date details of the matters set out in (a) above are available by means of a website, including a reference to that website; and | |||||

| (ii) | a paper copy of that website information will be made available free of charge upon request. | |||||

[Note: A transitional provision applies to row 3(ca) of this table: see COLL TP 1.28.]

The Securities Financing Transactions Regulation sets out the additional information which:

an authorised fund manager of a UCITS scheme must include in the UCITS scheme prospectus; and

an authorised fund manager who is a full-scope UK AIFM of a non-UCITS retail scheme must make available to investors before they invest.

COLL 4.2.5BEU and COLL 4.2.5CEU copy out the relevant provisions of that regulation.

An authorised fund manager who is a full-scope UK AIFM of a non-UCITS retail scheme should publish the information in the scheme’s prospectus.

An authorised fund manager of a UCITS scheme or a non-UCITS retail scheme that does not use securities financing transactions or total return swaps is not required to include the information in COLL 4.2.5CEU in the prospectus or other pre-sale documents.

[Note: A transitional provision applies to COLL 4.2.5AG: see COLL TP 1.38G]

| Transparency of collective investment undertakings in pre-contractual documents | |

|---|---|

| 1. | The prospectus referred to in [COLL 4.2.2R], and the disclosure by AIFMs to investors required by [FUND 3.2.2R] shall specify the SFT and total return swaps which UCITS management companies or UCITS investment companies, and AIFMs respectively, are authorised to use and include a clear statement that those transactions and instruments are used. |

| 2. | The prospectus and the disclosure to investors referred to in paragraph 1 shall include the data provided for in Section B of the Annex. |

| [Note: article 14(1) and (2) of the Securities Financing Transactions Regulation and article 3 for relevant definitions] | |

| Information to be included in the UCITS Prospectus and AIF disclosure to investors: | ||

|---|---|---|

| _ | General description of the SFTs and total return swaps used by the collective investment undertaking and the rationale for their use. | |

| _ | Overall data to be reported for each type of SFTs and total return swaps | |

| _ | Types of assets that can be subject to them. | |

| _ | Maximum proportion of AUM that can be subject to them. | |

| _ | Expected proportion of AUM that will be subject to each of them. | |

| _ | Criteria used to select counterparties (including legal status, country of origin, minimum credit rating). | |

| _ | Acceptable collateral: description of acceptable collateral with regard to asset types, issuer, maturity, liquidity as well as the collateral diversification and correlation policies. | |

| _ | Collateral valuation: description of the collateral valuation methodology used and its rationale, and whether daily mark-to-market and daily variation margins are used. | |

| _ | Risk management: description of the risks linked to SFTs and total return swaps as well as risks linked to collateral management, such as operational, liquidity, counterparty, custody and legal risks and, where applicable, the risks arising from its reuse. | |

| _ | Specification of how assets subject to SFTs and total return swaps and collateral received are safe-kept (e.g. with fund custodian). | |

| _ | Specification of any restrictions (regulatory or self-imposed) on reuse of collateral. | |

| _ | Policy on sharing of return generated by SFTs and total return swaps: description of the proportions of the revenue generated by SFTs and total return swaps that is returned to the collective investment undertaking, and of the costs and fees assigned to the manager or third parties (e.g. the agent lender). The prospectus or disclosure to investors shall also indicate if these are related parties to the manager. | |

[Note: section B of the annex to the Securities Financing Transactions Regulation and article 3 for relevant definitions.] [Note: AUM means assets under management.] | ||

In relation to COLL 4.2.5R (3)(b) the prospectus might include:

a description of the extent (if any) to which that policy does not envisage the authorised fund remaining fully invested at all times;

for a non-UCITS retail scheme which may invest in immovable property:

the maximum extent to which the scheme property may be invested in immovables; and

a statement of the policy of the authorised fund manager in relation to insurance of immovables forming part of the scheme property; and

a description of any restrictions in the assets in which investment may be made, including restrictions in the extent to which the authorised fund may invest in any category of asset, indicating (if appropriate) where the restrictions are more onerous than those imposed by COLL 5 (Investment and borrowing powers).

In relation to COLL 4.2.5R(3)(c-b), the prospectus might explain, if it is the case, that one index or factor may be used for both a target benchmark and a constraining benchmark in relation to the same scheme.

In relation to COLL 4.2.5R (13), the type of payments are likely to include management fees (such as periodic and performance fees), depositary fees, custodian fees, transaction fees, registrar fees, audit fees and FCA fees. Expenses which represent properly incurred costs of the scheme may also be treated as a type of payment for this purpose.

[deleted]

In relation to COLL 4.2.5 R (16)(a), where the prospectus includes provisions for both a single-priced authorised fund and a dual-priced authorised fund, it should state prominently which method of pricing is applicable to which authorised fund, and explain how the differences between them may affect unitholders (for example if a unitholder exchanges units in a single-priced authorised fund for units in a dual-priced authorised fund, or vice versa).

In relation to COLL 4.2.5R(3)(pa)(ii) and (iii), the types of liquidity management tools and arrangements that should typically be described include:

suspension of dealing under COLL 7.2.-3R, COLL 7.2.-2R, COLL 7.2.-1R and COLL 7.2.1R;

fair value price adjustment (see COLL 6.3.3ER, and COLL 6.3.6G(1)(5) to COLL 6.3.6G(1)(7));

fair and reasonable valuation of an immovable (see COLL 6.3.6G(1)(7A) and COLL 6.3.6G(1)(7B)); and

measures to prevent dilution, such as applying a dilution levy (see COLL 6.3.8R).

Additional matters which are not contained in COLL 4.2.5 R may be required to be included in the prospectus, for example for the purposes of making the scheme eligible under relevant tax legislation.

The authorised fund manager of a UCITS scheme should consider the appropriateness of including additional matters in its prospectus as a result of the ESMA Guidelines on ETFs and other UCITS issues (ESMA 2012/832).

A full-scope UK AIFM that is the authorised fund manager of a non-UCITS retail scheme should ensure that the prospectus of the scheme includes the information required under FUND 3.2 (Investor information) and COLL 4.2.5R.

The authorised fund manager need not state the same information twice to satisfy both sets of requirements.

This section applies to an authorised fund manager.

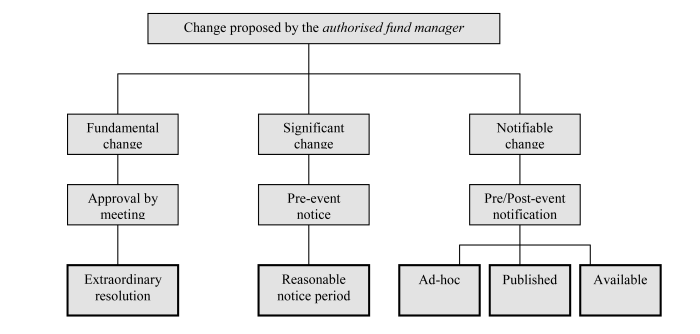

The diagram in COLL 4.3.3 G explains how an authorised fund manager should treat changes it is proposing to a scheme and provides an overview of the rules and guidance in this section.

Regulation 21 of the OEIC Regulations (The Authority's approval for certain changes in respect of a company), section 261Q of the Act (Alteration of contractual schemes and changes of operator or depositary) and section 251 of the Act (Alteration of schemes and changes of manager or trustee) require the prior approval of the FCA for certain proposed changes to an authorised fund, including a change of the authorised fund manager or depositary or a change to the instrument constituting the fund. This should be kept in mind when considering any proposed change.

This diagram belongs to COLL 4.3.2 G.

The authorised fund manager, must, by way of an extraordinary resolution, obtain prior approval from the unitholders for any proposed change to the scheme which, in accordance with (2), is a fundamental change.

A fundamental change is a change or event which:

changes the purposes or nature of the scheme; or

may materially prejudice a unitholder; or

alters the risk profile of the scheme; or

introduces any new type of payment out of scheme property.

Any change may be fundamental depending on its degree of materiality and effect on the scheme and its unitholders. Consequently an authorised fund manager will need to determine whether in each case a particular change is fundamental in nature or not.

For the purpose of COLL 4.3.4R (2)(a) to COLL 4.3.4R (2)(c) a fundamental change to a scheme is likely to include:

any proposal for a scheme of arrangement referred to in COLL 7.6.2 R (Schemes of arrangement: requirements);

a change in the investment policy to achieve capital growth from investment in one country rather than another;

a change in the investment objective or policy to achieve capital growth through investment in fixed interest rather than equity investments;

a change in the investment policy to allow the authorised fund to invest in derivatives as an investment strategy which increases its volatility;

a change to the characteristics of a scheme to distribute income annually rather than monthly; or

the introduction of limited redemption arrangements.

The authorised fund manager must give prior written notice to unitholders, in respect of any proposed change to the operation of a scheme that, in accordance with (2), constitutes a significant change.

A significant change is a change or event which is not fundamental in accordance with COLL 4.3.4 R but which:

affects a unitholder's ability to exercise his rights in relation to his investment; or

would reasonably be expected to cause the unitholder to reconsider his participation in the scheme; or

results in any increased payments out of the scheme property to an authorised fund manager or any other director of an ICVC or an associate of either; or

materially increases other types of payment out of scheme property; or

results in the authorised fund manager introducing joint payments for third-party research and execution services (see COBS 18 Annex 1 (Research and inducements for collective portfolio managers)).

The notice period in (1) must be of a reasonable length (and must not be less than 60 days).

Changes may be significant depending in each case on their degree of materiality and effect on the scheme and its unitholders. Consequently the authorised fund manager will need to determine whether in each case a particular change is significant in nature or not.

For the purpose of COLL 4.3.6 R a significant change is likely to include:

a change in the method of price publication;

a change in any operational policy such as dilution policy or allocation of payments policy;

an increase in the preliminary charge where units are purchased through a group savings plan; or

a change in the pricing arrangements for units of the scheme so as to cause a single-priced authorised fund to become a dual-priced authorised fund, or vice versa.

Where the directors of an ICVC elect to discontinue holding annual general meetings under paragraph 37A of the OEIC Regulations, they are required to give 60 days' written notice to shareholders. For the purpose of COLL 4.3.6 R this should be treated as a significant change to the operation of the scheme.

[deleted]

The authorised fund manager must inform unitholders in an appropriate manner and timescale of any notifiable changes that are reasonably likely to affect, or have affected, the operation of the scheme.

A notifiable change is a change or event, other than a fundamental change under COLL 4.3.4 R or a significant change under COLL 4.3.6 R, which a unitholder must be made aware of unless the authorised fund manager concludes that the change is insignificant.

The circumstances causing a notifiable change may or may not be within the control of the authorised fund manager.

For the purpose of COLL 4.3.8 R (Notifiable changes) a notifiable change might include:

a change of named investment manager where the authorised fund has been marketed on the basis of that individual's involvement;

a significant political event which impacts on the authorised fund or its operation;

a change to the time of the valuation point;

the introduction of limited issue arrangements; or

a change of the depositary or a change in the name of the authorised fund.

The appropriate manner and timescale of notification would depend on the nature of the change or event. Consequently the authorised fund manager will need to assess each change or event individually.

An appropriate manner of notification could include:

sending an immediate notification to the unitholder;

publishing the information on a website; or

the information being included in the next long report of the scheme.

Where the authorised fund manager of either a feeder UCITS or a feeder NURS is notified of any change in respect of its master UCITS or qualifying master scheme which has the effect of a change to the feeder UCITS or feeder NURS, the authorised fund manager must:

classify it as a fundamental change, significant change or a notifiable change to the feeder UCITS or feeder NURS in accordance with the rules in this section; and

for a fundamental change, obtain approval from the unitholders by way of an extraordinary resolution; or

for a significant change, give written notice to unitholders of that change; or

for a notifiable change, comply with COLL 4.3.8 R (Notifiable changes).

The actions required by COLL 4.3.11 R (2)(a) and (b) must be carried out as soon as reasonably practicable after the authorised fund manager of the feeder UCITS or feeder NURS has been informed of the relevant change to the master UCITS or qualifying master scheme.

The authorised fund manager of the feeder UCITS or feeder NURS should assess the change to the master UCITS or qualifying master scheme in terms of its impact on the feeder UCITS or feeder NURS. For example, a change to the investment objective and policy of the master UCITS or qualifying master scheme that alters its risk profile would constitute a fundamental change for the feeder UCITS or feeder NURS. In order for the feeder UCITS or feeder NURS to continue investing in the master UCITS or qualifying master scheme, the authorised fund manager of the feeder UCITS or feeder NURS should obtain the approval of unitholders by way of an extraordinary resolution, or else make a proposal to invest in a different master UCITS or qualifying master scheme. For a feeder UCITS this should be done in accordance with COLL 11.2.2 R (Application for approval of an investment in a master UCITS).

Not all changes affecting the master UCITS or qualifying master scheme will have the same significance for the feeder UCITS or feeder NURS and its unitholders. For example, a change to how the prices of the units in the master UCITS or qualifying master scheme are published might not be a significant change for the feeder UCITS or feeder NURS if the prices of its own units continue to be published in the same way.

Where the authorised fund manager of the feeder UCITS or feeder NURS receives insufficient notice of the intended change to the master UCITS or qualifying master scheme to be able to seek the prior approval of unitholders to any fundamental change or to inform them at least 60 days in advance of any significant change, it should nevertheless use reasonable endeavours to inform them of the change as soon as possible so that they can make an informed judgement about the merits of continuing to invest in the feeder UCITS or feeder NURS.

This section applies to an authorised fund manager, a depositary and any other director of an ICVC.

In this section:

a ‘physical meeting’ is a general meeting convened at a physical location where unitholders, or their proxy, must be physically present;

a ‘hybrid meeting’ is a general meeting which allows unitholders, or their proxy, to be physically present at the location where the meeting is convened, or to attend and vote remotely; and

a ‘virtual meeting’ is a general meeting where all unitholders, or their proxy, attend and vote remotely.

The authorised fund manager, the depositary or the other directors of an ICVC may convene a general meeting of unitholders at any time.

The unitholders may request the convening of a general meeting by a requisition which must:

state the objects of the meeting;

be dated;

be signed by unitholders who, at that date, are registered as the unitholders of units representing not less than one-tenth in value (or such lower proportion stated in the instrument constituting the fund ) of all of the units then in issue; and

be deposited at the head office of the ICVC or with the depositary of an AUT or ACS.

The authorised fund manager, the depositary or the other directors of an ICVC must on receipt of a requisition that complies with (2), immediately convene a general meeting of the authorised fund for a date no later than eight weeks after receipt of the requisition.

The advisory committee of a charity authorised investment fund may also request the convening of a general meeting of unitholders by giving notice in accordance with COLL 14.3.5R.

The instrument constituting the fund may make provision for a general meeting to be:

a hybrid meeting; or

but in any event the authorised fund manager may hold a virtual meeting or a hybrid meeting if this is not inconsistent with any provisions in the instrument constituting the fund.

Any unitholder who participates remotely in a hybrid meeting by the means specified in the notice given under COLL 4.4.5R is deemed to be present at the meeting and has the same rights as a unitholder who is physically present at the meeting.

Any unitholder who participates in a virtual meeting by the means specified in the notice given under COLL 4.4.5R is deemed to be present at the meeting and has the same rights that the unitholder would have at a physical meeting.

Any unitholder who participates remotely must be enabled to do so without having to appoint a proxy and must not be required to submit their vote on a resolution in advance of the meeting.

This section applies, unless the context otherwise requires, to class meetings by reference to the units of the class concerned and the unitholders and prices of such units.

Unless a unit in the authorised fund is a participating security, in this section "unitholders" means unitholders as at a cut-off date selected by the authorised fund manager which is a reasonable time before notices of the relevant meeting are sent out.

If any unit in the authorised fund is a participating security, a registered unitholder of such a unit is entitled to receive a notice of a meeting or a notice of an adjourned meeting under COLL 4.4.5 R (Notice of general meetings), if entered on the register at the close of business on a day to be determined by the authorised fund manager, which must not be more than 21 days before the notices of the meeting are sent out.

For the purposes of (2), in COLL 4.4.6 R (Quorum) to COLL 4.4.11 R (The chair, adjournments and minutes) "unitholders" in relation to those units means the persons entered on the register at a time to be determined by the authorised fund manager and stated in the notice of the meeting, which must not be more than 48 hours before the time fixed for the meeting.

Where the authorised fund manager, the depositary or the other directors of an ICVC decide to convene a general meeting of unitholders:

each unitholder must be given at least 14 days written notice, inclusive of the date on which the notice is first served and the day of the meeting;

the notice must specify:

whether the meeting is to be a physical meeting, a hybrid meeting or a virtual meeting;

if the meeting is a physical meeting or a hybrid meeting, the place of the meeting;

if the meeting is a hybrid meeting or a virtual meeting, the means by which a unitholder may participate, including any requirements for unitholders to register before the meeting begins or to provide proof of their right to attend, and an explanation of how participating unitholders may vote in a show of hands or in a poll, if they do not appoint a proxy;

the day and hour of the meeting;

the terms of the resolutions to be proposed; and

the address of the website where the minutes of the meeting will subsequently be published; and

a copy of the notice must be sent to the depositary.

The accidental omission to give notice to, or the non-receipt of notice by, any unitholder does not invalidate the proceedings at any meeting.

Notice of an adjourned meeting of unitholders must be given to each unitholder, stating that while two unitholders are required to be present – in person, by proxy or remotely – to constitute a quorum at the adjourned meeting, this may be reduced to one in accordance with COLL 4.4.6R (3), should two such unitholders not be present after a reasonable time of convening of the meeting.

Paragraph (1)(a) does not apply to the notice of an adjourned meeting.

Where the meeting is a hybrid meeting or a virtual meeting, the authorised fund manager must take reasonable care to ensure that the necessary supporting technology to enable unitholders to attend and vote is in place at the start of the meeting and operates adequately throughout its proceedings, so that unitholders who attend or vote remotely are not unfairly disadvantaged.

The quorum required to conduct business at a meeting of unitholders is two unitholders, present in person, by proxy or (where applicable) remotely using the means specified in the notice given under COLL 4.4.5R.

If after a reasonable time from the time for the start of the meeting, a quorum is not present, the meeting:

if convened on the requisition of unitholders, must be dissolved; and

in any other case, must stand adjourned to:

a day and time which is seven or more days after the day and time of the meeting; and

in the case of a physical meeting or a hybrid meeting, a place to be appointed by the chair.

If, at an adjourned meeting under (2)(b), a quorum is not present after a reasonable time from the time for the meeting, one person entitled to be counted in a quorum present at the meeting shall constitute a quorum.

The chair of a meeting which permits unitholders to attend and vote remotely must take reasonable care to give such unitholders:

an adequate opportunity to be counted as present in the quorum; and

sufficient opportunities to participate fully in the proceedings of the meeting, in particular when a vote is taken on a show of hands or by poll.

Except where an extraordinary resolution is specifically required or permitted, any resolution of unitholders is passed by a simple majority of the votes validly cast at a general meeting of unitholders.

In the case of an equality of, or an absence of, votes cast, the chair is entitled to a casting vote.

Where a resolution (including an extraordinary resolution) is required to conduct business at a meeting of unitholders and every unitholder is prohibited under COLL 4.4.8R (4) from voting, it shall not be necessary to convene such a meeting and a resolution may, with the prior written agreement of the depositary to the process, instead be passed with the written consent of unitholders representing 50% or more, or for an extraordinary resolution 75% or more, of the units of the scheme in issue.

On a show of hands every unitholder who is present in person, or who attends the meeting remotely using the means specified in the notice in COLL 4.4.5R, has one vote.

On a poll:

votes may be given either personally or by proxy or in another manner permitted by the instrument constituting the fund;

the voting rights for each unit must be the proportion of the voting rights attached to all of the units in issue that the price of the unit bears to the aggregate price or prices of all of the units in issue:

if any unit is a participating security, at the time determined under COLL 4.4.4R (2) (Special meaning of Unitholder in COLL 4.4);

otherwise at the date specified in COLL 4.4.4R (1); and

a unitholder need not use all his votes or cast all his votes in the same way.

For joint unitholders, the vote of the most senior who votes, whether in person, by proxy or remotely by the means referred to in (1), must be accepted to the exclusion of the votes of the other joint unitholders. For this purpose seniority must be determined by the order in which the names stand in the register of unitholders.

No director of the ICVC or the authorised fund manager of an AUT or ACS can be counted in the quorum of, and no such director or the authorised fund manager of an AUT or ACS nor any of their associates may vote at, any meeting of the authorised fund.

The prohibition in (4) does not apply to any units held on behalf of, or jointly with, a person who, if himself the registered unitholder, would be entitled to vote and from whom the director, the authorised fund manager of an AUT or ACS or its associate have received voting instructions.

For the purpose of this section, units held, or treated as held, by the authorised fund manager or any other director of the ICVC, must not, except as mentioned in (5), be regarded as being in issue.

A resolution put to the vote of a general meeting must be determined on a show of hands unless a poll is (before or on the declaration of the result of the show of hands) demanded by:

the chair;

at least two unitholders; or

the depositary.

Unless a poll is demanded in accordance with (1), a declaration by the chair as to the result of a resolution is conclusive evidence of the fact.

A unitholder may appoint another person to attend a general meeting and vote in his place.

Unless the instrument constituting the fund provides otherwise, a unitholder may appoint more than one proxy to attend on the same occasion but a proxy may vote only on a poll.

Every notice calling a meeting of a scheme must contain a reasonably prominent statement that a unitholder entitled to attend and vote may appoint a proxy.

For the appointment to be effective, any document relating to the appointment of a proxy must not be required to be received by the ICVC or any other person more than 48 hours before the meeting or adjourned meeting

A meeting of unitholders must have a chair, nominated:

in the case of an AUT or ACS, by the depositary;

in the case of an ICVC, by a director other than the ACD or an associate of the ACD or, if no such nomination is made, by the depositary.